Heading into a shortened workweek, it seems only fitting to offer up a shortened weekly message. Here goes:

While getting a jump on this week’s macro analysis over the weekend, I guessed that the forthcoming reading of the Index of Leading Economic Indicators would jump nicely given the positive look of many of the other 72 data points we track.

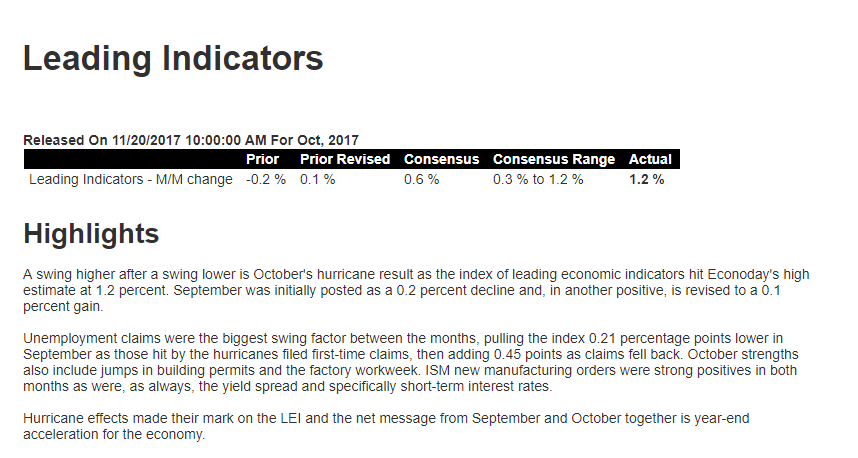

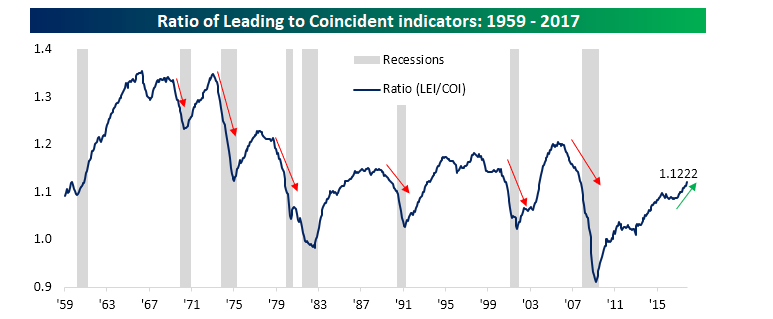

Sure enough: click any insert to enlarge…

While the above Bloomberg summary cites a hurricane rebound, the macro trends that are presently instructing our growthy equity sector targets were solidly in place prior to this year’s horrendous hurricane season.

Bespoke Investment Group does a nice analysis of the the relationship between leading and coincident indicators. As you can see in this chart of their leading/coincident indicator ratio, while anything’s possible, the odds of recession any time soon are remote:

Above, I mentioned the positive look of many of the data points we track: Actually “many” is somewhat of an understatement! As things stand this week, 75% of our indicators read positive, 4% read negative, with the remaining 21% in neutral mode. Our “macro score” came in at 52, which bested the previous all-time high (we’ve back-tested the past 20 years) of 50 (hit just two weeks ago).

Bottom line, you should be feeling good about the state of the economy as we head into the holiday season. Of course, mind you, the stock market can, and will — through its normal course of action — defy even the most bullish of macro setups. In other words, as we said in last week’s message:

…. please, make no mistake, positive setups are forever rife with negative setbacks. It’s called volatility; remember volatility?

Not to close on a negative note. Well, actually, we didn’t! Volatility is natural in the financial markets; lack thereof isn’t. So, hey, we closed on a positive note! I mean what could be better than the market acting naturally? 🙂

Happy Thanksgiving to you and yours!

Marty