531k new jobs, 80k above expectations, with the two previous months revised by an additional 235k.

The unemployment rate came in at 4.6% (down .2%), while the participation rate, however, concerningly remained unchanged 61.6%.

The manufacturing space added 60k. Construction another 44k. Leisure and hospitality up 164k. Professional business services added 100k.

Wages overall rose by 4.6% annually.

Economist Peter Boockvar, in frank fashion, summed it up with a jab at the Fed that yours truly happens to sympathize with in his morning note:

“Bottom line, the number of unemployed is down to 7.4mm which compares to more than 10mm job openings as of September. After losing 22.3mm jobs last March and April, the economy has added back 18.2mm jobs. This, combined with wages now rising more than 5% on an annualized basis over the past 6 months on top of inflation just about everywhere makes the Federal Reserve look even more out of touch with policy relative to reality. Again, their idea right now of tightening is to take their balance sheet higher by another $500b about over the next 8 months and still have rates at zero.”

Listening to Bloomberg TV as the numbers came out this morning, and the equity market positively reacted, the commentary was all about stocks rallying due to the fact that while the data are good, there’s nothing there that’s going to sway the Fed’s dovish stance…. That these types of numbers are going to have to become the trend for quite some time before the Fed consequentially moves the needle.

Well, forgive my cynical tone, but that (that the fed will consequentially move the needle based on employment trends) is simply not my take.

You see, the consequentiality of the Fed consequentially moving the needle would express itself immediately and dramatically in the equity market (in a not good way for the bulls). And that my friends is simply not an option for this Fed.

I.e., suffice to say that, in my humble view, this utterly stock market-centric Fed is in no way interested in the porridge (data) showing up in any way hot. They need it Goldilocks to the point that they’ll tell us (their “forward guidance” tool) that the temperature’s plenty cool, even while they’re burning their tongues…

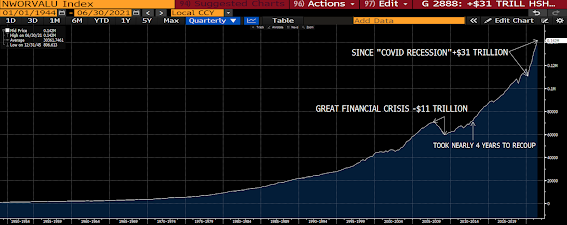

Why? Well, have a look at our chart of U.S. household net worth:

$20 trillion of that mind-boggling $31 trillion that has arrived on household (and non-profit organizations) balance sheets since March of last year is explained by the stock market!!

Imagine the economic (consumption) impact if what some justifiably view as an epic bubble were allowed to pop. Or, let’s say, imagine the heat the Fed will bear if, as is typically the case, they — by seriously tightening policy in response to robust jobs data — catch the blame for the popping…

Stay tuned, more on this mind-boggliness to come herein…

In contrast to what we’ve been reporting on most days of late, this morning’s early rally is being met by very good breadth. The US averages are higher across the board, with SP500 advancers leading decliners by ~7 to 1, nearly 2 to 1 for the Nasdaq Comp. Among major USequity sectors, healthcare is the only one taking a not-small hit this morning (down 0.68%).

Asian equities leaned green overnight, with all but 5 of the 16 markets we track closing higher.

Europe’s doing okay, on balance, this morning, with 11 of the 19 bourses we follow trading higher, as I type.

US major averages are rallying to start the session: Dow up 318 points (0.88%), SP500 up 0.76%, SP500 Equal Weight up 1.12%, Nasdaq 100 up 0.53%, Nasdaq Comp up 0.60%, Russell 2000 up 1.52%.

The VIX sits at 15.08, down 2.75%.

Oil futures are up 0.80%, gold’s up 0.32%, silver’s up 0.50%, copper futures are down 0.47% and the ag complex is down 0.41%.

The 10-year treasury is (interestingly, given this morning’s data) up (yield down) and the dollar is up 0.22%.

Led by MP (rare earth miner), Latin American stocks, oil services companies, banks and metals miners — but dragged by uranium miners, KRBN (carbon credits), solar, wind and healthcare stocks — our core portfolio is up 0.28% to start the day.

As clients and regular readers have no doubt gathered, we see politics/geopolitics as major influencers of modern day markets to a historic degree. Thus, we’re having to allocate notably more of our research time and budget to the study of political/geopolitical dynamics these days.