So, possibly as early as this weekend a lot of folks are going to receive a very nice injection of cash into their bank accounts. While we can get into the whys and the wherefores and pontificate on need, inflation, distortion, yada yada, we’ll just for now acknowledge that such government largesse to this point has been very bullish for the stock market.

In fact, if you believe the polls, a not-small percentage of what’s coming to folks’ bank accounts will be immediately transferred to their online trading accounts — to buy the stuff that the now-famous ARK ETF complex is loaded up on.

Interesting, I must say, that, in light of the above, the Nasdaq 100 Index is nevertheless down a big 1.60% as I type.

Ah, but, you know, we’ve been preaching ad nauseum of late that tech stocks (well, ultimately, most sectors, actually) simply cannot handle higher interest rates.

So, okay, let’s go ahead and touch on just a couple of distortions that come from too much government intrusion into market functions.

I.e., take a look at interest rates so far this morning:

10-year treasury yield:

And while the dollar has been stubbornly resistant of late to matching the move in interest rates, that’s not the case this morning.

U.S. Dollar Index:

Remember, as we also keep preaching, in the grander, longer-term, scheme of things, stocks can’t do a higher dollar either. And, therefore, neither can the Fed…

I.e., this keeps up and you’ll see some serious (well, even more serious) intervention into both (interest rates and the dollar) — and, initially at least, stocks will love it — and so will our commodities exposures. The latter being a more logical fundamental play…

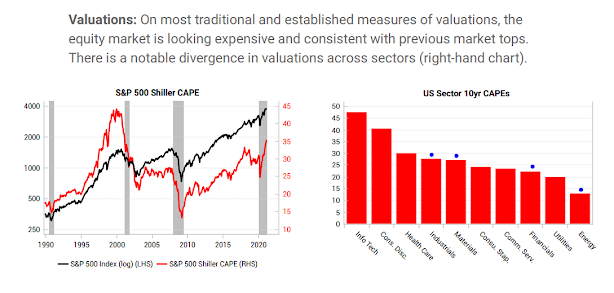

In this week’s video message I touched on the general setup for the tech sector (not good) versus others in which we hold larger positions (decent). Premium research provider Variant Perceptions supports what we’re thinking, from a valuation standpoint.

The tech sector’s CAPE P/E (historically expensive) is the first bar on the left, I blue dotted the 4 sectors I featured in the video:

We also took a technical look at the Nasdaq 100 Index.

Here’s an updated, zoomed-in, peek.

Note that the index bounced strongly off that 2nd support level, but stopped yesterday right at the 50-day moving average. It’s failing it so far this morning:

The S&P 500, by the way, is struggling (although less so) this morning as well — and, per the below (yellow circles), it’s threatening to carve out a potentially-nasty double top:

Now, technicals notwithstanding, given that the factors presently weighing on stocks are factors that the market believes the Fed can effectively manipulate, odds — in the short-run — probably favor yet more upside from here, with of course some major volatility (both directions) along the way.

Asian equities were mixed overnight, with 7 of the 16 markets we track closing lower.

Europe’s leaning slightly red so far this morning, with 11 of the 19 bourses we follow trading lower.

U.S. major averages are mixed to start the day: Dow (read Boeing) up 97 points (0.30%), SP500 down 0.43%, SP500 Equal Weight up 0.21%, Nasdaq 100 down 1.72%, Russell 2000 down 0.06%.

The VIX (SP500 implied volatility) is up 1.96%. VXN (Nasdaq i.v.) is up 6.99%.

Oil futures are down 0.36%, gold’s down 1.24%, silver’s down 2.31%, copper futures are down 0.97% and the ag complex is down 0.52%.

The 10-year treasury is getting creamed (yield screaming higher) and the dollar is up a big 0.59%.

Our core portfolio’s leaders this morning are AT&T, banks, financials, Verizon and industrials. Our biggest losers are MP (rare earth miner), solar stocks, emerging market equities, silver and gold. All in, we’re off 0.47% to start the session.

As clients and long-time readers know, among all of history’s market players, Jesse Livermore tops my list of those worth studying. I sometimes wonder if it has something to do with a common passion?

“There is time to go long, time to go short and time to go fishing.”