We’ve been fielding an unusual number of market-related inquiries from clients of late. Interestingly, they’re coming from two distinctly different angles; and I’d say the split is roughly 70/30. That is, it seems like better than 2/3rds are soliciting our thoughts on the market’s amazing run from a skeptical point of view, others conversely are asking if perhaps we should untether some of their fixed income holdings (read cash and short-term CDs, currently) to get more capital working in the equity market.

From the former we’re hearing that they’re reading stuff that says the market’s gotten way ahead of itself, that investors are dangerously optimistic, and so on. And, thus, they’re getting nervous. The latter are reading other stuff that says the presently strong global economy, coupled with tax cuts, etc., here at home paints a mid-’90s picture, that, therefore, suggests we’ve got a good few years to go.

With all due respect to those of you whom I’m writing about, there’s always more to an investor’s present state of mind than simply what he/she happens to be reading, and/or watching on the financial networks. We’re all human, with all that it entails. And we humans come with innate emotions, tendencies and opinions. In terms of opinions, alas, the strongest among many folks has to do with their politics, but let’s not go there… The point being, who we are can cloud our perceptions — and we do mean “we”.

Our point in the previous paragraph is paramount to this discussion. When we say “we” we’re talking about you, about us and about the media-favored “experts” whom you may be listening to.

To cut to the chase: Certainty is a luxury no one can afford when it comes to world financial markets. And anyone — credentials notwithstanding — who would predict markets (any markets) with table-pounding certainty is someone to avoid like the measles!

In terms of us here at PWA, knowing that we’re human just like everybody else demands that we do everything, well, humanly possible to set aside our own proclivities, biases, emotions, whatever, and listen to what the world markets — via the data — are telling us. And while the latest readings from our macro model, as well as the technical trends (among virtually all things cyclical), has been music to the ears of our clients who prefer the bullish mid-90s narrative, when it comes to the music, we’ve, frankly, thrown away our speakers. Again, we look at the data, test it against history, and form our own conclusions; which truly should be music to the ears of you clients out there!

So now we’re going to hopefully turn down the volume just a bit for you presently hard partiers:

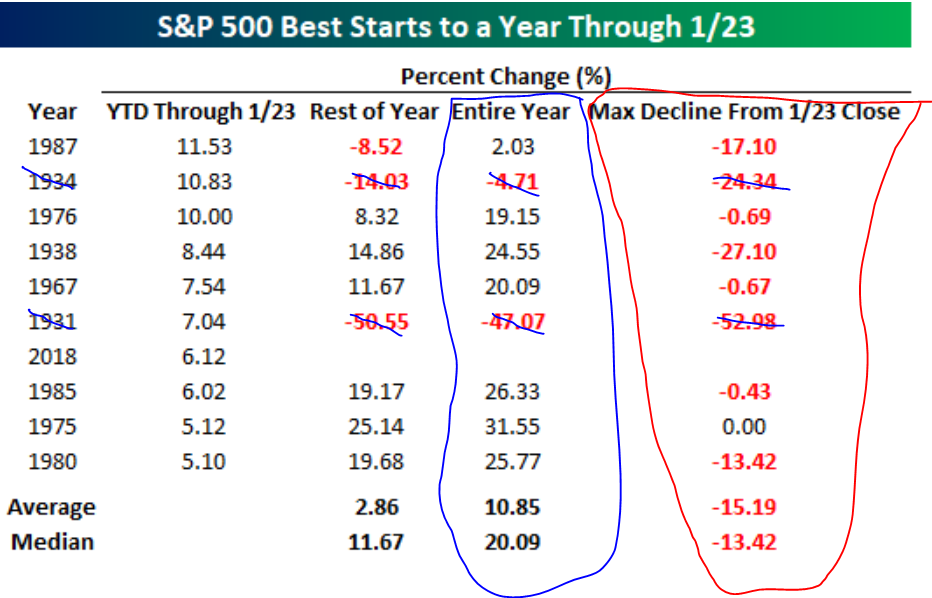

As of yesterday the S&P 500 has logged its seventh-best start to a year in history; there have been only 9 (counting this year) with returns exceeding 5% by January 23rd. And save for the two Great Depression occurrences, that’s historically good news for the bulls: The average full-year gain for the remaining years that experienced a better than 5% gain as of January 23rd was 21.35% (10.85% counting the recession years).

Here’s where the slow-dance music comes in: The average max decline (during the year) from January 23rd in each of those years was -8.49% (-15.19% counting the depression years).

source: Bespoke Investment Group

You know how we keep reminding you about volatility? This is why! And, alas, we’re getting the sense that too many folks simply aren’t expecting it.

Case in point: Spoke with a friend the other day who said he wasn’t at all worried last week when the Dow dropped over 200 points in a day. He absolutely knew that it would be right back up the next day. Of course I tried, but I suspect my dear friend’s nerves are going to be tested during the course of this year… -8.49% (and that’s just the average) is 1,300 Dow points from here!

So, then, the 2/3rds of our inquirers (the skeptics) are right to come knocking, right? Well, not if they were to suggest that we try and anticipate when the volatility will occur, and, thus, somehow time our way to riches! Statistically-speaking that’s a profoundly losing game for the vast majority who attempt it. Plus, save for the Great Depression (when I suspect our macro model would have been bleeding red), years like 2018 have been quite generous to the patient volatility-tolerant investor. Which is consistent with our assessment as I type here today.

That last sentence said, again, there is no certainty when it comes to markets! There’s only thoughtful analysis and decision-making based on probabilities — which are determined based on the concurrent weight of the evidence. When the weight of the evidence changes so will our assessment of the probabilities, and so will our target allocations.

Have a great rest of your week!

Marty