We’ve expressed herein a few times of late (here’s one) our view that — rising/record home prices notwithstanding — today’s housing market does not nearly possess bubble characteristics.

To further support that notion, take a look at the latest quarterly Fed assessment of U.S. consumer credit, courtesy of Bespoke Investment Group. I.e., it takes a lot more (a lot more!!) than the ability to fog a mirror (the mid-2000s litmus test) to qualify for a mortgage these days:

click charts to enlarge…

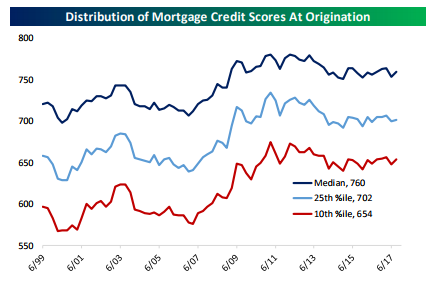

As shown in the chart, mortgage lending standards remain almost brutally high. Even the 10th percentile (i.e., worse than 90% of all loans). Experian describes FICOs of 670 an above as “good”, so that gives you an idea of just how tight mortgage credit has been in recent years; very, very few borrowers with low FICOs (and therefore a lower likelihood of repayment) have been given mortgages since the mid-2000s subprime debacle.

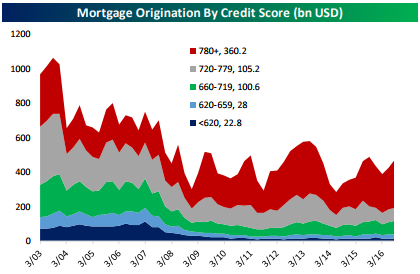

That’s resulted in low overall

mortgage origination. As shown

in the chart, mortgage

origination (both purchase and

refinancing) was running in the

$700bn range for most of the

mid-2000s, topping $1 trillion

earlier in the period. The modern

mortgage market does

around $500bn/quarter of volume,

drastically lower given

higher home prices and incomes

since the mid-2000s.

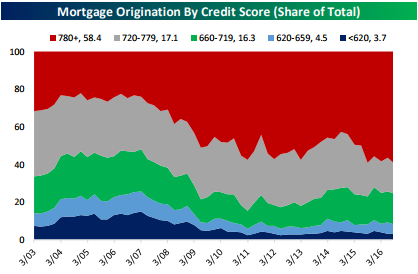

It’s also important to reemphasize

how high quality

mortgage lending has been on a

FICO basis. As shown in the

chart, about half of all

mortgage originations go to

FICOs north of 780; Experian

describes an 800 FICO as

“exceptional”, which really

serves to emphasize that it’s

only very high quality borrowers

with easy access to credit at

the moment.