Deere knocked earnings out of the park (we like industrials right here!) and global manufacturing PMIs showed encouraging improvement overnight. “Stimulus” by the boatload is on its way and the new treasury secretary keeps saying that we simply can’t go too big on government spending going forward, “now’s the time!”

Uh oh!!

So why the “Uh oh!!”?

Here’s from this week’s main message:

“…we are about to see, far and away, the greatest coordinated assault on recessionary conditions, on financial market risk, and, frankly, on capitalism, the world has ever seen.

A nearly $2 trillion “stimulus” package is about to be passed, followed later in the year by a several (likely ~3) $trillion infrastructure plan.

While the prospects for fiscal spending sounds bullish for equities, given, among other things, what was a primary driver of stocks throughout the longest bull market in history, there’s serious risk in that narrative.

I.e., I’m in the camp that believes that the coming epic combination of fiscal spending and monetary easing (involving the Fed buying up the treasury issuance that’ll fund the fiscal largesse) will spark a potentially not-small round of inflation that will naturally do a real number on the bond market; read higher interest rates!

The fact that the equity market has feasted on historically low interest rates, and that present valuations can only be justified by, yes, historically-low interest rates, means that those high growth names’ in particular will simply not hold up against a rising discount rate.

Note the action in Apple vs the 10-year treasury yield:”

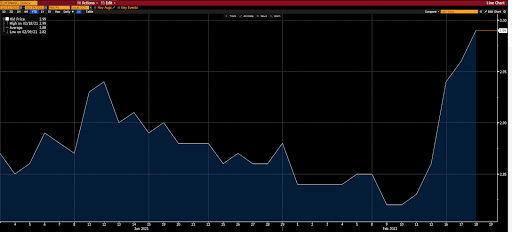

Here’s the 10-year treasury yield so far this morning:

“We’ll (in diversified fashion [which includes cash and ultra-short-term fixed income securities]) emphasize the cyclical value plays that are destined to take the most advantage of what’s to come: Materials (including miners), industrials, financials & energy (including renewables) will be our top U.S. equity sector weightings. Commodities (including gold — given the prospects for deeply negative “real” yields) are a no-brainer. And non-US equities represent unusual value amid what virtually has to be a weak-dollar environment (on a trend basis) well into the foreseeable future.”

Nietzsche warned us about the Fed (and the treasury):

“…as soon as ever a philosophy begins to believe in itself. It always creates the world in its own image; it cannot do otherwise; philosophy is this tyrannical impulse itself, the most spiritual Will to Power, the will to “creation of the world,” the will to the causa prima.”

Have a nice day!

Marty