For this week’s message I’ll share this morning’s two entries to our market journal, cleaned up for your reading pleasure. The first speaks to recent market volatility, the second to my thoughts on the energy sector:

363 point Dow drop was accompanied by selloffs in bonds and gold. I.e., save

for perhaps the 3.25% spike in the vix (although intraday it

was up nearly 7%) yesterday was anything but a panicky run-for-the-fences kind

of down day. For me yesterday’s action (in fact, much of the

heightened volatility of late) – save for last week’s early-week

turbulence that I attributed to protectionist rhetoric – supports the

notion (my notion for sure) that the bond bull market’s days

are numbered.

the stock market is going to have to come to terms with higher interest rates;

a factor that will call present valuation levels into serious question.

However, given where we appear to be in the economic cycle, where the Fed

appears to be in the tightening cycle, as well as the results of our ongoing

technical and fundamental analyses, history suggests (no guarantees mind you) that the present bull market in stocks has

a ways to run. If so, it’ll be the “climbing a wall of worry” scenario, it’ll

just be that the worry will be the market’s valuation level, which – despite

the attention it gets – is historically the absolute worst market-timing

indicator. Regardless, I have no doubt that it’ll be a rocky climb…

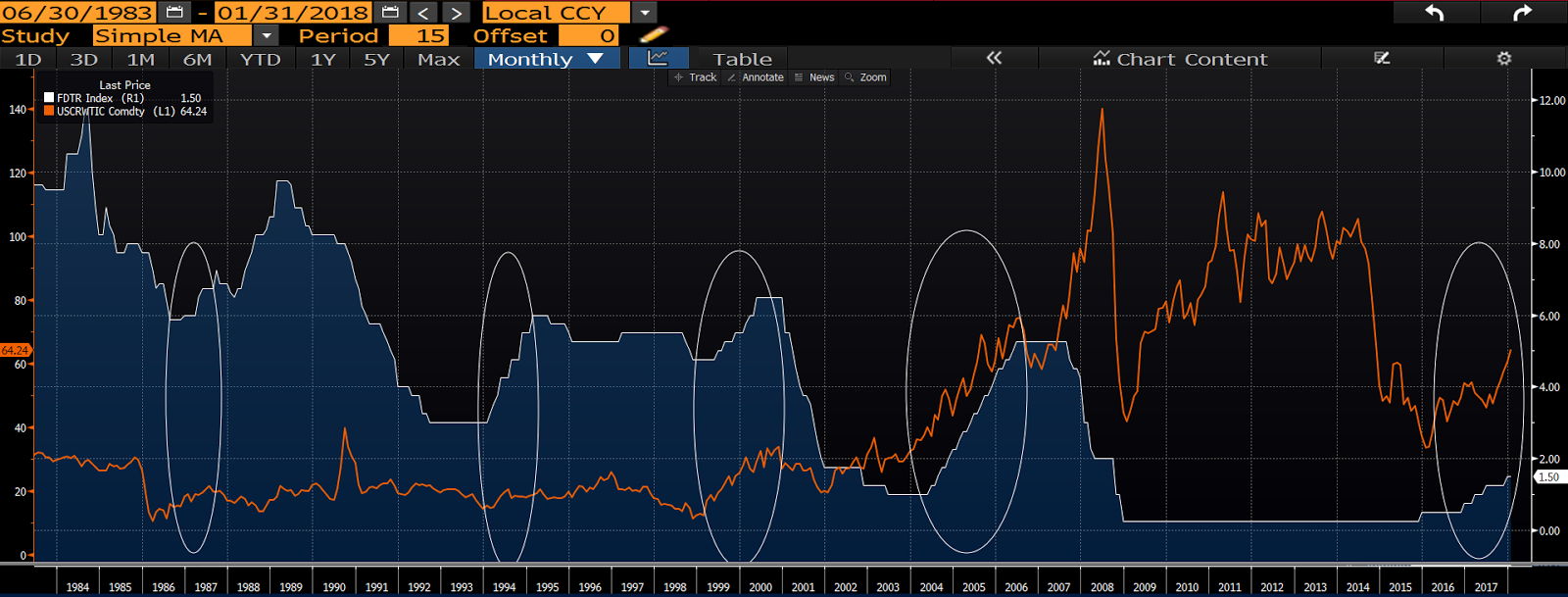

- I maintain that before the year’s out we could see a rally in the dollar that’ll be exacerbated by some

major short covering. - The Trump Administration is uber-friendly to oil production

(bearish for price). - OPEC and Russia’s production cuts (bullish for price) are

working and, thus, North American production is now screaming higher (bearish

for price). - OPEC can be wishy-washy when it comes to production quotas. Should

it abandon the current limit early, price would scream lower. - Total S.A. just made its largest discovery ever in the Gulf of

Mexico. - Kuwait’s KPC will spend $114 billion on capacity expansion over

the next 5 years. - Exxon Mobile has successfully cut costs in the Permian Basin to

the point that it now sees itself increasing production there three-fold.

doing exceptionally well, which for sure means high oil demand (bullish for

price). Plus, looking at previous Fed tightening cycles, oil tends to do well

(dramatically last three occurrences), particularly in the early stages:

fact that the Fed tightens when the economy is in good shape and inflation is heating up.

North America has never been a player like it is today!

(certainly their earnings) can do well in 2018, the question is are they positioned

as well as, say, financials (deregulation and higher rates), materials

(infrastructure the world over), industrials (ditto materials) and consumer

discretionary (tight labor market, rising wages, optimism)?

“4. Renewables: While the world will continue to

consume fossil fuels into the future, anyone who would deny the fact that the

industry faces major challenges, as the world pushes to clean itself up, is,

well, in denial. Thus, while we’ll indeed see geopolitical, etc.-induced spikes

in the price of a barrel from time to time well into the future, the

longer-term trend will indeed be a lessening of dependence on fossil fuels and,

thus, a massive structural rebalancing that, again, poses major challenges for

the industry in the years to come.”

December that I plug in at night. It uses gas too, but about half as much as

our last one. Oh, and we get a nice “clean energy” tax credit! And it’s amazing to drive (very

quick). I.e., I really like the feel when it’s in electric mode…

now take our energy target down a point to 7% and increase consumer

discretionary to 13%…