In our client review meetings these days I of course expound on much (the good and the bad) of what you’ve read herein, and when it comes to the historic chasm that separates current stock prices from underlying fundamentals I typically declare that the major averages would need to decline by easily two-thirds (a bit more than the ’08 experience) to catch down to present reality.

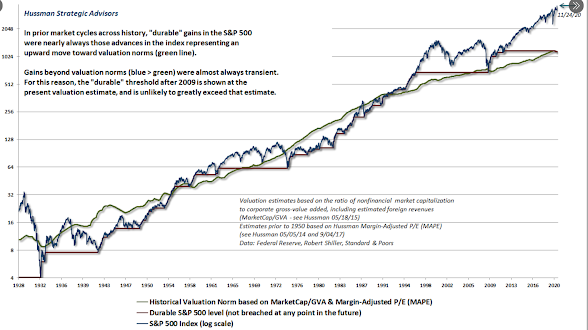

“In prior market cycles across history, “durable” gains in the S&P 500 were nearly always those advances in the index representing an upward move toward valuation norms.

Gains beyond valuation norms (blue>green) were almost always transient. For this reason, the “durable” threshold after 2009 is shown at the present valuation estimate, and unlikely to exceed that estimate.”

Now, does this mean we need to brace for ultimately a 2/3rds hit to stock prices? Not necessarily, it simply says that stocks are very expensive right here, which is a scenario that can indeed last a very long time. It does, however, support our view of the risks inherent in the present setup. And, along with our general macro concerns, exemplifies the need to hedge our equity exposure…

Be sure and read this week’s message, posted earlier today, when you have a chance. There’s much to parse, some of it historically unique, in both the short and long-term market setups…