In fact, here’s the bulk of my response to one such inquiry from yesterday:

Well, like I said in yesterday’s blog post, the macro setup is very good. The technical setup shows a little short-term weakness in a few spots, but long-term bullish trends are, for now, very much intact.

The Market will run as long as a positive setup and ample liquidity exists. Lately sentiment has been waning, which is a good thing because waning sentiment suggests there remains ample liquidity — the Fed’s moderate tightening notwithstanding.

Bull markets never die of old age, they die amid deteriorating conditions… conditions remain good for now. That said, I wouldn’t be surprised in the least to see a notable pickup in volatility after the first of the year, which, by itself, would not change our thesis.

As for the market’s present levels and the existing bull market’s duration, when we consider semiconductor stocks, we could almost get away with saying, we’re just now back to square one.

Take a look at this chart of the SOX (Semiconductor Index): click to enlarge

Yep, chip makers, as a group, are just now back to where they peaked 17 years ago!

So then, can we say that the party is finally back to where it left off nearly two-decades ago, and, therefore, it’s just getting started? Well, that 2000 high represented a tech bubble for the ages. Thus, one could make the case that it’s once again time for investors to cash in their chips; for the last time such a level was reached a three-year bear market ensued.

Of course the question thus becomes; today, is there once again a tech bubble in need of popping? Well, a couple things to consider:

1. Valuations: What were average price to earnings ratios back in 2000 compared to today.

2. General Conditions: What was the overall condition of the market and the economy back then?

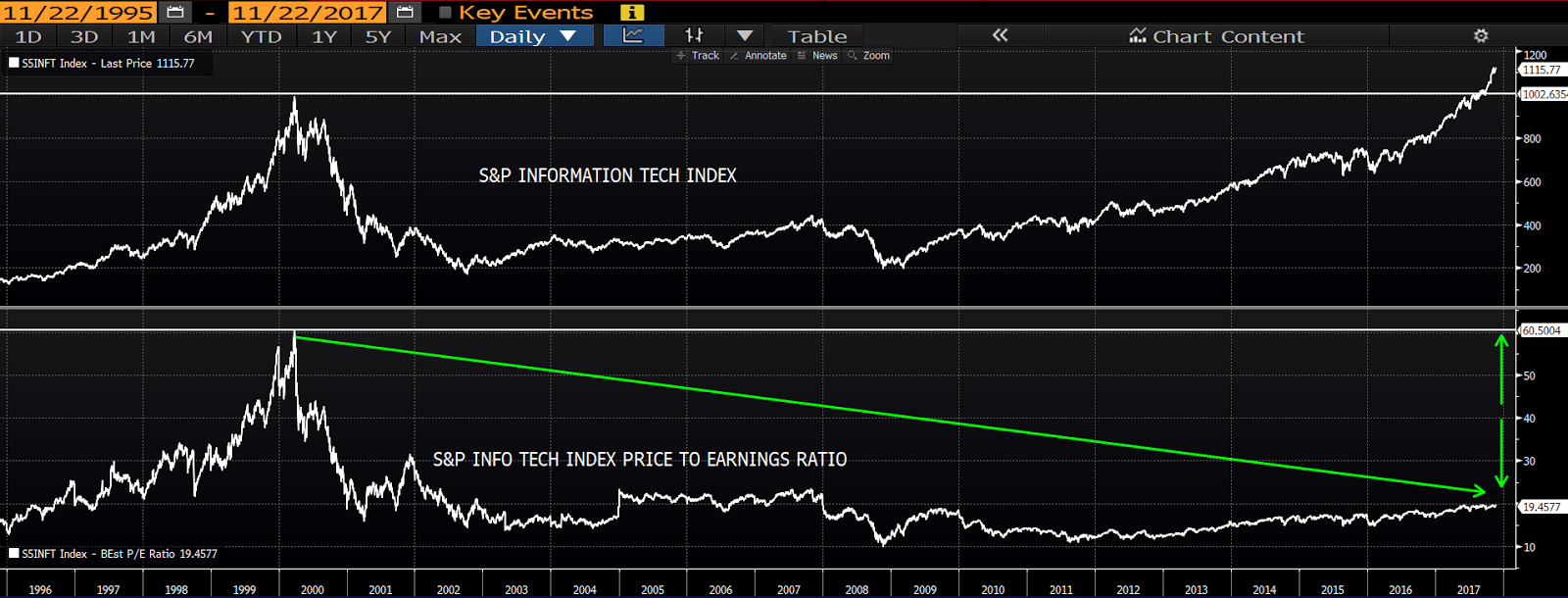

As for valuations, unfortunately we don’t have the p/e data for the SOX back that far, but we can proxy using the S&P Tech Index.

The top panel below shows the tech index’s price action (which has actually surpassed its 2000 high). The bottom panel is the average price to earnings ratio of the tech sector then versus now. As you can see, from a valuation standpoint, no, present valuations are epically below where they were in bubbly 2000: click to enlarge

In terms of general conditions; we back tested our macro model as of 08/11/2000 (just prior to the ultimate rollover into that massive bear market):

For that date it scored a -15; with 16% of our indicators reading positive, 47% negative, and 37% neutral. I.e., not your rosy outlook!

As of this Monday, the model scored a +52; with 75% reading positive, 4% negative, and 21% neutral. I.e., your rosy outlook!

So, again — while we forever caution that with markets anything can happen — we’re simply not experiencing that bubbly feeling right about now.