I wonder if the members of The Federal Open Market Committee (the Fed) were too preoccupied by their discussions over the data today (day one of their two-day policy meeting) to take note of today’s data?

If not — if they indeed took a peak — those who favor little or no tweaking (the hawks) had to have looked at their dovish counterparts (those clamoring for a .50% rate cut) and said “see what we mean!”

Here’s Econoday’s commentary on Redbook’s Same Store Retail Sales Report: emphasis mine…

“At 5.4 percent, Redbook’s same-store year-on-year sales growth did slow 1 percentage point in the September 14 week but from the prior week’s extraordinarily strong 6.4 percent rate. Five percent sales growth, especially for same stores which exclude new store growth, is exceptional. This sample is offering an early indication of strength for the September retail sales report.”

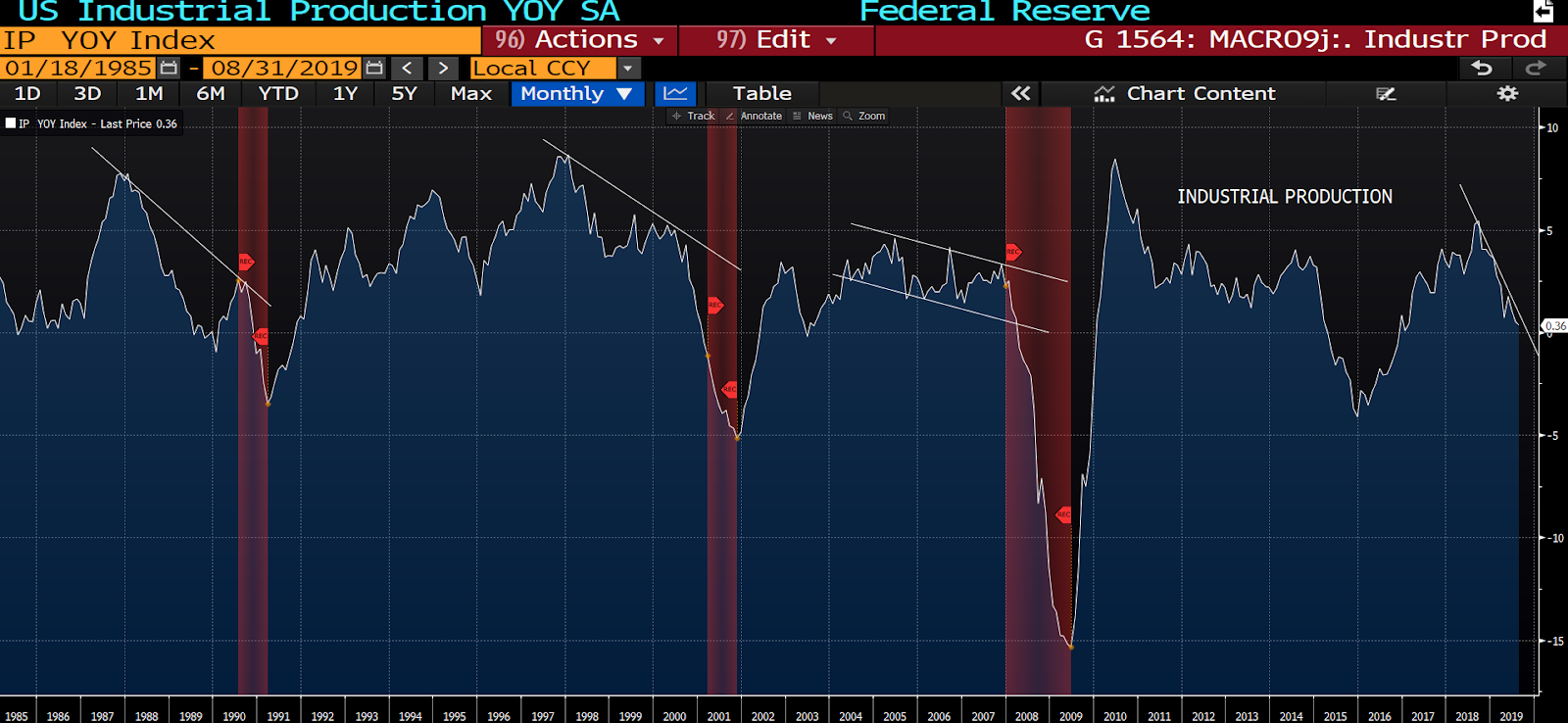

Here’s on Industrial Production:

“Showing broad strength in August, strength that will ease concerns at the Federal Reserve over weakness in manufacturing, industrial production hit the very top of Econoday’s consensus range with a 0.6 percent gain and the strongest showing of the year. Manufacturing production exceeded Econoday’s consensus range, at a 0.5 percent monthly rise and third gain in four months. This reading opened the year with four straight declines, three of which were very sharp including a 0.9 percent plunge in April.

Before turning back to manufacturing, the report’s other two major components also showed strength led by a 1.4 percent monthly jump in mining and a 0.6 percent rise for utilities. The rise in mining is of special note as this sector, after sharp acceleration in both 2017 and 2018, has had a flat year, notwithstanding August’s improvement. The rise underway right now in oil prices following the attack on Saudi production points to another month of mining strength in this report for next month.

But manufacturing, facing a slowing export market, is the concern for the Fed right now and August’s results, though only one month’s results, are very positive. Production of business equipment rose 1.0 percent in the month which should ease specific concerns at the Fed that slowing in global demand is cutting into business investment. Business supplies showed a sharp gain in August as did construction supplies. Other readings show gains for machinery, primary metals and fabrications (all part of the capital goods group) as well as gains for aerospace. Production of motor vehicles slowed in the month.

This report isn’t a game changer but it is an eye opener, one that may well cool the Fed’s enthusiasm for rate cuts, at least an outsized 50-basis-point cut. Watch tomorrow for the FOMC decision where expectations are firmly set for a 25-basis-point cut and the promise of at least one more such cut before year end.”

And here’s on Housing Market Index (homebuilder sentiment):

“Low mortgage rates are helping the housing sector, at

least for builders whose September housing market

composite index jumped to 68 to exceed Econoday’s

consensus range. The current sales component is the

source of September’s, up 2 points to a very strong 75

and offering a positive indication for coming new

home sales data as posted by the government. The

traffic component held unchanged at 50 which is actually

a good reading for this stubbornly weak component.

Sales six-month hence did edge 1 point lower but are

still strong at 70. Regional composite scores are led by

the two most important regions, the West at 75 and the

South at 70 with the Northeast at 59 and the Midwest at 57.”

Now, for our purposes, all three of the above are components of our proprietary macro index. As it stands, retail sales are already scoring in the green (+1), as is the housing market index; so neither of those will improve our indicator’s overall macro score. As for Industrial Production, while the month-on-month (today’s featured data point) is encouraging, on a year-on-year basis (our metric), it’s still a drag (per the chart below); hence, the “isn’t a game changer” point in Econoday’s commentary. But still, it could get the Fed’s attention…

U.S. Industrial Production YOY: