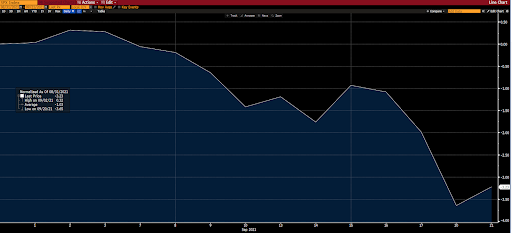

So it’s September, the only month of the year that over the long-run sports a negative average annual return for the S&P 500 Index. And, so far, September 2021 hasn’t disappointed.

9/1 to current:

Although a -3.23% showing thus far is certainly nothing to freak out about.

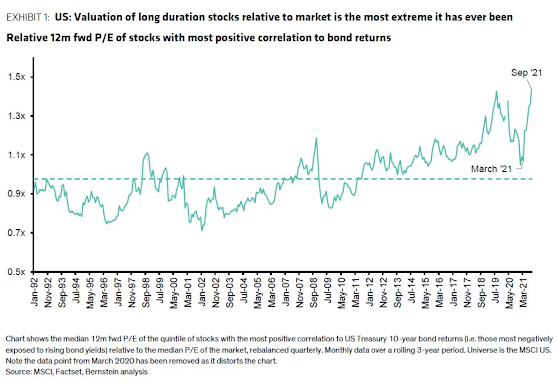

But maybe the fact that, per Bernstein’s quant team, the longest duration stocks (read tech) are trading at an all-time high 30% valuation premium to the overall market (HT Daniel DiMartino Booth) is indeed something to freak out about:

Or perhaps we should be freaking out over the plethora of market top signals that presently exist. Such as:

High valuation multiples, high corporate leverage, central banks (some) beginning to tighten, leading economic indicators rolling over, recession risk denial among economists, ISM new orders to inventories rolling over, yield curve flattening, negative technical divergences, bears capitulating and buying in, low quality IPOs aplenty, large share buybacks continuing, no shortage of M&A, high margin debt…. on and on!

Or, as was ostensibly the case on Monday, the threat of a credit/property bust in the world’s second largest economy (Evergrande/China)!

I of course could go on — abounding political/policy risk, yada yada — but suffice to say that uncertainty is indeed palpable as we sit here today.

Okay… So, uncertainty’s certainly thick, but what if anything do we indeed know for certain.

And we know that real property comprises the highest % of Chinese household net worth (74%!!).

Now think about the incentives/constraints/pressures the above two realities place on the economic/financial market impacting decisions of each nation’s respective politicians/policymakers!

If you’re thinking that those last two points do not a fundamentally bullish case make, particularly amid the historic toppy-ness of today’s markets, I couldn’t agree more. So I’ll try a bit harder.

Being that really bad bear markets tend to be things of recessions, the fact that employers are desperate to hire (10+ million US job openings presently), that our proprietary macro index reads +15 (odds favor expansion going forward), that ISMs (purchasing manager surveys) in both the manufacturing and services spaces are comfortably above 50 (the dividing line between recession and expansionary conditions), and so on, says that, for the time being, we shouldn’t be losing too much sleep over the risk of something ’08 or tech bubble-ish.

Now, that last paragraph said, there’s this thing called reflexivity that says a major financial market meltdown could indeed bring the economy right down with it.

And make no mistake, the Fed is uber-sensitive to what they call “the wealth effect” (people do stuff [spend] when they feel wealthy!). I.e., with all that household net worth tied up in such a toppy stock market, well, you can bet that the Fed’s board members are indeed sleeping uneasily these days… Fearing a reflexive economic jolt should they misstep and induce a selling panic…

So, clients, if you’re at all wondering what keeps us so stubbornly and actively hedging our (your) major downside exposure these days, well, there you have it!

But what about beyond (amid even) these days, are there not opportunities (long-term in nature perhaps) to be exploited nevertheless — the risks outlined above notwithstanding?

In a word, yes.

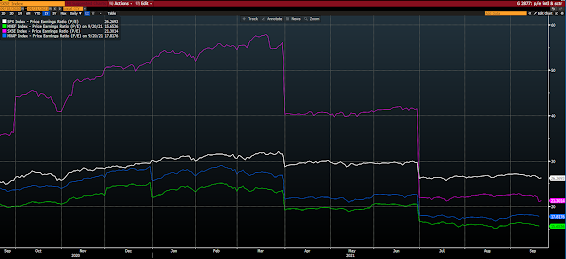

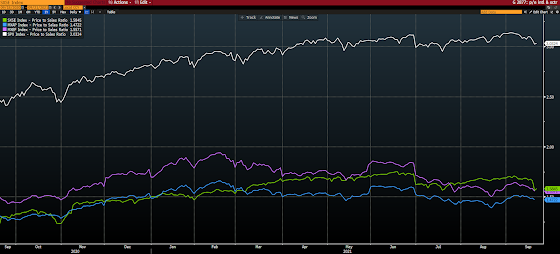

For one, as I’ve pounded on extensively herein for easily the past year, present U.S. economic constraints simply do not allow for a higher-trending dollar in the years to come. That, plus absolutely abysmal multi-year relative performance (next chart), more attractive valuations (the following 3 charts) and, not to mention, higher yields (last chart) — and various country-by-country idiosyncrasies — make non-US equities unusually attractive to us right here.

S&P 500 (white), Asia-Pac (blue), Eurozone (green) and emerging market (purple) equity returns from the bottom of the Great Financial Crisis (2008) to current:

Price-to-earnings ratios:

Price-to-book ratios:

Price-to-sales ratios:

Dividend yields:

What else? Commodities, energy related in particular…

Let the following from Bloomberg sink in: emphasis mine…

“The era-defining shift from fossil fuels to clean energy will deliver an unprecedented new boom for commodities—and an opportunity for investors—as a range of relatively obscure materials become essential to delivering emissions-free power, transport and heavy industry.

The transition could require as much as $173 trillion in energy supply and infrastructure investment over the next three decades, according to research provider BloombergNEF, and will reverberate from lithium-rich salt flats in Chile to polysilicon plants in China’s Xinjiang region.

As electric vehicles supplant gas guzzlers, and solar panels and wind turbines replace coal and oil as the world’s most important energy sources, metals like lithium, cobalt and rare earths are on the brink of rapidly accelerating demand, along with more familiar industrial materials like steel and copper.”

“Though shifting demand patterns are being signposted far in advance, project developers urgently need to secure capital for new mines or production lines. Efforts to lift supplies of key raw materials—which can require years of exploration and construction—must begin now to keep pace with future requirements. That pressure could be most pronounced for EV charging infrastructure and lithium-ion batteries, which face steep growth curves, though more established solar and wind sectors have been challenged this year by pricier commodities.”

“That pressure could be most pronounced for EV charging infrastructure and lithium-ion batteries, which face steep growth curves…” Ya think? Here’s what popped up when I Googled “Electric vehicles 2021”:

Here’s more:

“Solar panels with the power capacity of a gigawatt need about 18.5 tons of silver, 3,380 tons of polysilicon and 10,252 tons of aluminum, according to BloombergNEF estimates.”

“Wind turbines and infrastructure with the power capacity of a gigawatt need about 387 tons of aluminum, 2,866 tons of copper and 154,352 tons of steel, according to BloombergNEF estimates.”

“Lithium-ion batteries able to store 1 gigawatt hour of energy require about 729 tons of lithium, 1,202 tons of aluminum and 1,731 tons of copper, according to BloombergNEF estimates.”

“A fast, public electric vehicle charger typically needs 25 kilograms of copper, while a smaller charger to use at home needs around 2 kilograms of copper, according to BloombergNEF estimates.”

“As the energy transition supercycle gets closer, a major question is whether miners, financiers and governments can mobilize enough capital fast enough to bring on new supplies in line with demand. That means raw materials and the companies that produce them should offer higher returns—though also more risk—than component manufacturers, equipment makers or electric car producers, according to Pala’s Fung.

“It doesn’t matter what battery chemistry you have, lithium is needed across all of them, and nickel is needed in many of them,” she said. “If it’s solar or wind or EV charging units, you need copper to connect it all together—that’s why we like looking at these commodities.”

The world’s biggest mining firms, including BHP Group and Glencore Plc, are emphasizing their links to clean energy, while smaller competitors are surging. Lithium producers including Pilbara Minerals Ltd. and Orocobre Ltd. are advancing faster this year than battery giants like Contemporary Amperex Technology Co. and are among the top performers in the Bloomberg Electric Vehicles Total Return Index.

Still, green-focused equities have stumbled before. Valuations of solar equipment makers plunged from a 2007 peak, and lithium miners suffered more than two years of losses through early 2020 before resuming gains.”

Per that last paragraph, yes, patience and diversification are always key!

I have more dialed up but this one’s getting long in the tooth, and I want to keep you engaged… Saving the rest for later…