It’s interesting… Listening to “Wall Street”… Looking at retail investor sentiment surveys…. Tracking the bull/bear sentiment spread emerging from investment advisor surveys… Measuring the cash (lack thereof) held by mutual funds… And, per today’s Bloomberg article titled Bubble Deniers Abound to Dismiss Valuation Metrics One by One, considering the number of perhaps legitimate gurus who are capitulating (like it’s 1999) to the notion that traditional valuation metrics simply don’t matter, as, “it’s different this time” — well, I for one, would offer up zero argument if you were to suggest to me that sentiment is, at present, dangerously optimistic.

Funny thing is, however, I just scored our own “Fear/Greed Barometer” — and it comes in at +10, which is actually an, albeit slightly, net fear reading.

So what gives? I mean, given all that I typed into that first paragraph, you’d think our indicator would be at -100. Max greed!

Well, indeed, the individual investor and investment advisor sentiment readings are screaming greed, but 5 of our market-based metrics suggest that the quiet “smart” money is positioning (or protecting) itself in a manner that is anything but optimistic.

Take a look:

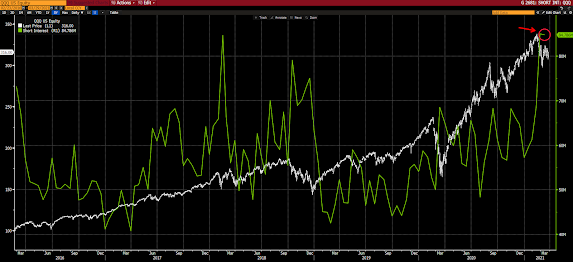

Here (in blue) is the short interest on SPY (the most heavily traded ETF that tracks the SP500 Index) — (pardon all of my annotations; just follow the red arrow on the right):

That’s a not-small spike in the number of trades anticipating a not-small selloff…

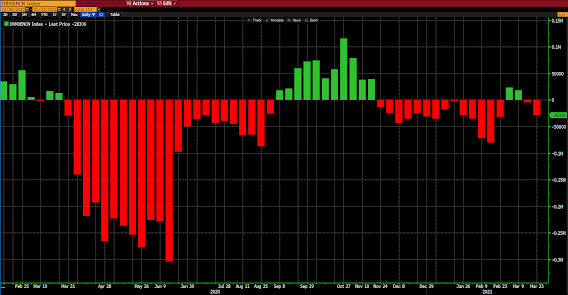

Here (green) is the short interest graph for QQQ (the Nasdaq 100 tracking ETF):

That’s a serious bearish position! Anticipating a notable correction in the tech sector, which, btw, we’ve begun to witness of late. I.e., the Nasdaq 100 is now negative on the year…

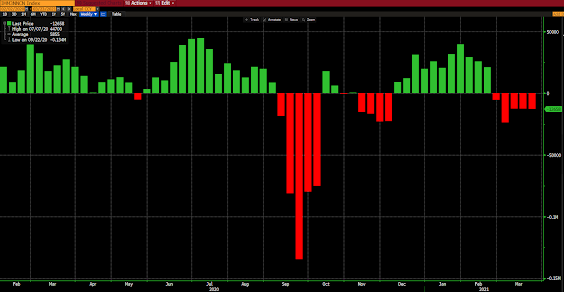

As for futures speculators, they’re presently net short SP500 contracts:

They’re net short Nasdaq 100’s as well:

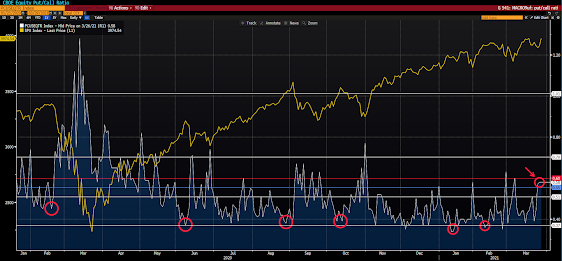

And, with regard to options, the CBOE Equity Put/Call Ratio is showing a notable rise in put (downside bets) volume, relative to call (upside bets) volume:

Hmm…

Now, you can view this in two different lights:

1. You can go where it appears that I’m leading you… I.e., perhaps investors and advisors are dangerously complacent (if not ignorant) with regard to some serious near-term underlying risk… After all, I did refer to the folks whose actions those 5 graphs illustrate as the “smart money.”

Or,

2. You can view it all as simply more fuel to push the market yet further into all-time high territory. As, let’s say, we get some bullish commentary from the Fed, positive news around the next multi-trillion dollar stimulus package, or some strong economic data releases forcing those bears to cover their shorts (i.e., buy!).

Although, look out for rising interest rates in that positive data scenario (they’ve played real havoc with tech stocks of late)…

What do I think? Well, those two different lights are equally legitimate points of view. However, for the moment, I’d say that they’re relevant only in a short-term sense…

In a longer-term, fundamental, context, the overall setup is, frankly, the definition of precarious!

Now, don’t get me wrong, that doesn’t mean that the market, beyond the very short-term, is about to fall apart. In fact, one can argue that with the economy opening up and more stimulus in the pipeline, the odds of a major market mishap are relatively low.

But, then again, the market leadership (tech and FAANG (Facebook, Apple, Amazon, Netflix, Google) has been rolling over of late, despite all that “good stuff” to come… Which, as we know, in retrospect, typically spells the beginning of the end for bull markets…

Now, that said, it could very well be that this go-round we’re simply witnessing a rotation out of the leaders and into the previously-weaker value/reflation trades. And that, say, FAANG — rather than ultimately dragging everything with them into the next bear market abyss — are simply consolidating their post-covid gains and will ultimately resume their climb to never-before seen heights, and valuations…

Bottom line: No doubt, with regard to those two different lights, #1 resonated with some of you, #2 with others. We humans simply can’t help it; we’re either drawn to what we want, or to what we fear. And it’s not entirely innate. Our surroundings — what we watch, whom we listen to, our past experiences, and so on — can indeed influence our bias toward fear or greed at any given moment…

As portfolio managers to many of you readers, we here at PWA have to do everything humanly possible to remain open-minded to any and all possibilities. Which is why we must constantly, and painstakingly, crunch the data, study and chart the history, measure the thickness of the ice, take the outside temperature and, when it’s all said and done (which of course it never is), position according to our ever-evolving (along with ever-changing general conditions) risk/reward thesis…