9/17/19 Tuesday

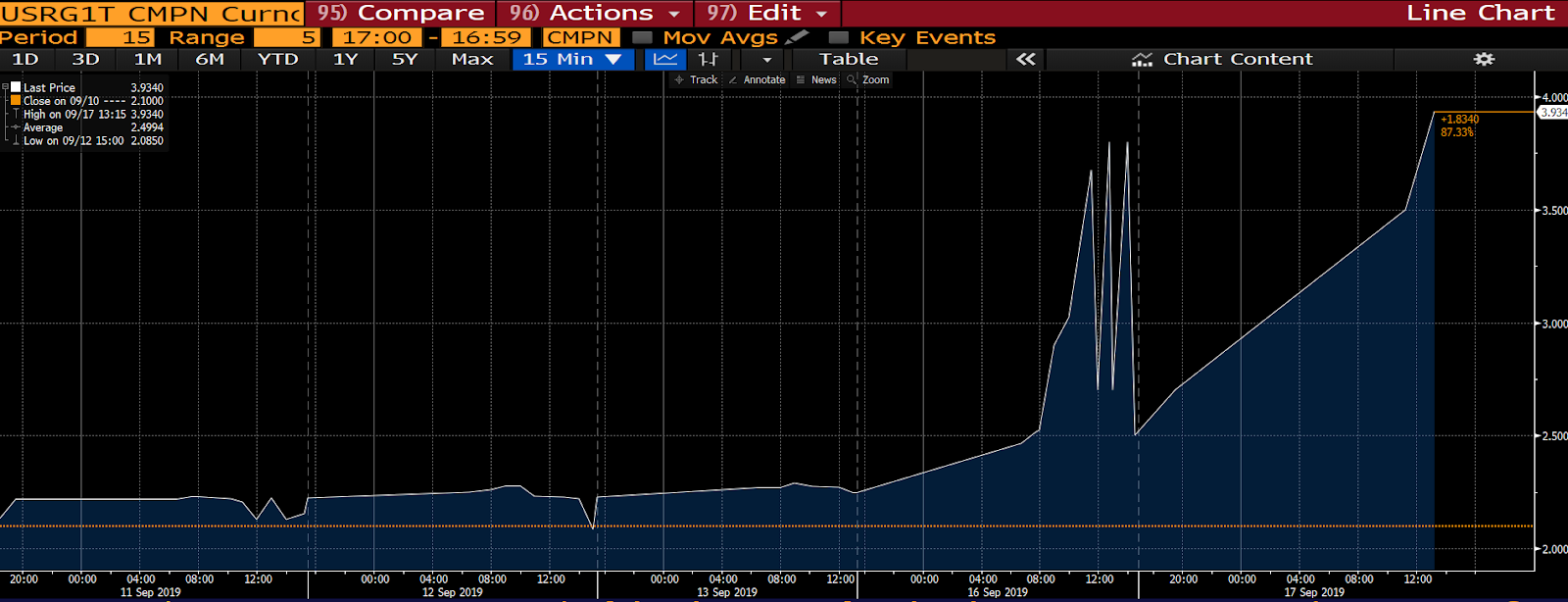

Something very weird is going on with overnight repo rates!

BTW: The “repo rate” represents the cost of one-day repurchase agreements (repos) between banks (one bank buys a security [a treasury] — essentially lends cash to the seller — with the proviso that the seller repurchase it [pay the cash back] the following day at a higher price [the difference in price equates to the “repo rate”]).

While there has been a plethora of explanations as to what’s going on, simply put, there is/was all of a sudden a serious lack of liquidity. The accepted excuse was the unfortunate timing of companies pulling billions from banks to pay their quarterly taxes, combined with the treasury borrowing $78 billion this week against only $24 billion of maturing debt. Plus, there’s a rumor that the Saudis pulled tens of billions over the past two days (needed to fund their efforts in dealing with the oil supply shock).

In any event, it serves as a clue that there exists the potential for a squeeze on liquidity that, taken to the extreme, could essentially freeze credit markets and create all manner of havoc in the financial markets and the economy!

Not to be an alarmist, and I don’t think there’s anything systemic here (at this juncture), but just another thing to keep our eyes on.

Yesterday I made the case that the Fed may come in dovish tomorrow and, thus, spark a rally in stocks. As I type we’re just over an hour from the close and the market is essentially flat. Clearly, traders are waiting on tomorrow.

Given the latest core CPI number, along with on balance better than anticipated data of late (the U.S. econ surprise index is back in the green) — and, not to mention, a friendlier tone regarding trade — you’d think that the Fed would come in hawkish, which of course contradicts my note yesterday.

Yesterday’s thought was mostly about the huge disruptive potential of heightened conflict in the Middle East. Despite today’s news that it appears as though there’s evidence that the attack was launched from Iran, there seems to be little stomach for a military response at this juncture. Otherwise, the stock market would for sure be trading down a bunch, and oil would be spiking (wti is down 5% as I type!). So, if the Fed shares the market’s apparent sanguineness, and takes the latest data and trade optimism to heart, scratch what I wrote yesterday; indeed they could come off hawkish, and the market could sell off in response.

But, then again, what about the repo rate issue?? If there is something sinister brewing there the Fed may want to get in front of it; which would make them dovish, which would be short-term bullish.

Let’s just call it 50/50 at this point…