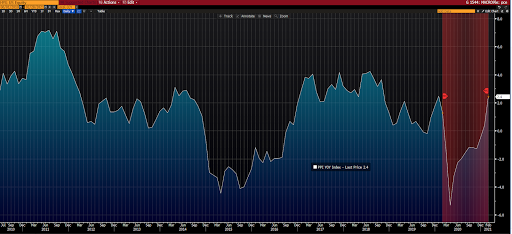

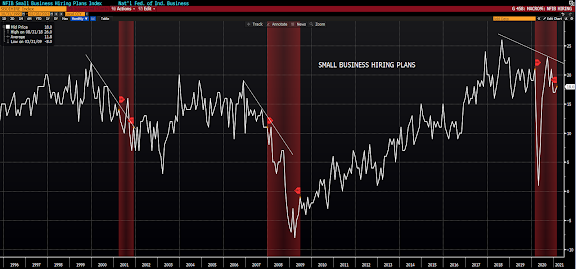

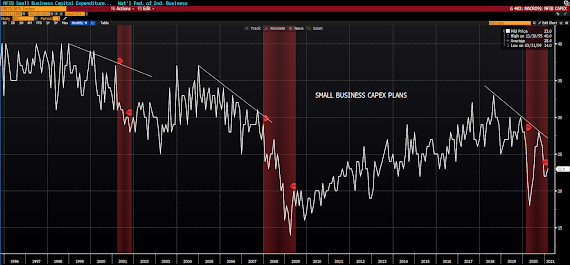

The steady ascent of late of our proprietary macro index took a pause this week, with our overall score remaining at +16.33:

“The coronavirus [COVID-19] pandemic is affecting us in terms of getting material to build from local and our overseas third- and fourth-tier suppliers. Suppliers are complaining of [a lack of] available resources [people] for manufacturing, creating major delivery issues.” (Computer & Electronic Products)

“Supply chains are depleted; inventories up and down the supply chain are empty. Lead times increasing, prices increasing, [and] demand increasing. Deep freeze in the Gulf Coast expected to extend duration of shortages.” (Chemical Products)

“Steel prices have increased significantly in recent months, driving costs up from our suppliers and on proposals for new work that we are bidding. In addition, the tariffs and anti-dumping fees/penalties incurred by international mills/suppliers are being passed on to us.” (Transportation Equipment)

“We have experienced a higher rate of delinquent shipments from our ingredient suppliers in the last month. We are still struggling keeping our production lines fully manned. We anticipate a fast and large order surge in the food-service sector as restaurants open back up.” (Food, Beverage & Tobacco Products)

“Overall capacities are full across our industry. Logistics times are at record times. Continuing to fight through shipping and increased lead times on both raw materials and finished goods due to the pandemic.” (Fabricated Metal Products)

“Prices are going up, and lead times are growing longer by the day. While business and backlog remain strong, the supply chain is going to be stretched very [thin] to keep up.” (Machinery)

“Things are now out of control. Everything is a mess, and we are seeing wide-scale shortages.” (Electrical Equipment, Appliances & Components)

“Labor shortages at suppliers are affecting material deliveries and prices.” (Plastics & Rubber Products)

“We have seen our new-order log increase by 40 percent over the last two months. We are overloaded with orders and do not have the personnel to get product out the door on schedule.” (Primary Metals)

“A sense of urgency is being felt regarding new orders. Customers are giving an impression that a presence of stability is forthcoming and order flow is increasing.” (Textile Mills)

“Prices are rising so rapidly that many are wondering if [the situation] is sustainable. Shortages have the industry concerned for supply going forward, at least deep into the second quarter.” (Wood Products)

A couple other inputs to our analysis, while not needle-movers, worth discussing are…

Overall (slight uptick):

“… there has to be a realization that all the fiscal stimulus in the United States is transitory, it will lead to a two-quarter boom and then a bust into 2022 as the withdrawal takes over. Either that, or President Biden and his band of Keynesian interventionists will have to continue to prime the fiscal pump that much harder. Or else, six months from now, we will be talking about a fiscal cliff even as the economy recovers.”

Speaking of Dave, while I have great respect for his work, and sympathize with his concerns highlighted above, he’s firmly in the camp that sees the present pickup in inflation — given the enormous debt burden weighing on the economy, the still crazy-high unemployment, the gaping output gap (potential GDP vs reality), etc. — as entirely temporary. Well, I’m personally not in that camp…

As, per my commentary the past several months, my present view more aligns with Chetan Ahya’s, as expressed in Tuesday’s Financial Times:

“As demand surges, so will inflationary pressures. But will this be a transitory phenomenon or lead to a more sustained rise?

I would argue that the driving forces of inflation are already aligned and a regime shift is under way. The change in the conduct of fiscal policy is pronounced. This time, active fiscal policy has gone well beyond filling the output hole. To date, US households have lost $490bn in income but have received $1.3tn in transfers. The total amount of transfers will undoubtedly rise with the passage of the next fiscal stimulus package.”

Time will definitely tell…