Thursday morning we added two charts (U.S. and Australian trade data) to our current trends file. Both speak positively about the current state of the global economy.

While we believe the U.S. trade deficit receives far too much, and ill-conceived, attention, we do look into the data to help gauge our view of the global economy. We agree with Bloomberg’s note below that American export growth speaks positively: click charts to enlarge…

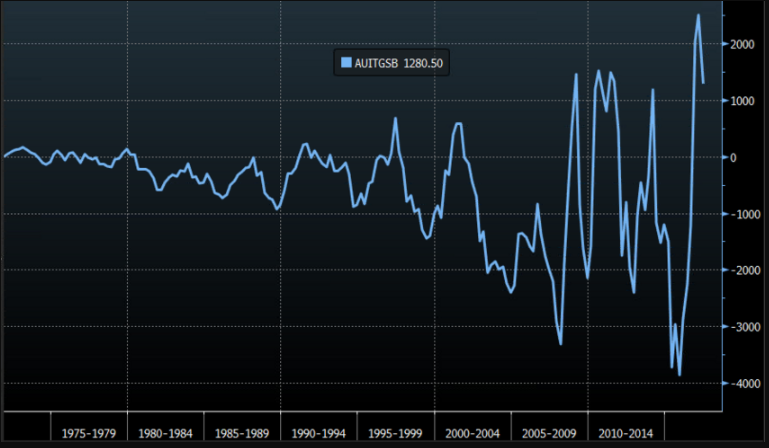

Australia’s trade data was released Wednesday evening. A huge commodity supplier to the world (particularly China), Australia’s recent export surge supports the global growth narrative:

Although Australia’s numbers are owed to rising commodities prices as well:

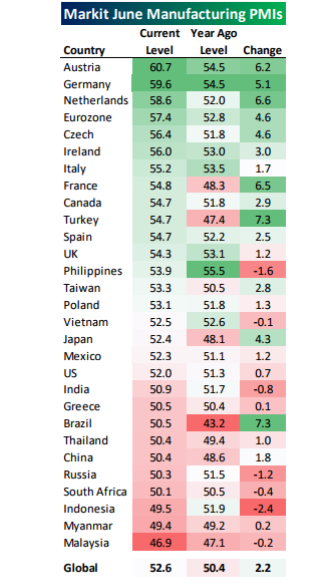

Manufacturing Purchasing Managers Surveys across the globe also — on balance — argue on behalf of global growth (above 50 denotes expansion):

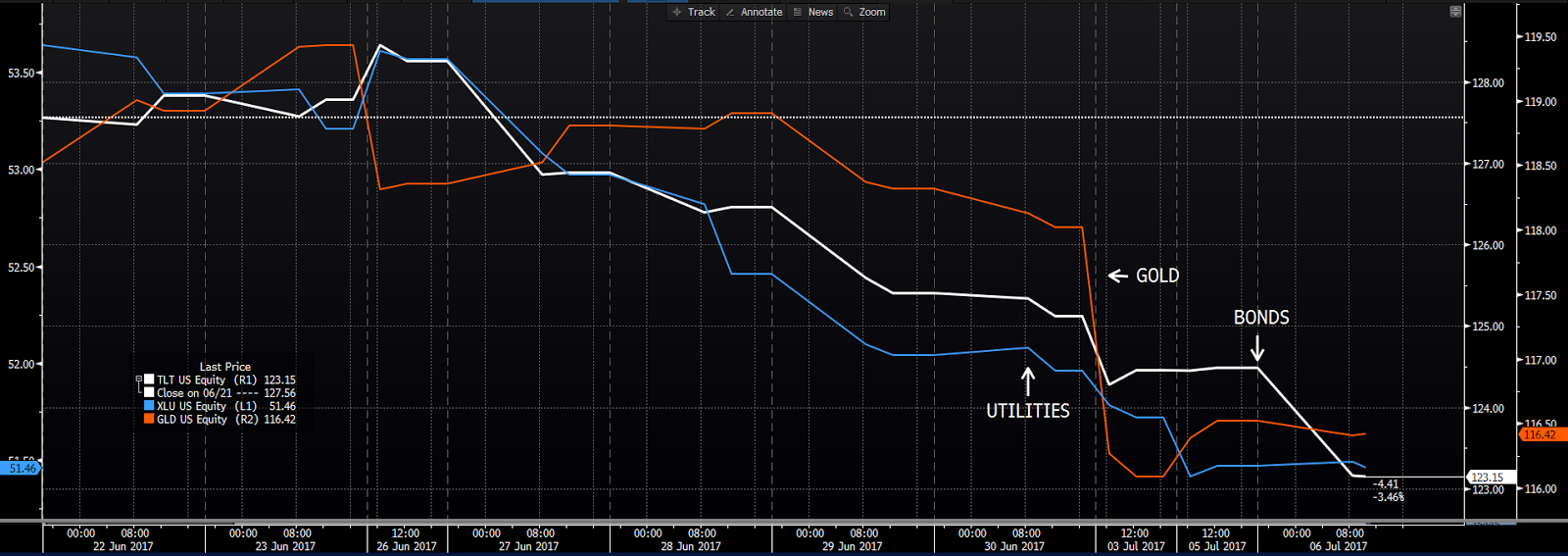

While that’s all fine and good, if you tend to worry about the potential negative effects of higher interest rates on asset prices, the above should trouble you. For a feel of the heightened sensitivity, here’s a 2-week look at bonds, gold and utility stocks (3 classes we view as presently (highly) exposed to interest rate risk):

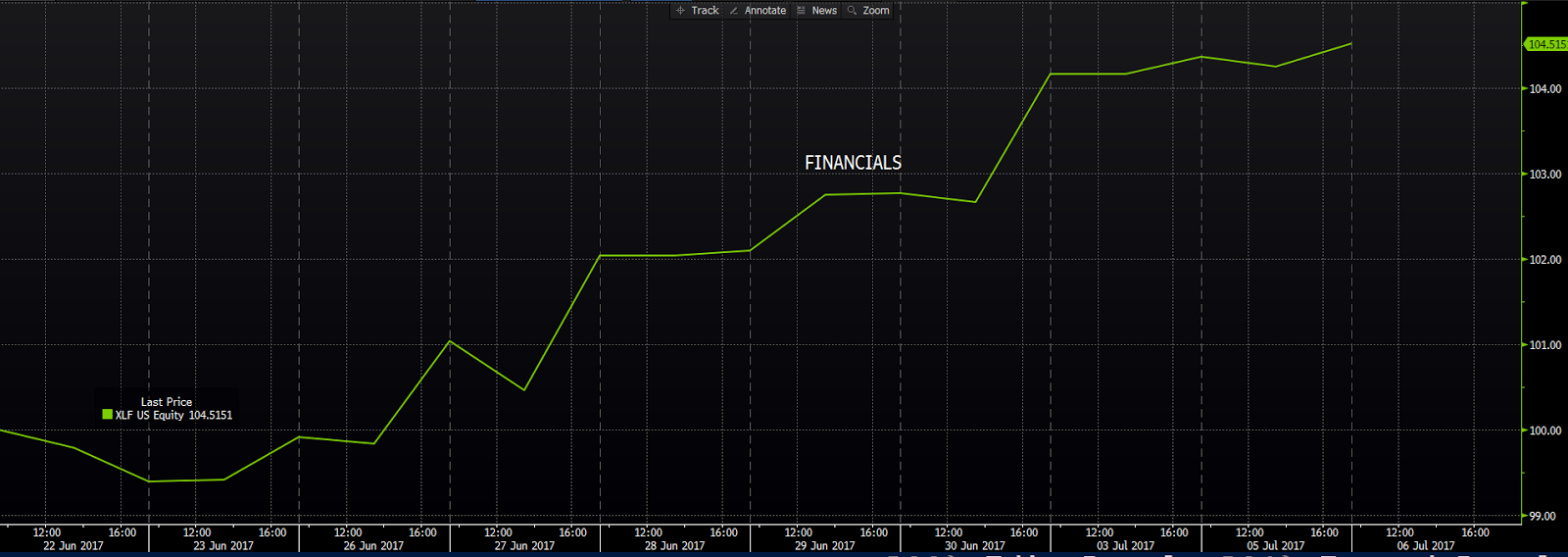

Ah, but if, like us, you’re bullish on financials, you’re feeling pretty good about higher rates amid an improving global economic backdrop. Here’s a 2-week look at our core financials ETF:

Two things to note in closing: One, 2-week charts are never the makings of long-term investment theses, and, two, after a phenomenal stretch of extremely low rates, we virtually have to expect higher — across the board — volatility, as global asset markets recalibrate to a higher interest rate environment (assuming that’s what shakes out over the coming months). As implied by this 2-week look at the S&P 500 Volatility Index (VIX):

Have a great weekend!

Marty