Brexit was a surprise, to say the least! Many folks, many whom I know, celebrated the Brit’s desire to chart their own course going forward. I can certainly sympathize. However, if they thought the breaking from a hard-fought trade union wouldn’t come home to roost on their economy… well….

While the Eurozone economy is clearly improving, the UK has major issues.

Here’s from Bespoke’s morning report:

Growth of consumer credit has stalled out at

about 1.5bn GBP/month (chart) while UK mortgage

credit is in a similar position at a ~3.5bn GBP/month

run rate despite some improvement in recent

months (chart). The UK consumer is also seeing

deteriorating real incomes, which hit spending, and a

collapse to nearly zero in the most flattering version

of the savings rate (chart). We continue to view the

pace of spending from the UK consumer as wholly

unsustainable and consider a consumer-led

contraction in economic activity a when, not an if.

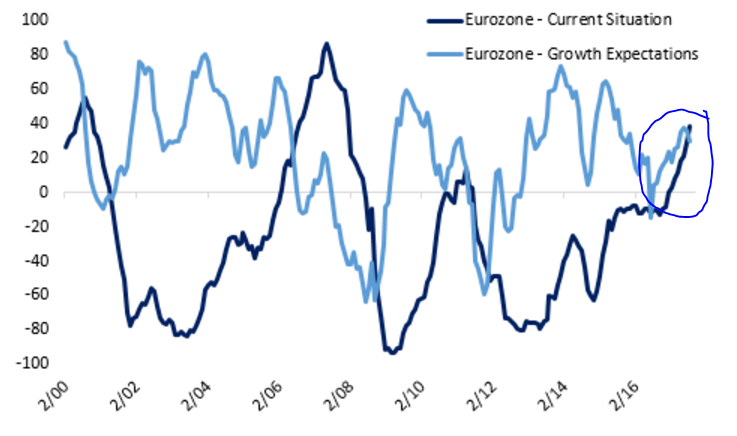

And here’s from this morning’s release of last month’s Zew Eurozone Sentiment Survey:

Clearly the UK isn’t sharing its to-be-ex-partners’ optimism!

Speaking of trade pacts, let’s hope our policymakers are very careful with their NAFTA “renegotiation”! Ironically, the industries the administration ostensibly aims to support stand to lose the most:

CEOs are also starting to mention Nafta on earnings calls. Profit estimates appear to reflect other factors, however, and may be the next shoe to drop. Machinery, autos, agriculture and energy appear to be the industries that face the greatest risk from Nafta renegotiations. They represent the U.S.’s largest two-way trade markets with Canada as well as Mexico.

Bloomberg Economics