Like I keep saying, there are too many similarities between today and the early 2000s to sit back and accept the “it’s different this time” mantra coming from Wall Street.

Now, indeed, perhaps it is (different this time), but even the present-day arguments in that regard are eerie echoes of the tech-inspired mantra of the late-90s.

Fiddling around with graphs this morning, something’s jumping out at me…

Take a look…

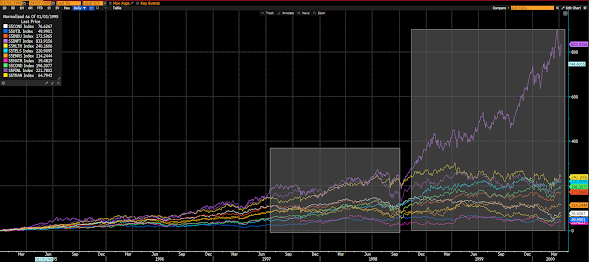

Here are the S&P major sectors % changes during the 5 years leading into the early 2000s tech disaster. Note the gaps forming leading into the 1998 19% correction, then the massive divergence (tech leaving the pack, especially) before the S&P got sliced in half, and the Nasdaq imploded into a devastating -85% 3-year freefall:

How about the period leading up to the Great Financial Crisis of 2008, when the S&P 500 gave up 57% of its value over ~17 months:

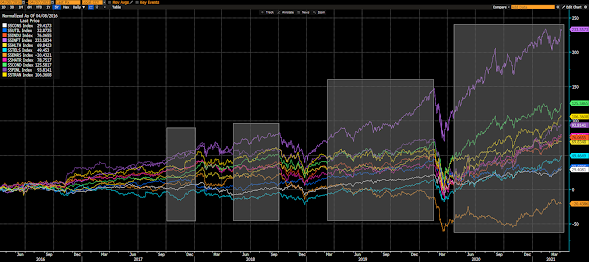

And here we capture the 5 years that included 10% and 19% corrections in early and late 2018, the 35% hit last year, an where we presently stand:

So, am I predicting something epic to the downside from here? Nope. I’m predicting no such thing. Just assessing setups and risks (i.e., risk/reward setups)…

Am I saying that the present setup, nevertheless, has me wanting to mix non-correlated (to stocks) assets into our clients’ portfolios and to hedge huge downside with options. Of course!! Which indeed we are…

Asian equities traded mixed overnight, with 6 of the 14 (that were open) markets we track closing lower.

Europe’s leaning lower so far this morning, with 11 of the 19 bourses we follow currently in the red.

U.S. major averages are mixed: Dow down 32 points (0.09%), SP500 up 0.05%, SP500 Equal Weight down 0.37%, Nasdaq 100 up 0.23%, Russell 2000 down a not-small 1.12%.

The VIX (SP500 implied volatility) is down 3.75%. VXN (Nasdaq 100 i.v.) is down 0.21%.

Oil futures are down 1.25%, gold’s down 0.06%, silver’s up 0.24%, copper futures are down 1.25% and the ag complex is up 0.41%.

The 10-year treasury is up (yield down) and the dollar is down for the 5th straight session (recall our technical dollar call from last week’s video), albeit barely, by 0.07%.

Led by MP (rare earth miner), ag commodities, tech, energy, the yen and silver — but dragged by ALB (lithium miner), solar stocks, uranium miners, emerging market equities and materials — our core mix is off 0.21% to start the session.

Yes, we study markets, in the most exhaustive fashion, but — as markets are merely the reflections of the decisions of humans — we study human behavior patterns ad nauseam as well. Particularly how we humans behave when we crowd together, as that’s when strange and wonderful (and not so wonderful) market events tend to occur:

“It is only by obtaining some sort of insight into the psychology of crowds that it can be understood how slight is the action upon them of laws and institutions, how powerless they are to hold any opinions other than those which are imposed upon them, and that it is not with rules based on theories of pure equity that they are to be led, but by seeking what produces an impression on them and what seduces them.”