Our May 11th blog post was well received (we assume so because of its unusually high number of clicks). That essay came to mind this evening as I pondered what I’d offer up for this week’s message. We subtitled it “Why Didn’t Brexit, or Trump’s Victory, Derail the Market?”.

Barring a missile landing on dry ground in a country other than its launcher’s (although the Jesse Livermore quote below challenges the notion that even such things will ultimately derail a market when it’s in a bullish mood), the market setup underlying recent volatility begs a weekly message featuring essentially the same theme. Therefore, we’ve copied and pasted it below, while replacing each chart with today’s. Just picture the words “North Korea” slipped in wherever you see Brexit and Trump.

Yes, this is indeed premature, but it explains why, at this juncture, we see present volatility as volatility to ignore. Of course, with financial markets, all possibilities (regardless of setups) are forever on the table.

—————————————————————————————–

May 11, 2017 (Charts as of August 10, 2017)

The great conundrums of the past year have been Brexit and Trump. Pundits, en masse, had global markets tanking should either, let alone both, succeed. Well, as you know, both succeeded and, go figure, a number of the world’s equity markets marched to all time highs in the aftermaths.

So, is it that Brexit and the President’s proposals/policies/positions are — contrary to early “expert” opinion — inherently good for markets? Or is it something else altogether?

What if the same events had occurred in the fall of 2007? At a time, we know in retrospect, when certain, and serious, stresses were boiling beneath the market’s surface. Would either event have delayed, mitigated or even eliminated the great 2008 recession/bear market? Or would they have exacerbated it? Well, how could anything have exacerbated what became the worst recession since the Great Depression?!?

While you and I may or may not agree as to the market-friendliness, or lack thereof, of either event, I bet we would agree — in that neither could’ve averted the 2008 economic collapse (right?) — that had either or both occurred back then, say, just before recession onset, it, or they, would’ve been dubbed the spark(s) that lit the forest fire.

We humans have a desperate need to make excuses for the world’s goings on, or, more kindly, we need to understand them. The thing about markets, alas, is that the moving parts are literally uncountable. Thus, we simply can’t know for certain what causes this or that to occur.

With that being said — surrendering to yours and my humanness — allow me to offer an excuse (albeit a broad, encompassing, yet a nonspecific and safe to present excuse) for our last recession. I’ll borrow the balloon analogy John Owen Weatherall featured in his fascinating book The Physics of Wall Street:

Imagine inflating a balloon. You start with a limp piece of rubber. In this uninflated state, the balloon is stretchy and very difficult to tear. You could poke it and prod it any way you like, even with a very sharp knife, and unless you stretch the balloon out first, the knife is unlikely to puncture it. A pin would do no damage at all. Now begin to blow air into it. After a few puffs, the balloon starts to expand. The pressure from the air inside is pushing the walls of the balloon out, just enough to give the surface a roughly spherical shape. The material still has considerable give. Depending on how much air has been pumped in, a very sharp knife might now slice the rubber, but the balloon certainly won’t pop, even if you manage to puncture it. A puncture would allow the air inside to leak, but it wouldn’t be very dramatic.

As you blow more air into the balloon, however, it becomes increasingly sensitive to outside effects. A fully inflated balloon is liable to pop from the slightest brush with a tree branch or a bit of concrete—a tap from a pin is certain to make it explode. Indeed, if you keep blowing air into a balloon, you can make it burst by touching it with your fingertips, or by simply blowing in another mouthful of air. Once the balloon is primed, it doesn’t take much to produce a very dramatic effect: the balloon shreds into tiny pieces faster than the speed of sound. What makes a balloon pop? In some sense, it’s an external cause: a tree branch or a pin, or perhaps the pressure from your fingers as you hold it. But these very same influences, under most circumstances, have little or no effect on the balloon. The balloon needs to be inflated, or even overinflated, for the external cause to take hold. Moreover, the particular external cause doesn’t much matter—it’s far more important that the balloon be highly inflated when it is pricked. In fact, the external cause of a popped balloon isn’t what makes the balloon pop at all. It’s the internal instability in the balloon’s state that makes it susceptible to an explosive pop. (emphasis mine)

Those last three sentences should’ve sparked in you a huge “Aha!”.

History’s great trader Jesse Livermore said it perfectly:

Not even a world war can keep the stock market from being a bull market when conditions are bullish, or a bear market when conditions are bearish. And all a man needs to know to make money is to appraise conditions.

Yes, it’s that simple folks, moving into 2008, conditions were bearish and stress in the economy (read bubble) was inflating mightily. The questions of course for the moment would be, are we presently experiencing bearish or bullish conditions? And, are we in a period of highly inflated economic stress — or are we at this point not nearly rubbing against a financial balloon ready to burst?

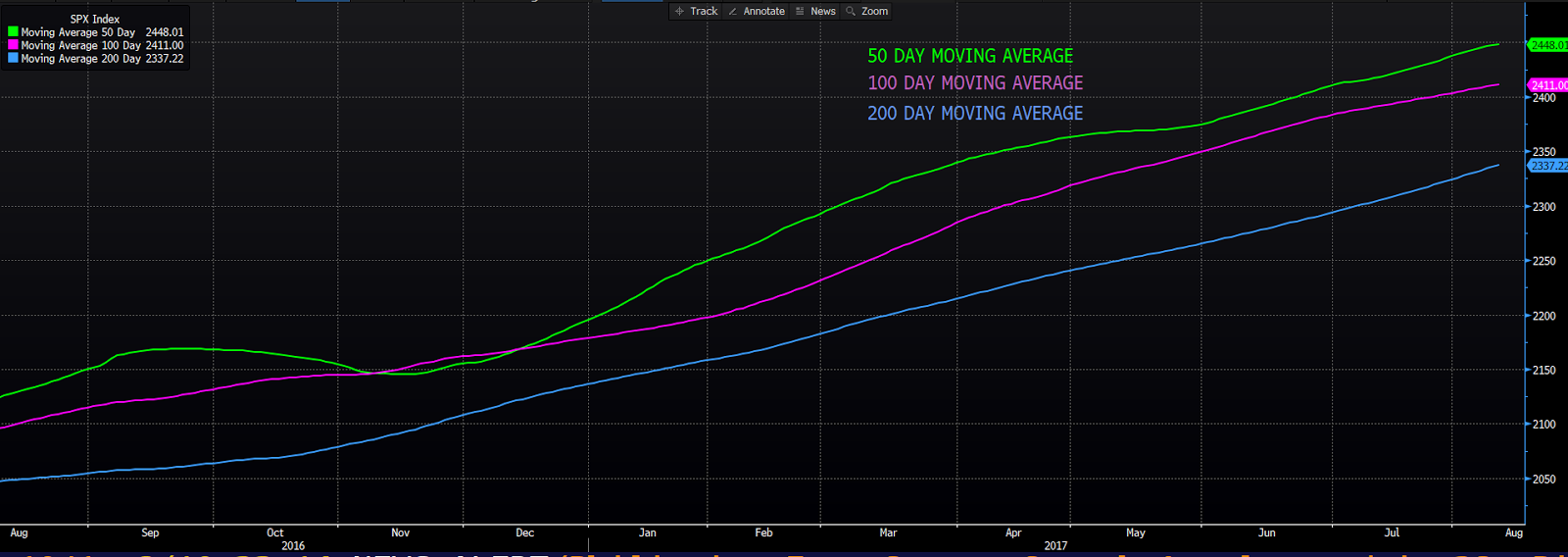

In terms of the market, all I can offer you is the underlying setup (market conditions) at this very moment. Take a look:

click any chart (each updated to 8/10/17) to enlarge…

That, with the S&P 500’s faster (shorter-term) moving averages on top, is the definition of a bullish condition.

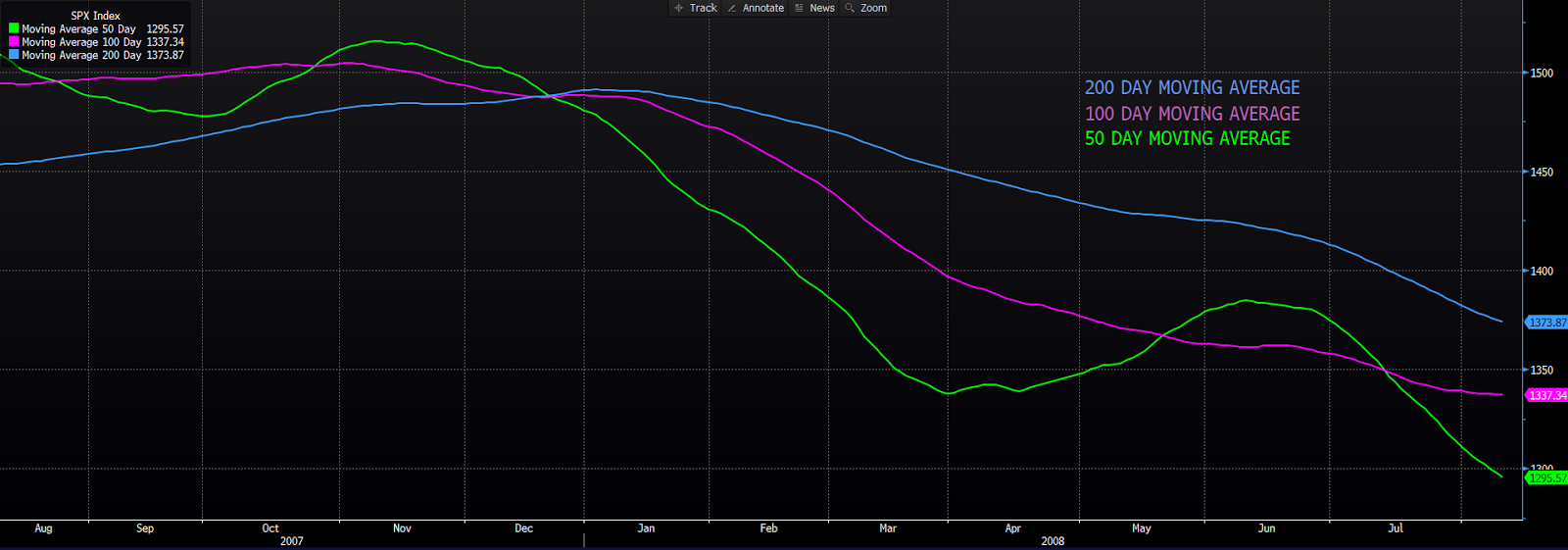

Here’s a look at the one-year chart leading up to this day in 2008:

That, with the faster moving averages on the bottom, would be your bearish condition.

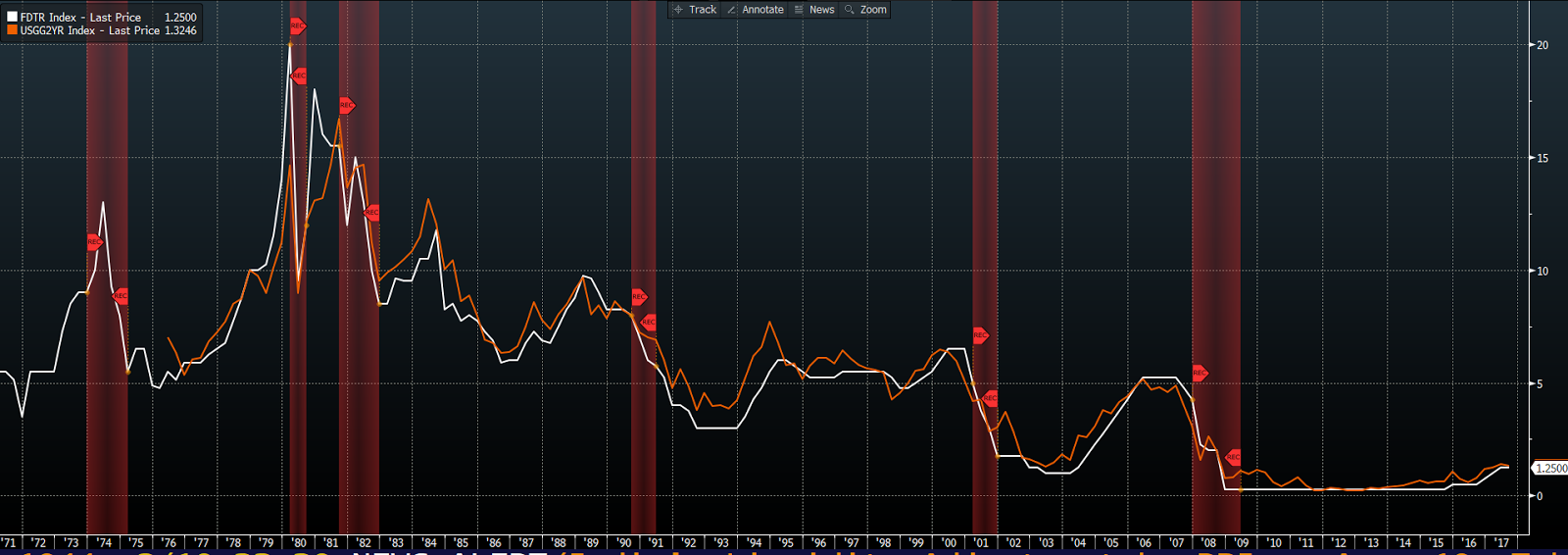

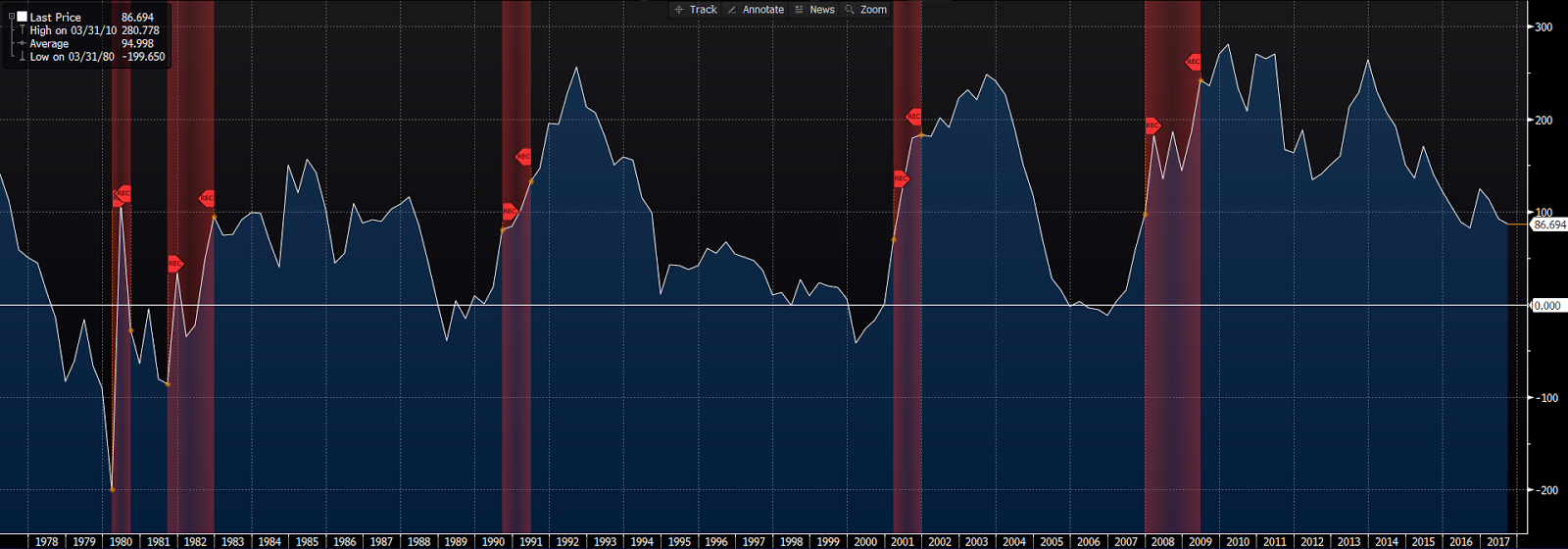

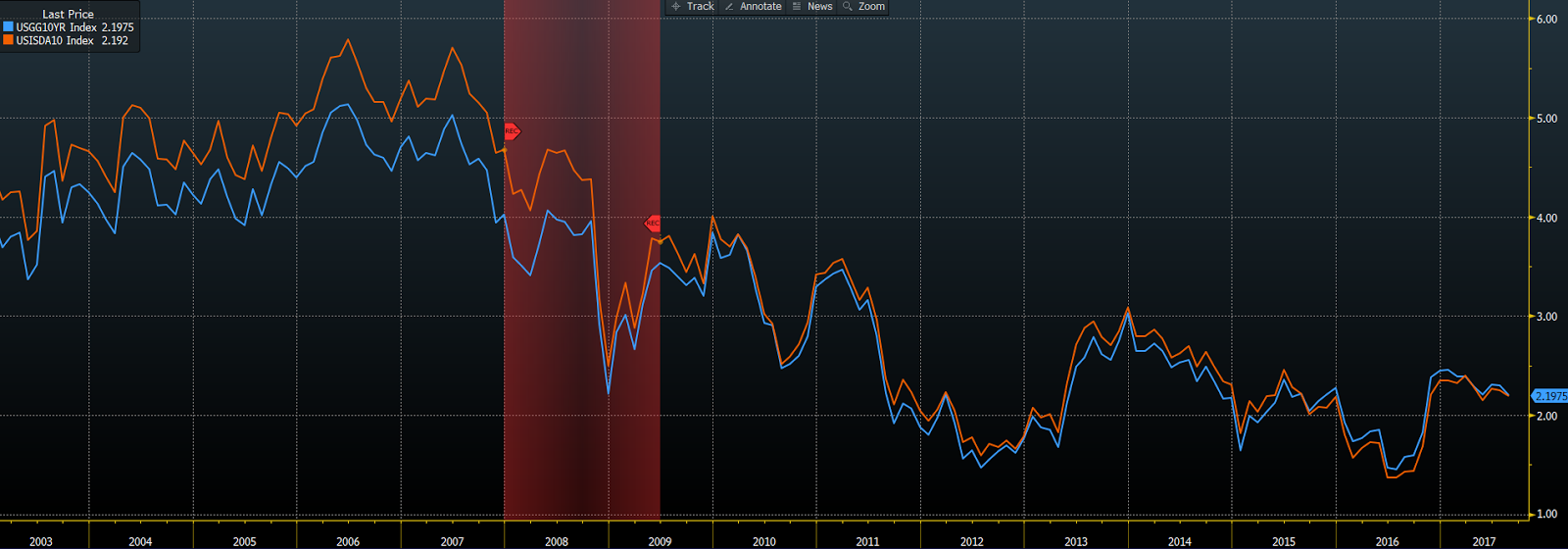

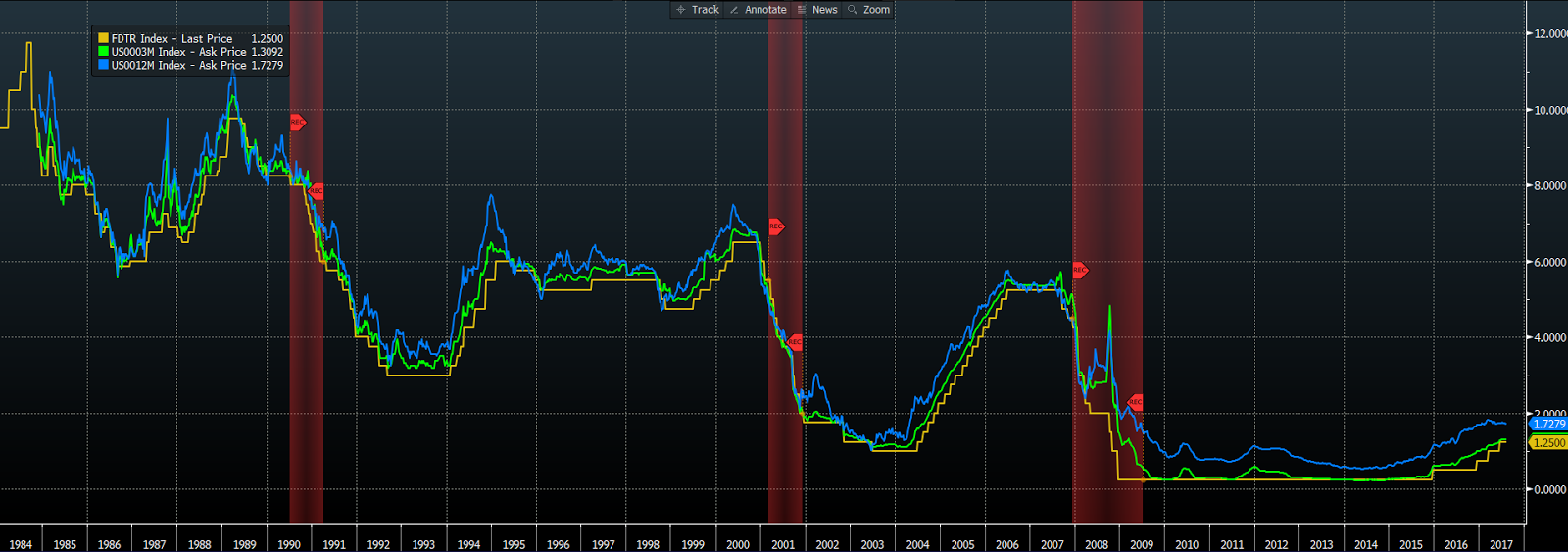

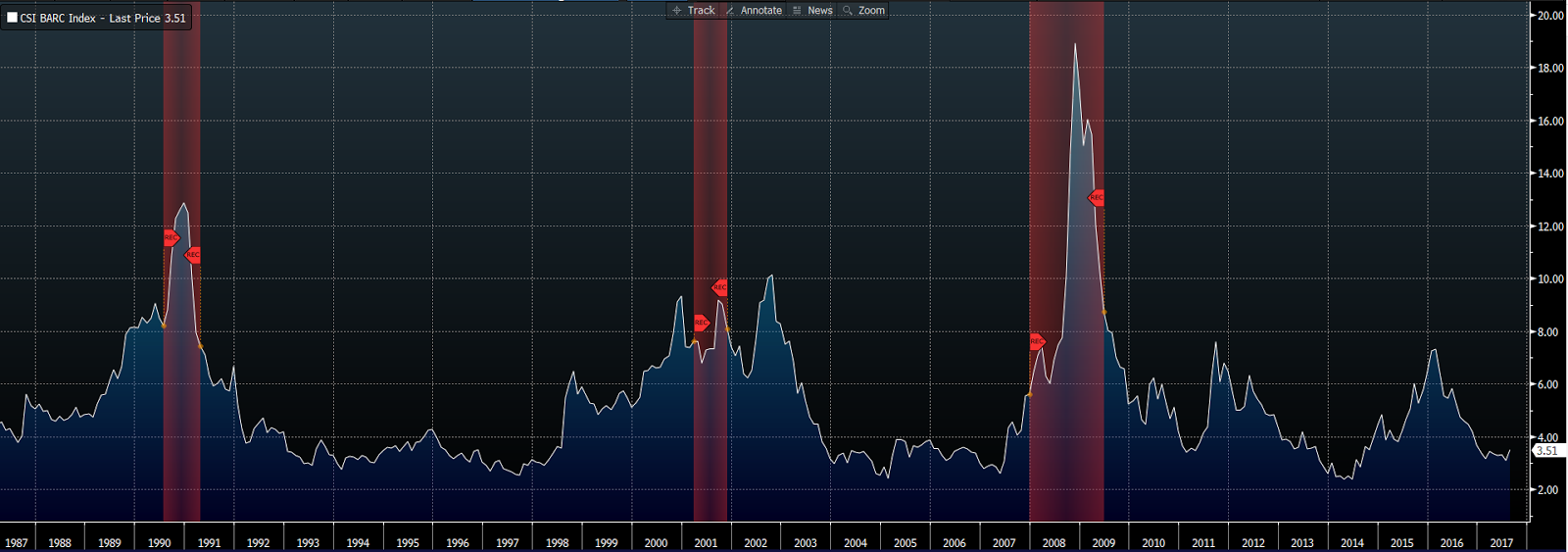

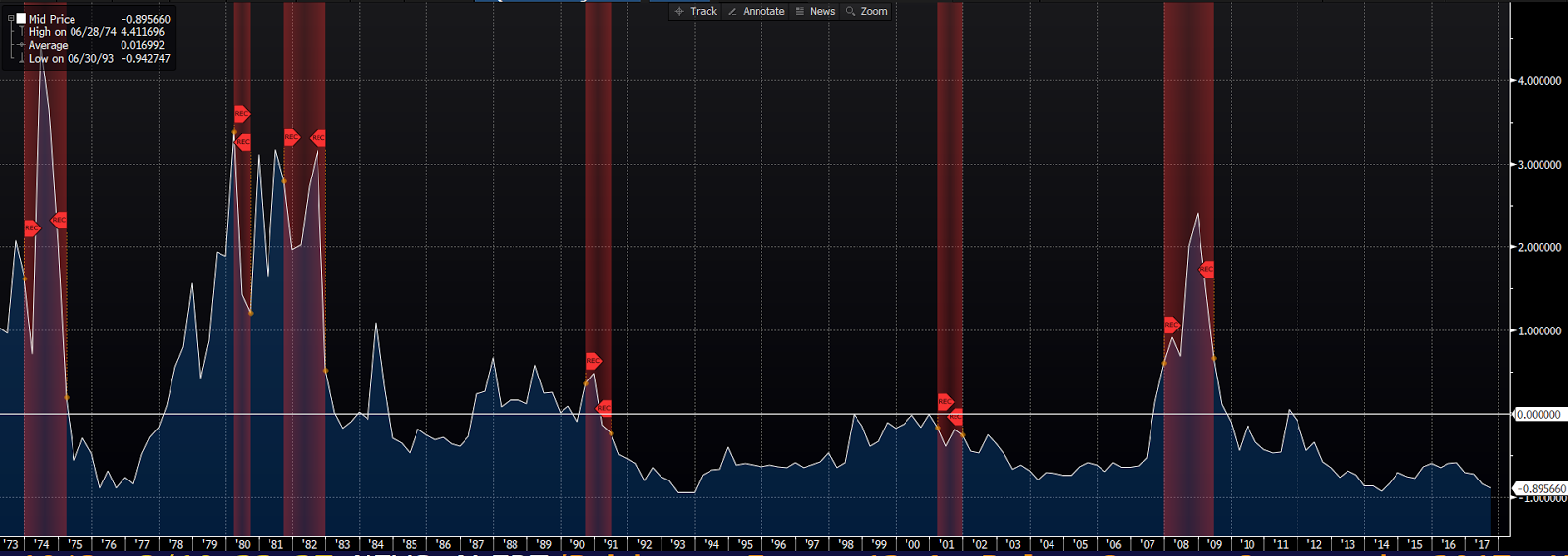

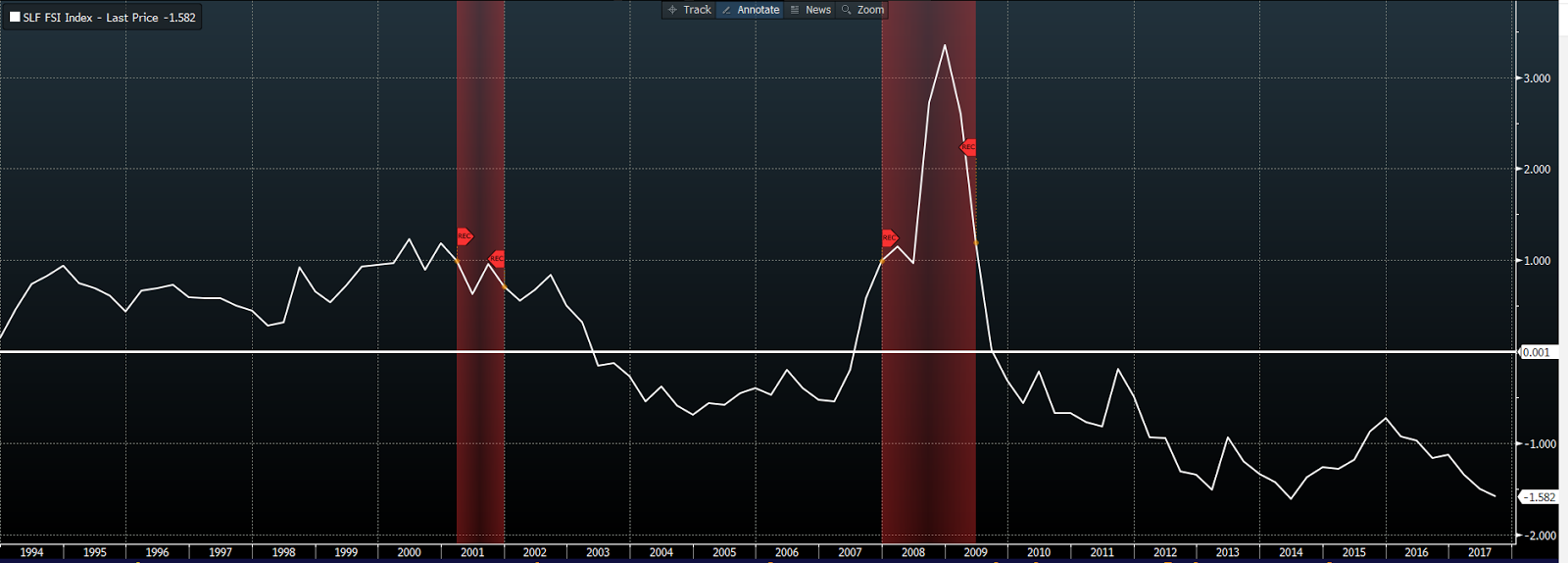

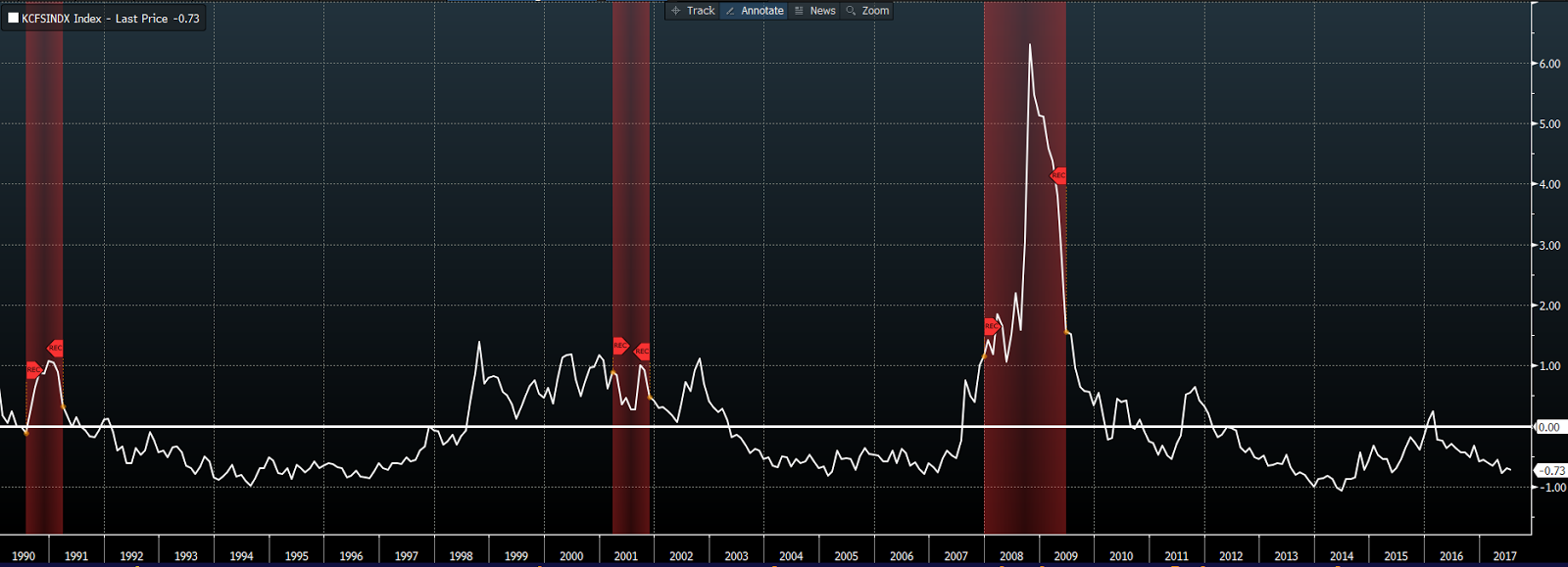

As for economic stress, here are the indicators I showed you last week. Compare present levels to those of past recessions (red shaded areas): Click here for definitions…

2-yr Treasury/Fed Funds Spread

Treasury Yield Curve:

Swap Spread

LIBOR/Fed Funds Spread

High Yield Credit Spread

Chicago Fed Financial Conditions Index

St. Louis Fed Financial Stress Index

Kansas City Fed Financial Stress Index

Bottom line: It’s this presently positive setup (bullish condition/lack of economic stress) that explains why events or circumstances that might otherwise be met with market turmoil (although, per the above, they may have virtually nothing to do with it) have thus far done little more than present buyable dips.

Of course this is all subject to — and ultimately will — change. We’ll keep you posted…

Have a great weekend!

Marty

.