We’ll make part 3 of this week’s look at the economy our weekly message as well. As you noticed in the previous two updates (here and here), U.S. consumer and business activity is not sending signals that we should be fretting the next great recession just yet.

As I’ve stated here before, there’s no better place to look for stress in the system than in the credit markets — so we’ll explore some key indicators to paint the present picture.

The following charts (click to enlarge) go back as far as the data allow. Note the trends leading into past recessions (red-shaded bars) and compare to the present. I highlight each title green, yellow or red to reflect my view of the prevailing trend.

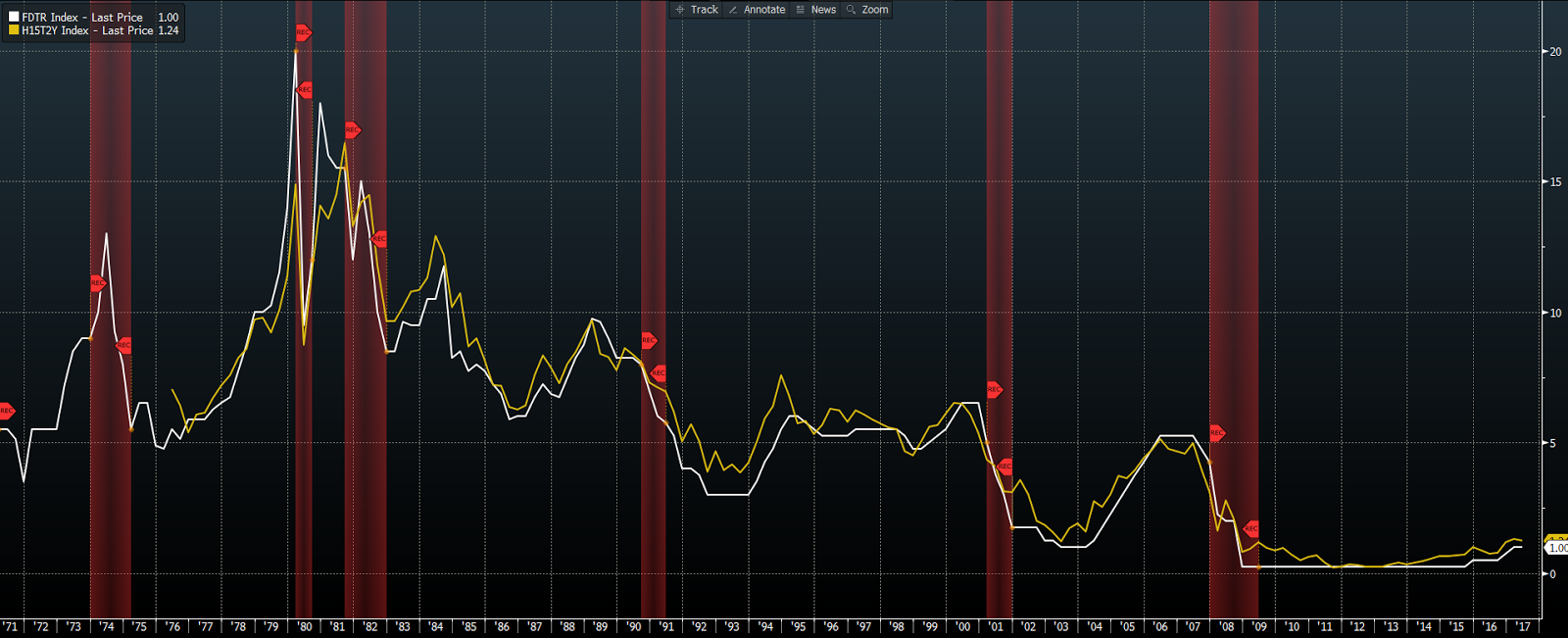

2-yr Treasury/Fed Funds Spread

The 2-year treasury note’s yield tends to trade at a slightly higher level than the target fed funds rate. When the 2-year yield deviates we pay attention: Moving below the fed funds target, for example, can be a sign of excessive pessimism in the economy and perhaps unrealistic hopes of a fed rate cut. If it moves unusually high relative to fed funds, it can be a sign of excessive optimism. The current .24% spread is, historically-speaking, a comfortable spread.

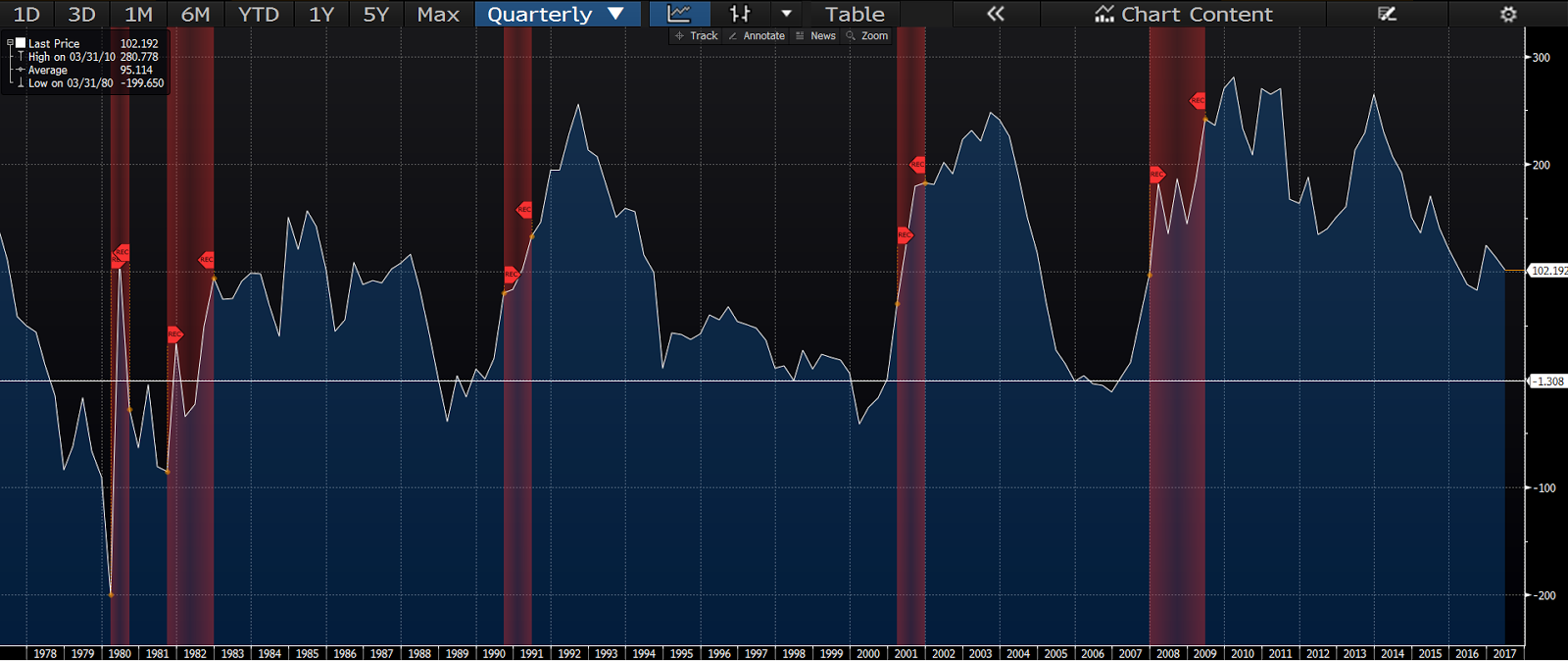

Yield Curve

Recessions seldom occur without the yield on the 10-year treasury bond first dipping below that of the 2-year note (an inverted yield curve). While the curve has dipped recently, we’re a long ways from inversion.

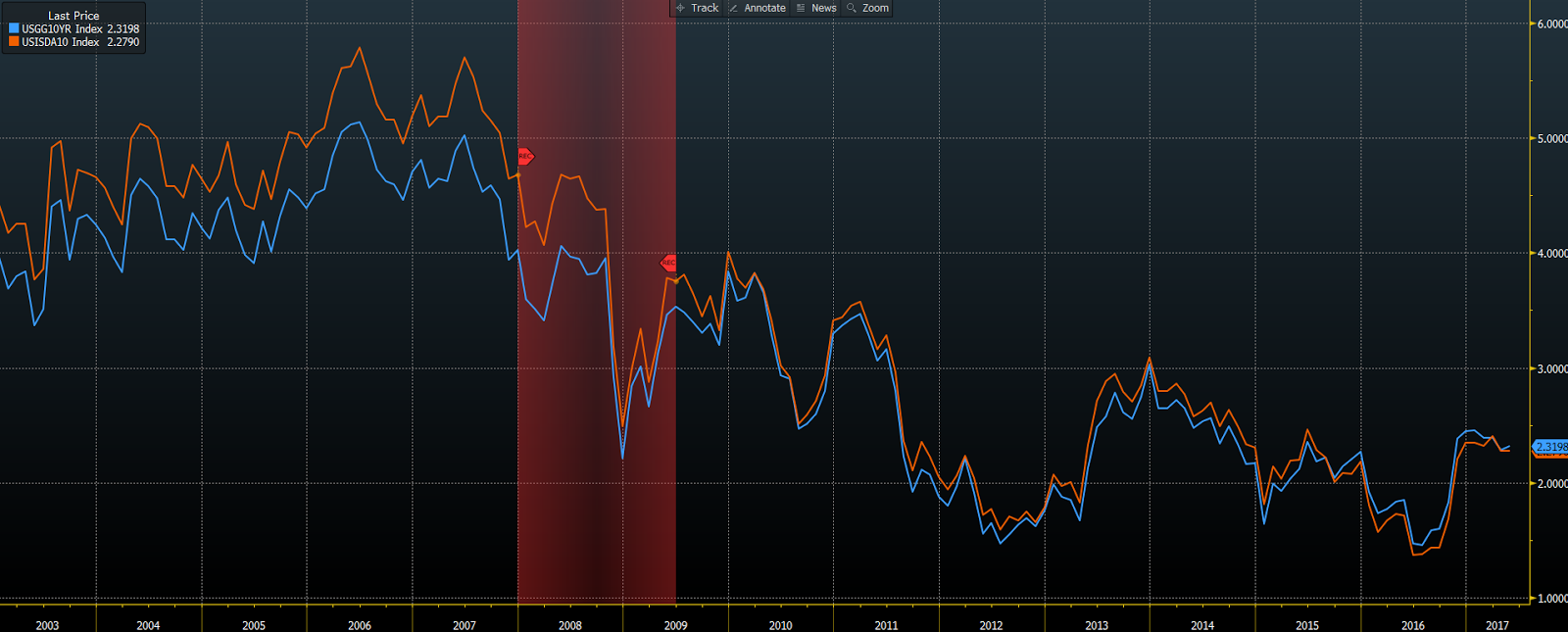

Swap Spread

When variable rate debt holders fear rates will rise they may look to the swaps market to trade (swap) their variable rate for a fixed rate. The higher demand will push swap rates higher. The swap rate thus becomes a gauge of interest rate expectations and overall credit conditions. The 10-year swap to 10-yr treasury spread gives a good look at forward expectations; it remains nonthreatening relative past trouble spots.

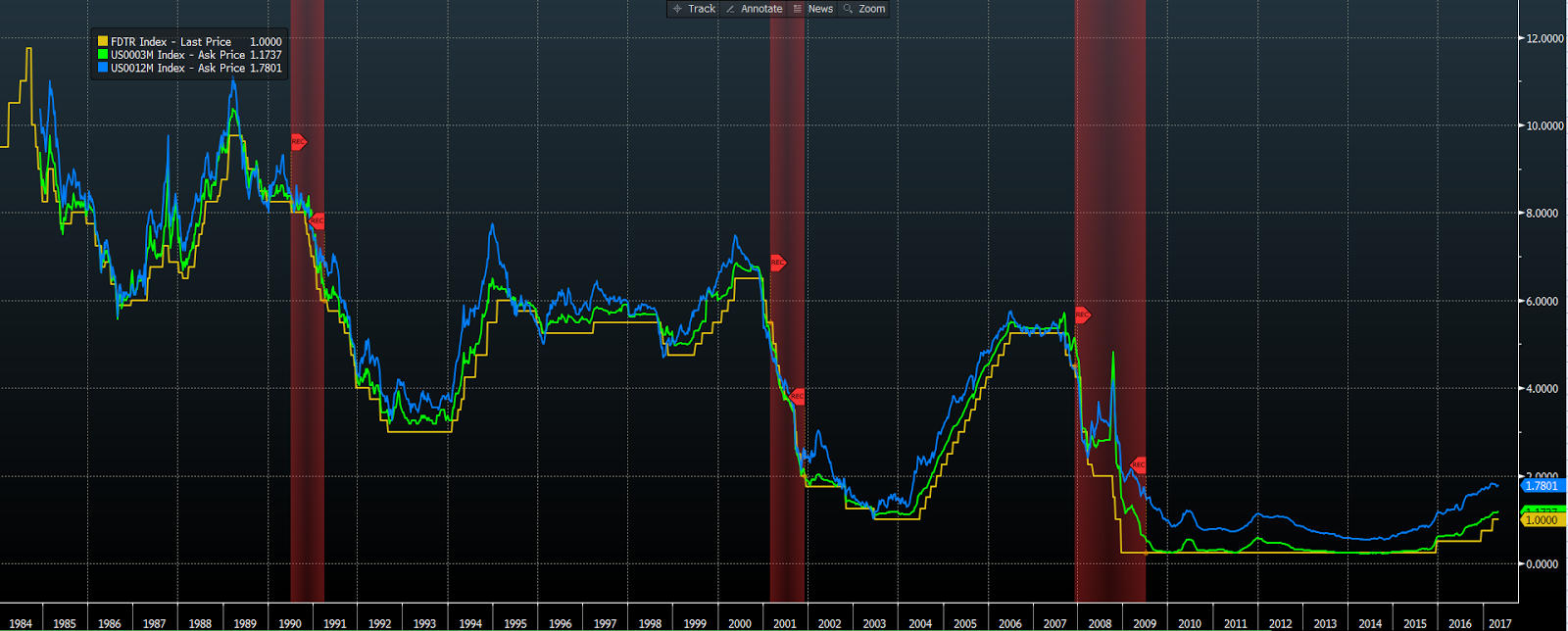

LIBOR/Fed Funds Spread

The cost of vast amounts of debt globally is tied to the LIBOR rate. The 3-month (green line) is tightly correlated to the fed funds rate. During periods of economic stress the spread widens as LIBOR rises in response to concerns regarding borrows’ credit worthiness. While the spread widened a bit throughout 2016, it has narrowed since and presently denotes little if any global credit concerns.

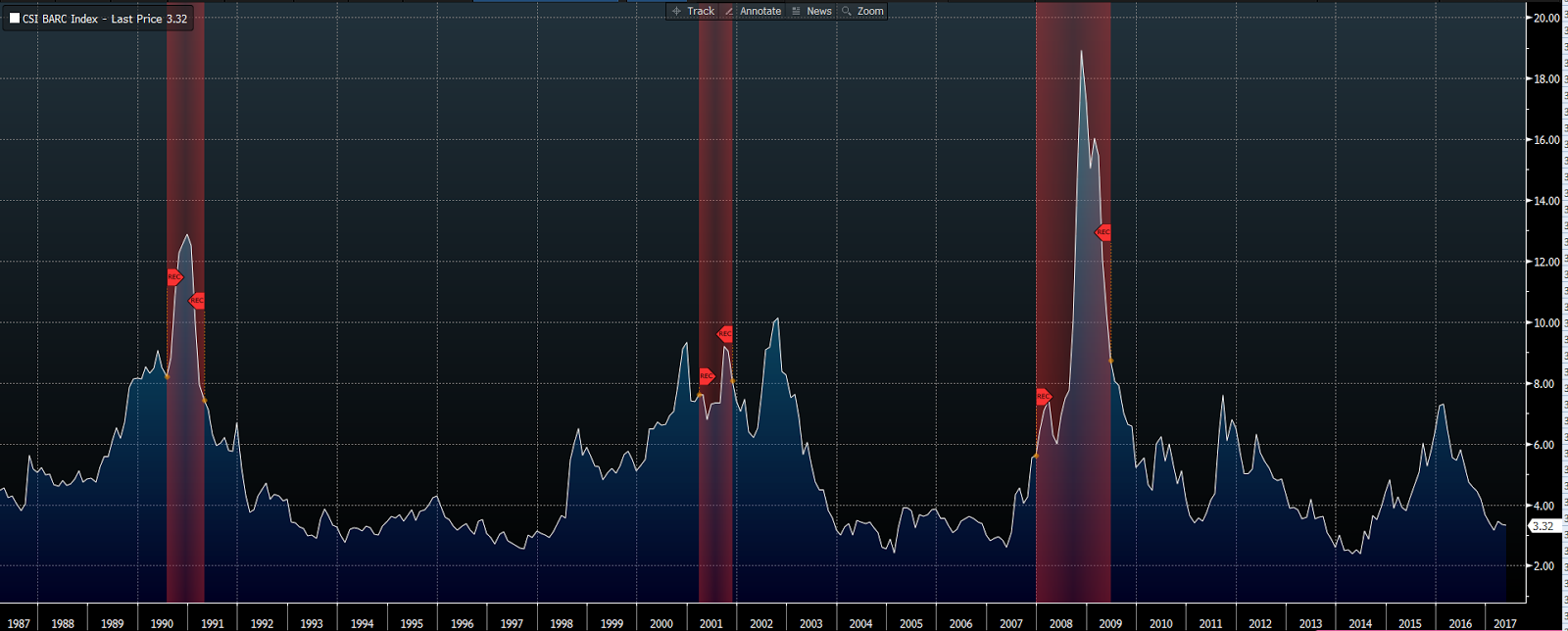

High Yield Credit Spread

The difference between the yield on high-yield (junk) bonds and treasury bonds is one of the best indicators of credit market conditions, as well as the overall state of the economy. When the economy is suspect, investors require higher returns from low-quality issuers of debt. They also buy treasuries under such circumstances, pushing treasury prices up and yields lower. The opposite occurs during good economic times: Investors are comfortable with the credit worthiness of lower-quality borrowers and thus bid their bond prices up and yields lower. They’re also less apt to invest in treasuries, forcing their prices down and yields higher. This indicator had a very concerning look from mid-2014 into early-2016: As we addressed here on the blog, it appeared at the time to be virtually all about the energy industry (the largest issuer of junk debt over the past few years). As oil prices collapsed, so did the marginal producers who had heavily tapped the high yield debt market. The present trend speaks very well of the economy and of current credit conditions!

Chicago Fed Financial Conditions Index

The NFCI tracks liquidity and leverage in debt and equity markets, as well as money markets and shadow banking systems to determine whether present financial conditions are tight(ening) or loose(ning). Positive values denote tight(ening) conditions. The present level is nearly as good as it gets.

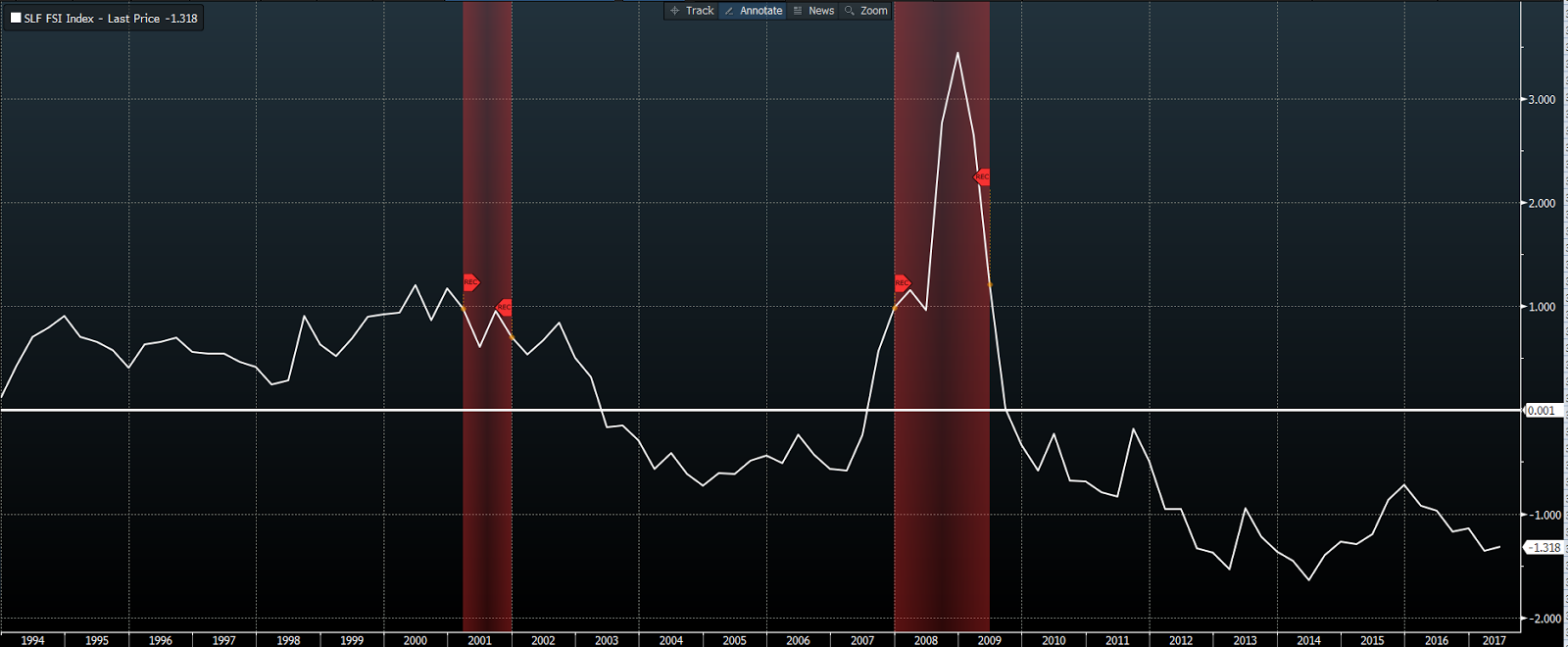

St. Louis Fed Financial Stress Index

The STLFSI tracks financial stress in the markets by assessing 18 weekly data series: 7 interest rate series, 6 yield spreads and five other series. Above zero denotes high stress in the system. Today’s level speaks very positively about present credit conditions.

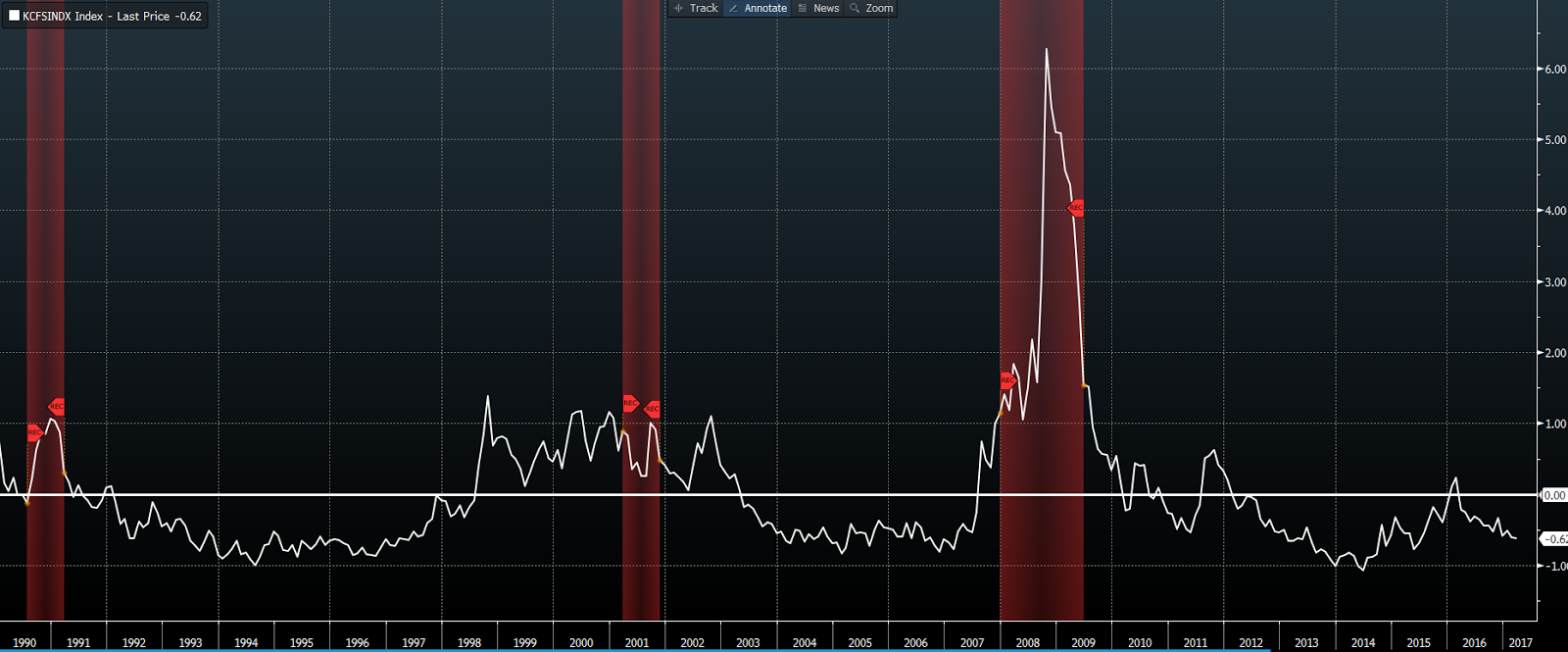

Kansas City Fed Financial Stress Index

![]()

The KCFSI measures stress in the U.S. financial system by tracking 11 financial market variables on a monthly basis. Values above zero denote above average stress in the system. Ditto the Chicago and St. Louis Fed indicators.

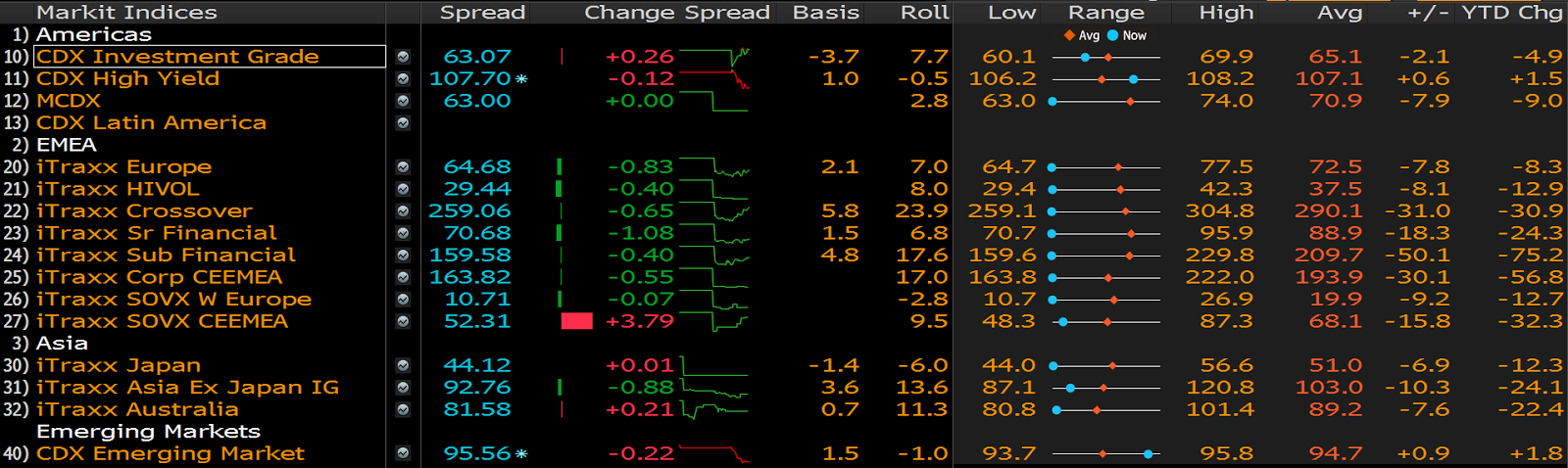

In my effort to present something that I can highlight in a color other than green, I thought I’d include a year-to-date look at global Credit Default Swap (CDS) spreads. Here’s how I described them in a recent blog post:

There’s a thing called a Credit Default Swap (CDS); it’s in essence a guarantee of someone else’s, or an entity’s, debt. For example, if I buy a French government bond and want to protect myself, I pay a guarantor a slice of the interest to protect my investment, should I be stiffed by the French. The contract we enter into is the CDS. Of course the riskier the borrower the more the interest the guarantor will require of me to protect myself. Make no mistake, the issuers of CDS, and those who trade those certificates in the market, are intently interested in the health of the global economy. That — as opposed to book sales — is where their livelihoods lie.

Problem is, I had to go green here as well. I initially thought I’d at least be able to add a little yellow or red due to worries in Europe. However, since for the moment it looks like Macron has the French election in the bag, and the Euro Zone economy is picking up markedly, Europe’s CDS spreads have plummeted.

Global CDS Spreads

The far right column shows the year-to-date change in spread. With the exceptions of U.S. High Yield and Emerging Market debt, the cost of protection has decreased notably so far this year.

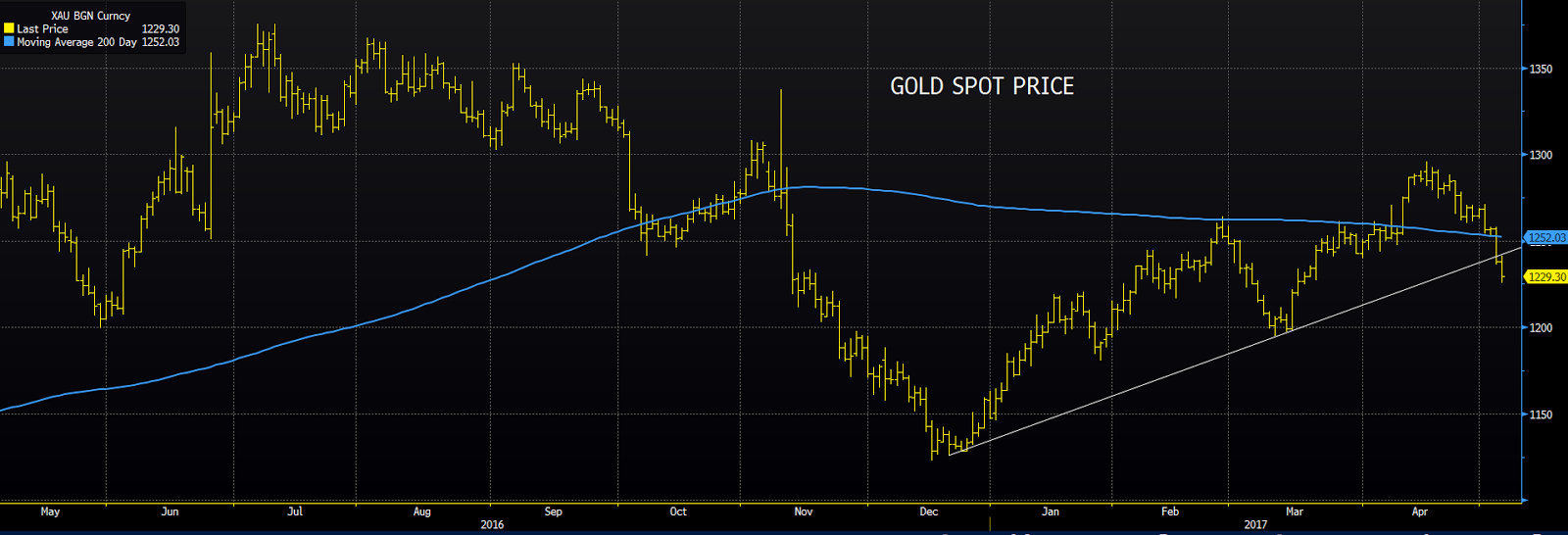

So, in a last ditch effort to mix up the colors, we’ll leave the credit markets and consider gold. Now here’s something that’s been flashing red (rising trend) since the end of last year (folks buy gold when they fear the end of the world beckons). However, as I‘ve addressed here on the blog, I haven’t been a believer. And, lo and behold, the yellow metal appears to be breaking down of late, meaning the global system may not be on the verge of breaking down after all. We’ll still highlight it yellow for now, I mean we gotta worry about something!

Gold Spot Price

Have a nice weekend!

Marty