“The real opportunities in macro, you have to wait for. You don’t always have to be doing something.

Having lived a few of these markets before, you have to be very careful because you can lose P&L very quickly by getting too excited.”

–Raoul Pal, 10/9/2020 RealVision Daily Briefing

Raoul is RealVision‘s founder and CEO, and one of today’s great macro thinkers. Of course I’m quoting him today because, as clients and regular readers know, his comments echo our present thinking…

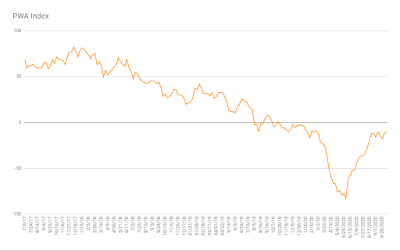

This week marks the second consecutive improvement in our macro index’s net overall score; rising 2 points to -10.

One of our inputs moved from negative to neutral, while the rest essentially held steady (although per the following, a few are starting to look suspect).

That one gainer was the Bloomberg Commodity index:

Now, while -10 is a far cry from the -83 score back on June 1st, we have to remain cognizant of the debt/government spending-fueled nature of the improvement.

I.e., particularly as “stimulus” measures pause or abate, it makes sense, while still mired in recession, that we’ll begin to see some of our indicators roll back over.

Which may presently be the case; here are three examples:

Latest job openings report:

Heavy truck sales:

Global Purchasing Managers Index:

Conducting a client portfolio review via Zoom this afternoon I found myself exclaiming that “if you’d told me at the beginning of this year that right now we’d be witnessing 840,000 weekly new unemployment claims while 11 million other folks are already on the rolls, I’d have told you that stocks would be down at least 50%.”

And, make no mistake, I also would have fully expected the Fed to be printing like mad and the government to be borrowing and spending like there’s no tomorrow (i.e., that stuff I would’ve gotten right).

Ah, but I would not have expected — because it was illegal at the time (well, technically still is) — that the Fed would be able to buy corporate bonds, junk-rated ones no less, and, thus, leave people with legitimate reason to believe that there’s absolutely no place they ultimately won’t go to keep markets from clearing (Federal Reserve Act constraints be damned!) — which given the debt mess we came into this recession with (before I could even spell coronavirus) would ultimately be destined to exacerbate the worst recession since the Great Depression.

Well, we indeed have the latter, but, thus far, we haven’t remotely experienced the clearing necessary to allow markets to emerge in any semblance of decent shape.

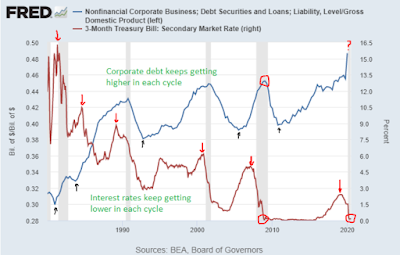

So why might I have previously proclaimed that the next recession would be the worst since the Great Depression? Well, among other things, charts like the following two:

My black arrows point to how after the past several recessions (grey shaded areas) total corporate debt cleared only to a point that left more on the books than the bottom of the one prior. My red arrows point to how interest rates peaked at a lower spot than they did at the peak of each prior expansion. My red circles point to how interest rates rested at zero when debt peaked during the 2008 worst recession since the Great Depression, which is where they essentially sit currently, while debt, alas, ramps ever higher:

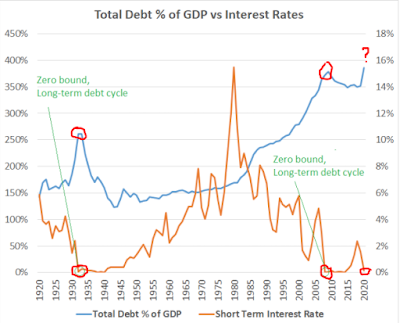

And here’s the proverbial icing on the cake.

My red circles are where debt peaked during the Great Depression and where interest rates were at the time; where it peaked in 2008 and where interest rates were at the time; and, alas, where interest rates currently sit — the level where debt will peak this time is yet to be determined:

Just imagine what might occur in financial markets given current (and rising) debt levels should the economy indeed show the kind of strength that would typically inspire a higher interest rate regime.

Yep, you got it, utter financial market disaster! I.e., the enormity of the debt is simply more than rising revenues in a better economy — with rising interest rates — can, in the aggregate, ultimately service, without perpetual government intervention that is.

So, yes, absolutely!!, the current setup has me very concerned about what’s in store! Yet it also has me (us, as a firm, actually) very cognizant of virtually all the Fed can/will do in their desperate effort to kick the proverbial can down the proverbial road.

While I have quite the number of additional visuals assembled to convince you that we’re on the right track, if you’re our client and/or a regular reader, I’m assuming we’ve already succeeded in that endeavor. Plus, it’s late on a Friday evening, and I’m starting to feel it 😑.

So I’ll make it easy on me, and you, and copy and paste, from our internal log, a synopsis of our current general thesis. This was penned before the Fed altered their inflation mandate; note in paragraph two that we anticipated that they would:

“Given all that’s evolved over the past several decades, given the complete carry-dependent state of the global economy, there’s only one road for the powers-that-be to take going forward; a steady, unrelenting debasement of the US dollar.

Virtually everything the Fed has signaled since the fallout in Q4 2018 assures that all appetite for volatility has been essentially purged from their thought processes. COVID, ironically, has given them — they presume — complete cover to get the ball rolling sooner and more aggressively than what otherwise may have occurred. I see zero question that they’ll completely change their narrative/policy on inflation going forward, and engage in direct yield curve control indefinitely.

The treasury will issue debt without restraint and the Fed will purchase it likewise, indefinitely.

Commodities — gold especially — are the most obvious trade under these circumstances. US equities stand to ultimately benefit as well, however — and this will produce great anxiety for the Fed along the way (due to extreme global carry) — with bouts of extreme volatility, given the unavoidable economic stagnation such a scenario creates, and the potential for huge political disruption — regulation, taxation, etc. — as growing income/wealth inequality continues unabated (exacerbated, in fact) going forward.

Foreign market equities, emerging markets in particular, stand to outperform the US markedly for several years to come; but we — while we anticipate adding there incrementally in the near-term — are going to let the COVID situation and the coming election play themselves out before we go there in a big way.

The immediate question for equity markets being, given the abysmal state of macro affairs, political risk, geopolitical risk and so on, will there be the 50+% correction that will reset valuations, etc., to the point I believe necessary for the US market to recapture any semblance of a “fundamentally” investable setup — at all or anytime soon? Bottom line; that risk is there, which demands that we hedge our equity exposure against a major drawdown either until one occurs or until the risk abates…”