Schwab’s Jeff Kleintop points out the extremely positive breadth (my highlight below) in global corporate earnings, which speaks to the general health of the global economy as well as the generally bullish equity setup (we’ve been illustrating herein) going forward:

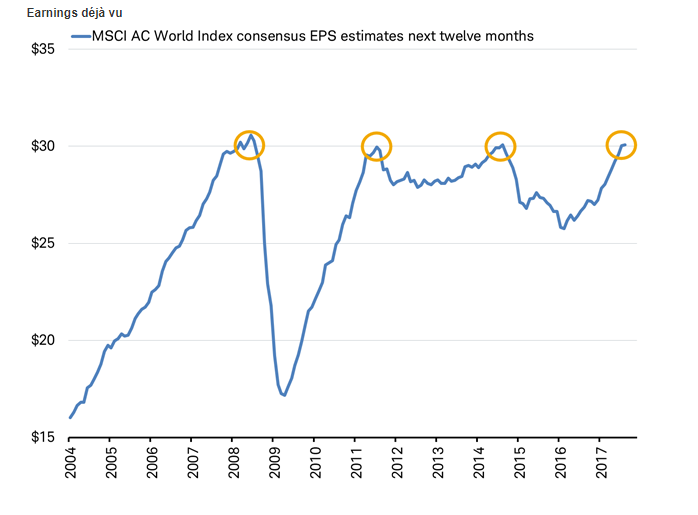

Ever get the feeling that we’ve been here before? For investors, the sense of déjà vu may be coming from corporate earnings. The analyst consensus estimate for earnings per share over the next twelve months for the world’s companies (measured by the MSCI All Country World Index) has risen back to $30 again for the fourth time in 10 years, as you can see in the chart below.

Since first reaching this level in 2008, earnings per share for the world’s companies has taken about three years to return to $30 after each decline. Despite the similar three year intervals, each decline in earnings was unique with differing depths and drivers.

- The drop after the 2008 peak, due to the global financial crisis, was deep and broad across regions and sectors.

- The drop after the 2011 peak was shallow and tied to the relatively mild recessions in Europe and Japan.

- The drop following the 2014 peak was greater than 10%, but almost entirely due to the impact of the crash in oil prices on the Energy sector.

Interestingly, the regions that lifted earnings to $30 have also been different each time, as you can see in the chart below (all regions’ earnings per share are indexed to 100 at the start of 2004 to make the comparisons easier).

- In 2008 it was Europe and the emerging markets that contributed the most to lifting global earnings to $30.

- In 2011, the full rebound in the United States and emerging markets were the drivers back to $30.

- In 2014, Japan’s rebound to its prior peak offset weakening emerging markets to reach $30 again.

- In 2017, the current rebound to $30 was supported by a rise in all regions.