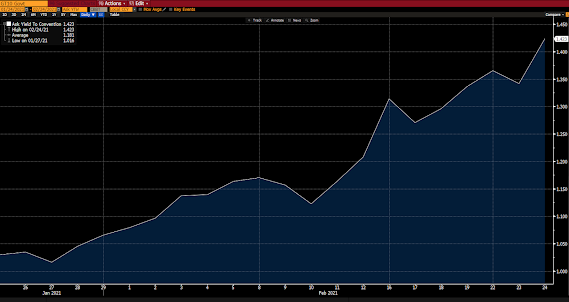

It’s unusual for us to be featuring the boring 10-year yield chart so frequently here on the blog. Of course, as you’ve noticed, things have gotten a bit lively there of late.

Here’s a 1-month look:

Oh, and by the way, this isn’t by any stretch a U.S.-only phenomenon.

Note the blue dots (now) vs the orange diamonds (average) in the range column below for 10-year sovereign yields across major regions:

In the old days this might be a signal to central banks that it’s time to begin (or begin thinking about) tightening, lest things get away from them.

Well, Fed Chair J. Powell will be delivering day-2 of his semi-annual report to Congress this morning, and I assure you he will more than reiterate his pledge to keep the floodgates wide open farther, for certain, than the market eye can see. Essentially the same message came from the Reserve Bank of New Zealand overnight.

Interestingly, there is one major player, however, who is actually thinking about central bank-fed asset bubbles and has been doing a bit of reigning in of late; China.

Here’s from the South China Morning Post earlier this month:

“China’s central bank has once again drained money from the financial system in the midst of market concerns that its stimulative monetary policy has reached a “turning point” in the face of weakening economic data due to fresh coronavirus outbreaks.

Even though the world’s other major economies, particularly the United States, are mulling new stimulus packages to combat the economic damage caused by the pandemic, Beijing has been considering fine-tuning some of its temporary support policies enacted last year.

This comes amid growing fears among some policymakers that excess liquidity might lead to asset bubbles, which would increase already high debt levels and pose risks to the financial system.”

“…excess liquidity might lead to asset bubbles, which would increase already high debt levels and pose risks to the financial system.” Ya think!

Asian markets got walloped overnight as Hong Kong increased what amounts to a tax on financial transactions: All but two of the 16 markets we track closed notably lower.

Europe, on the other hand, is leaning green this morning, with 12 of the 19 bourses we follow trading higher as I type.

U.S. major averages are mixed to start the day: Dow (despite half of its members in the red) is up 77 points (0.25%), SP500 up 0.02%, SP500 Equal Weight up 0.63%, Nasdaq 100 down 0.92%, Russell 2000 up 0.66%.

Oil futures are up 2.64%, gold’s down 0.75%, silver’s down 0.16%, copper futures are up 0.80% and the ag complex is up 0.83%.

The 10-year treasury is down (yield up) and the dollar is up 0.21%.

Our core positions are pretty much split down the middle to start the day. With oil services, energy, banks, miners and AT&T leading the leaders, while emerging market equites, Asia-Pac, gold, tech and the yen lead the laggards. All in we’re off 0.05% as I type.

I’m thinking about Carl Popper as I take in Fed Chair Powell’s comments this week:

“When we are faced with a falsification, we can always talk our way out somehow or other; we can introduce an auxiliary hypothesis and reject the falsification. We can ‘immunize’ our theories against all possible falsification…”