Monday’s release of NAHB’s monthly homebuilder sentiment read had builders feeling a bit better about their current setup and essentially the same regarding future expectations, in comparison to the previous month.

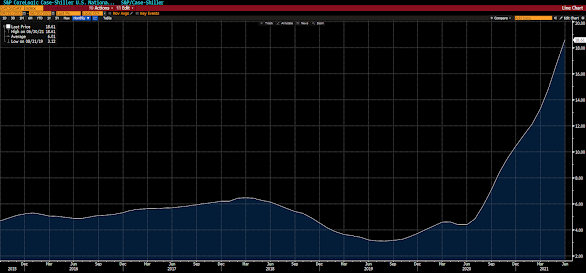

As we know, single family home prices have increased markedly over the past year, to put it mildly:

Case-Shiller Home Price Index Year-On-Year % Change:

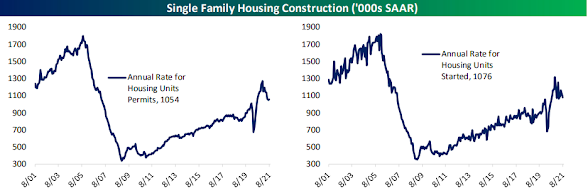

So then, it would make perfect sense to see single-family housing permits and starts rising through the roof, so to speak (pardon the pun). Well, not so much, of late:

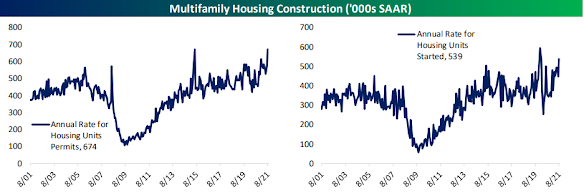

Ah, but multi-family’s another story, of late:

Now, the latter — given soaring rents — makes perfect sense, right? Rising prices for a good or service inspires higher production.

But what about the former? What gives with the single-family market?

Well, according to Bespoke Investment Group (the provider of the permits and starts charts above), it’s largely about supply bottlenecks that are uniquely (compared to multi-family) constraining to single-family construction.

I suspect that’s true, to some degree, but I’m wondering if it’s not also about some doubt around the sustainability of present single-family home prices, versus the present rent dynamic — the latter perhaps being viewed, indeed, as sustainable; which supports our longer-term inflation thesis…

Time will tell…

Today’s Fed decision day. There’ll be no change in the fed funds rate, but there’ll be plenty of talk around tapering bond purchases, inflation expectations and so on. Markets could move notably, one direction or the other.

Asian equities were mixed overnight, with 7 of the 16 markets we track closing lower (2 were shuttered).

Europe’s rallying big so far this morning, with all 19 bourses we follow notably (save for Turkey [flat]) in the green.

U.S. stocks are up nicely as well: Dow plus 333 points (0.98%), SP500 up 0.78%, SP500 Equal Weight up 1.17%, Nasdaq 100 up 0.53%, Nasdaq Comp up 0.55%, Russell 2000 up 1.11%.

The VIX sits at 22.06, down 9.44%.

Oil futures are up 1.90%, gold’s down 0.11%, silver’s up 1.22%, copper futures are up 2.48% and the ag complex is up 0.82%.

The 10-year treasury is up (yield down) and the dollar is flat.

Led by uranium miners, energy stocks, metals miners, metals futures and Viacom — but dragged by gold and inflation protected treasuries — our core portfolio is up 0.90% to start the session.

Herein and in client meetings I continue to find myself stating that — with regard to our current portfolio positioning — 5 days, 5 weeks, even 5 months out, I dunno. 5 years out, however, I have high confidence. The overall setup (debt, demographics, policy, societal trends, inflation prospects, geopolitics, etc.), as we sit here today, offers some serious clarity (in our view) in terms of longer-term probabilities.

What I’m essentially saying is that I’m certain we’re taking — given all available information — very good shots right here.

Now, that said, having done what I do for over 37 years, I remain very cognizant of the fact that even the best of decisions (based on all available information) — while making them consistently measurably improves the odds — don’t always result in the best of outcomes. I.e., as markets are dynamic, so must be our analysis.

“…on average, good decisions are more likely to result in good outcomes than bad decisions. They cannot ensure good outcomes, but they increase the chances of good outcomes. If you consistently employ good decision processes, you will accumulate better outcomes over the course of many decisions. Over the course of years, this can make a huge difference in your quality of life.”