Question: Why, with all of this volatility, aren’t we moving client portfolios to a defensively biased allocation?

Answer: Because typically bear markets (20+% declines that take more than a few weeks to recover) occur amid economic recessions, and the data just doesn’t yet say “recession looming”.

That said, for a number of reasons, we have reduced client exposures to some cyclical sectors (tech primarily), as well as foreign equities, while increasing exposure to defensive sectors a bit over the past few months, but not nearly enough to suggest that we’re getting defensive in the aggregate.

As of this moment — despite the volatility — we’re not inclined to make any additional directionally defensive moves.

Here’s why:

While our PWA (Macro) Index (86 economic and financial market datapoints) just scored its 2018 low (+25.58), it remains safely above what we deem the recession-warning level (0-).

Here’s 20 years of back-testing (note the readings when the S&P 500 [white bars] was hitting all time highs right before the last two bear markets): click to enlarge…

Also note what a really bad idea it would’ve been to sell during any of the sizable dips when our index was scoring in the green.

The above alone suffices in terms of justification for our presently staying the course. But there’s more:

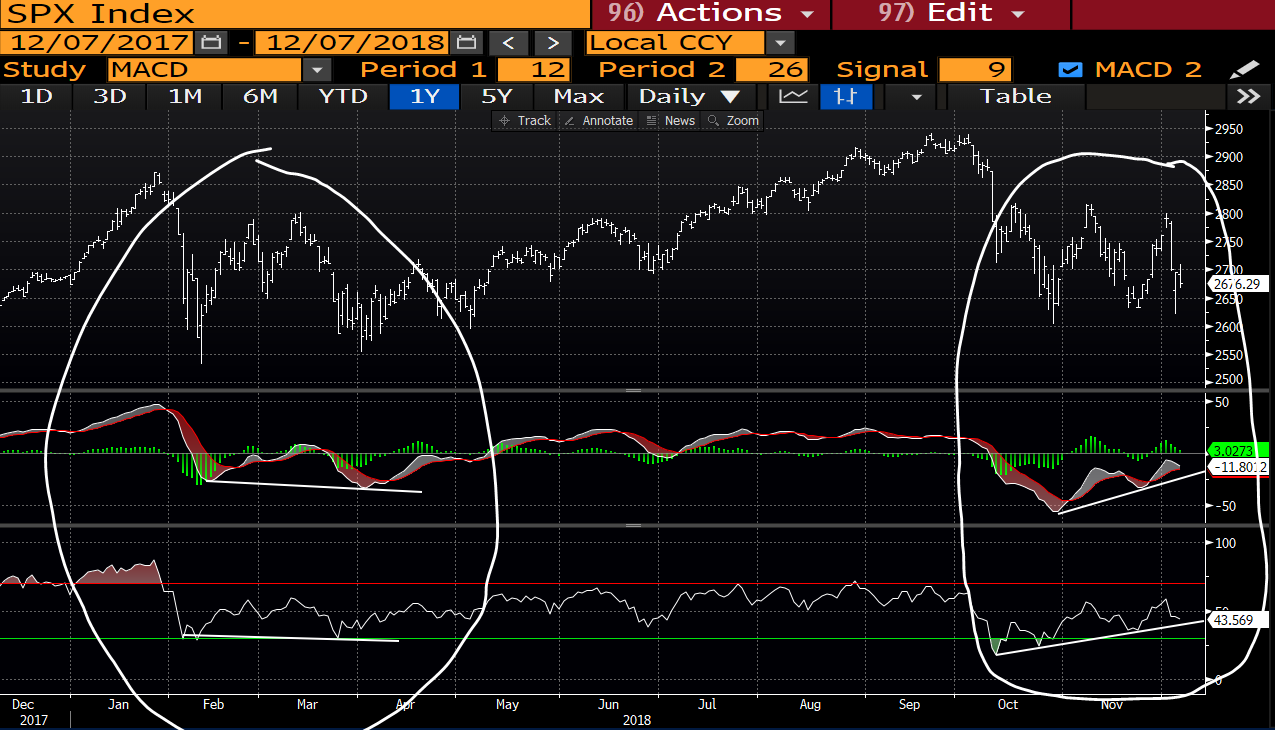

Per our 12/7 blog post, we’re also seeing a technical setup that looks remarkably like correction bottoms of the past. Here’s from that note:

Note the present bullish divergences in both the MACD and relative strength lines (momentum indicators) under the S&P 500 one-year chart,, and note how they looked during the correction earlier this year (not bullish):

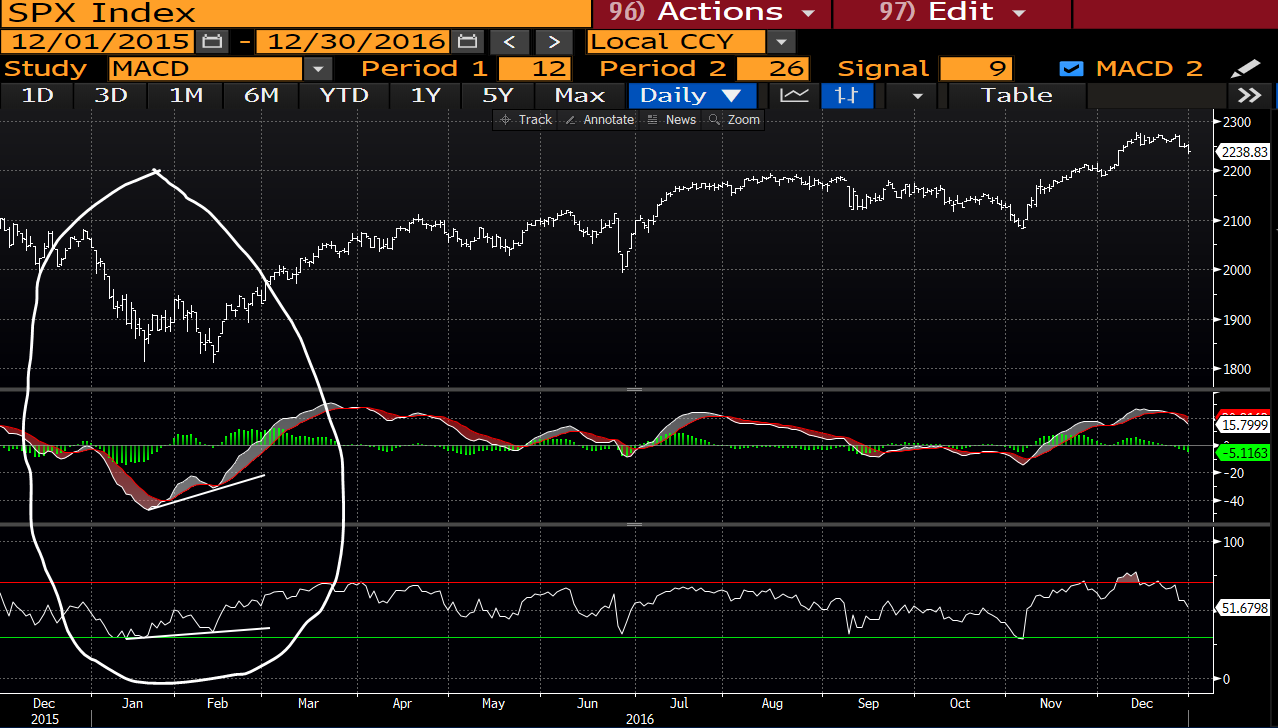

Here’s how they looked at the bottom of the early 2016 correction (worst start to a year ever):

And here’s how they looked at the bottom of 2011’s whopping 19% correction:

Here’s an up to date look (the setup remains):

Another encouraging sign is the presently discouraged state of the individual investor. The last time individual investors were this bearish (per the weekly American Association of Individual Investors weekly survey [a historically excellent contrary indicator]) was right at the bottom of the 2016 correction: click to enlarge…

I know, but this time has to be different! I mean we’re staring down a trade war, Fed rate hikes, a yield curve on the verge of inversion, and the possibility of a Presidential impeachment. No way the market can recover amid that kind of uncertainty!

Well, there are precedents you know. Take 1994-’95 for instance.

Here’s a video snip from money manager Chris Ciovacco’s weekly technical market analysis:

Once playing, click the icon in the lower right corner for full screen. Focus should occur after a few seconds; if not, click the wheel to the left of the YouTube icon to adjust:

In summary: While our primary focus in terms of positioning is always the state of general conditions, which presently has us sticking to our target weightings, we’re encouraged by current technical indicators that signal that we may (no guarantees!) see the bottom of the present correction in the not too distant future.

Keep in mind that we’re talking about probabilities, not certainties, so absolutely the presently positive setup can morph into a look that completely reverses our view of economic and equity market prospects. In which case we will indeed move to a net defensive allocation within client portfolios, regardless of where the stock market sits at the time. Again, that’s just not the signal we’re presently receiving…