Maybe a dozen times a year a client will tell me about a book he/she read, or send me a link to an article or a YouTube presentation where some really smart individual who once uncannily predicted some cataclysm (or so somebody claims [typically the soothsayer him/herself]) offers up yet another gloomy prediction. In perhaps less dire fashion, the financial networks forever parade those stock picking celebs who, with great condescension, pick apart the case that stocks — as a group — can move much, if at all, above present levels.

There’s definitely something cool about being the contrarian; particularly when the unwitting consensus is optimistic. Predictions of economic pain somehow seem deeper, more thoughtful, more intellectual than the bleary-eyed belief that, despite global political power struggles that inspire all manner of threat, everything’s a-okay.

Even Warren Buffett, the great believer in America, the forever long-term optimist, relishes playing the contrarian. Although, he kinda does it in reverse to the norm, i.e., in less cool fashion — he plays the optimist when the crowd’s pessimistic. His most quoted quotes would be: “I buy when there’s blood in the streets” and “I get greedy when everyone else is fearful”. Well, come to think of it, I guess he does at times play the “cool” contrarian; the latter quote has a second part: “and fearful when everyone else is greedy”.

Regular readers might think me the contrarian as well. I’ve made it my practice over the years to point out how the crowd generally congregates on the wrong side of the proverbial boat. I’d like to think, however, that when I am the contrarian, that I am so not for contrarian’s sake; I’d like to think that my views are supported by the data, by history, by the setup, if you will, as opposed to by a desire to impress.

But maybe it’s okay, or more than okay, to be contrarian for contrarian’s sake. I mean, if bucking the trend works for Buffett, and if other really smart people suggest we’re better off doing so, why don’t we just always buck the trend? That’s pretty much what Harvard economist Terry Burnham, in his interesting book Mean Markets and Lizard Brains, says we should do:

To do well, an investor has to purchase exactly that which is unloved. This requires an ability to take the emotional pain of being different.

One of the core truths about investing is that the consensus is comfortable, but unprofitable.

Yeah, I get that; like I said, I’ve preached it myself. But, you know, it’s not all that simple. My, how I wish it were! My job would be a piece of cake if all it takes to do well is to buy “that which is unloved”, or to counter the consensus. Yet my experience over the past 32 years — as you’re about to see — says otherwise.

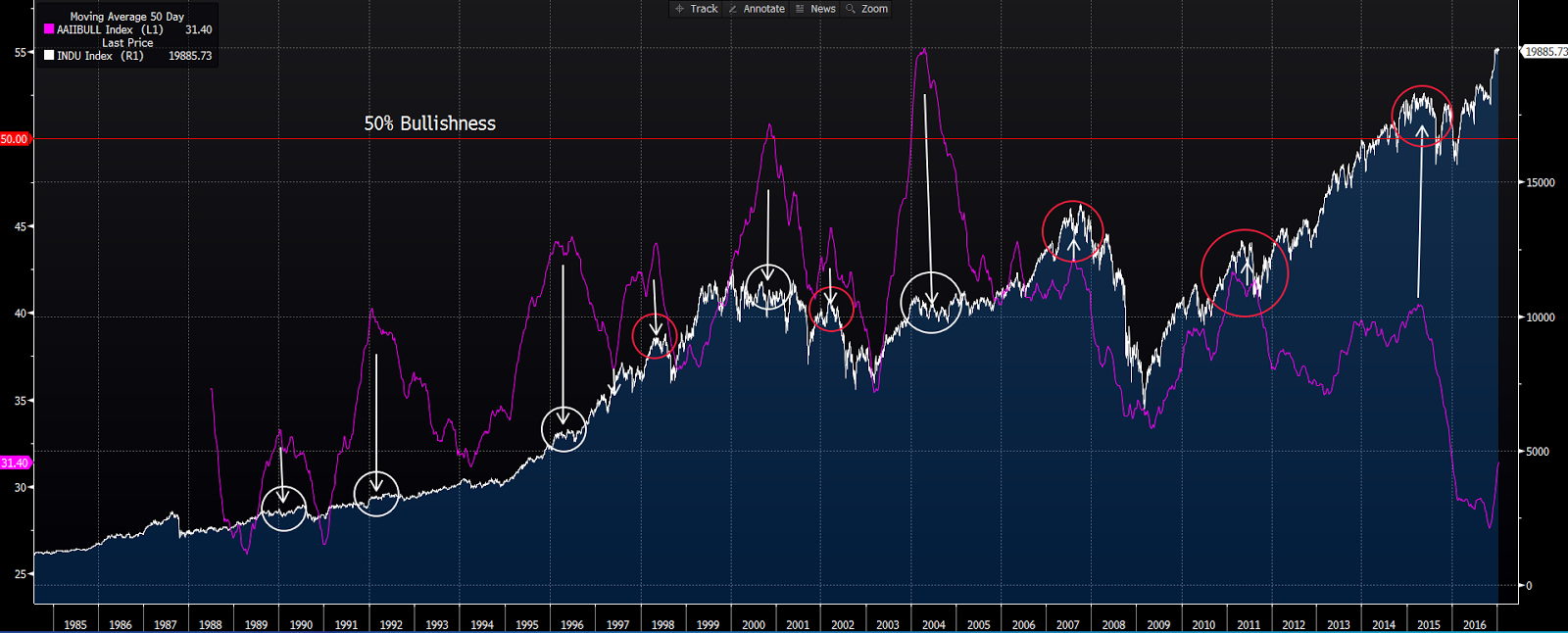

Here’s the Dow, along with the 50-day moving average of the bullish readings of the weekly AAII Sentiment Survey (purple), from the day I started my career: click to enlarge…

Note the arrows pointing to the Dow right at each peak in bullish sentiment. Clearly, for the long-term investor, playing the contrarian doesn’t always pay — the market turned down shortly after a bullish peak in just 5 of the 10 instances featured. In fact, I can argue that there were just two instances where the reading peaked at a level that would truly be considered highly bullish (above 50%). In the first the market meandered, dipped, then rallied before giving way to the bursting of the tech bubble. The second, the highest, occurred one year into what turned out to be a 4-year bull market. So we’ll say, charitably, that the contrarian was right half the time.

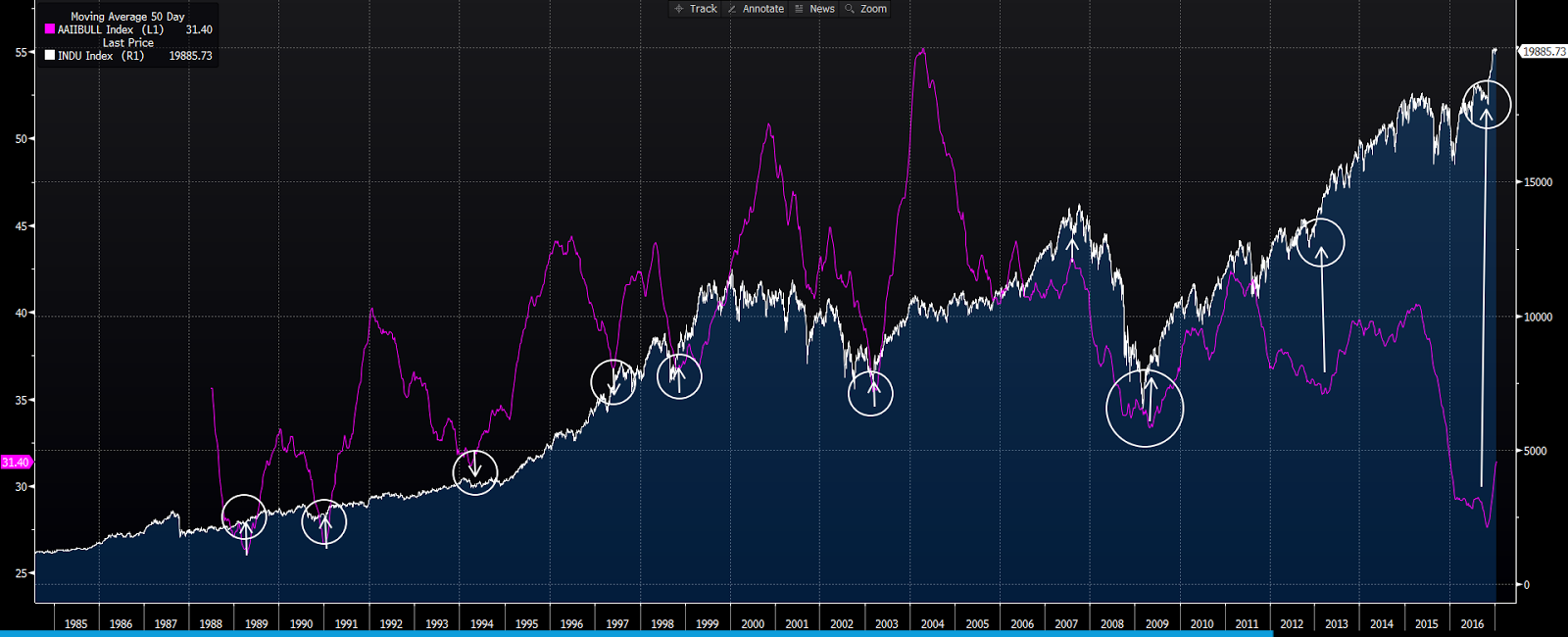

Now wait a second! Take another look at that chart. Look at what the market was doing when the crowd was the least optimistic. Here, I’ll circle the spots on the Dow where average bullishness was hitting its nadirs:

Fascinating! In all nine instances when bullishness was reaching its lows — and yes it was indeed low in those instances (under 40%) — the market was either beginning. or in the midst of, an impressive upward run. So, apparently it does indeed pay to be the contrarian — just more so when the crowd’s the most gloomy. The bummer is, like I said above, it’s not nearly as cool being the contrarian when it means being bullish.

In truth — when you get right down to it — many of the so-called contrarians running around out there aren’t contrarian at all, not even close. I mean, they may be cool (always being bearish) but they’re definitely not being contrarian — they just appear to be, since bull markets tend to last much longer than do bear markets.

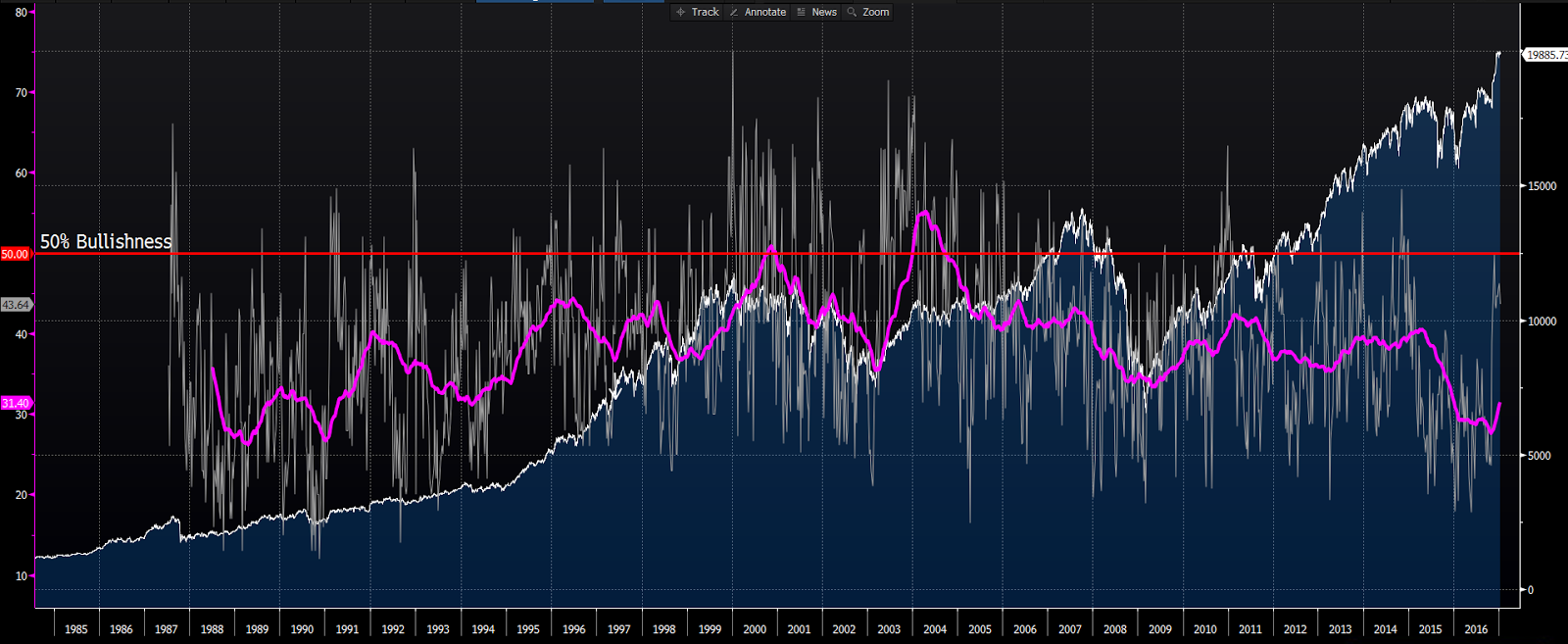

Note: In smoothing the sentiment indicator (by using its 50-day moving average) I run the risk of giving you the idea that a bullish reading above 50% is a rarity. Fact is, it’s not. The chart below includes the actual weekly readings. You can see why I needed to smooth the number, and you can see that high bullishness among individual investors is historically not at all uncommon. And, again, you can see that — for the long-term investor — it’s not always the best contrarian indicator.

Back to the dozen or so times a year when I’m forced to respond to the prognostications of some cooler-than-me doomsayer. The fact that it gets brought up suggests that the book, article or video indeed provoked concern among my client. And, alas, that (the willingness to be provoked) is — I assure you — far more dangerous to the financial health of the investor than is the prophesy itself.

While we can debate the efficacy of the above quotes from Burnham’s book, the following (from the same book) speaks to the dangers of allowing the news, or some prediction, to move us emotionally. This, in my view, is spot on:

A recent study documented the physiological reaction that people have to market information. Professor Andrew Lo and Dmitry Repin wired up a group of professional traders. With a setup not too different from a heart stress test, these MIT researchers were able to measure minute changes in body temperature, skin conductance, and a host of other variables. The traders they wired were trading real money for an investment firm.

What happened to our wired traders when news broke? Lo and Repin report two interesting findings. First, all the traders—even the most experienced—had measurable emotional responses to news. Second, the more experienced traders had weaker emotional responses than their less-experienced colleagues.

These physiological responses may help us understand mean markets. When people see stock price changes or read about world events, we have physiological responses. If we act on those emotions, we tend to make precisely the wrong moves. In other words, we need to shackle the lizard brain in order to make money.

To be successful we have to damp down our emotional response (toward the lower response of the experienced professional traders in the MIT study) or we need to prevent our emotional reactions from impoverishing us.

Have a nice weekend!

Marty