As we’ve been reporting, our analysis of current conditions suggests very low risk of recession on the near-term horizon. However, to some, one popular economic indicator — one that happens to be an important input to our weekly analysis — is flashing red! That would be what’s called the treasury yield curve.

Just yesterday a client asked me what I thought about the recently flattening curve; a very popular topic of late. My reply, edited for your reading pleasure, will serve as this week’s narrative.

With a normal yield curve the shortest term treasury security has the lowest interest rate, while longer term treasuries have higher rates. Rates tend to gradually rise as we extend the lengths of the securities (they rise as we “move out the curve”). I.e., the 2-year treasury security sports a higher rate than the 1-year, the 3-yr higher than the 2, the 5 higher than the 3, and so on.

When the curve, as they say, “flattens”, it means that the space between short and long-term yields has been compressing.

When the curve, as they say, “flattens”, it means that the space between short and long-term yields has been compressing.

We track the 2-year treasury vs the 10-year. An inverted yield curve (the prospects for which some folks are presently fretting) means, in my example, that the 10-year yield (interest rate on existing securities) has fallen below the 2-year yield (or the 2-year has risen above the 10). That (particularly the 10 falling below the 2) can be construed as a dire situation from an economic standpoint; which can be explained in a couple of ways:

1. If folks are piling into long-term treasury bonds (driving their price up and yield down) — in theory tying up their money — and not in other generally long-term investments like stocks, they gotta be worried about the prospects for those other long-term investments (i.e., worried about economic prospects).

2. Folks are so worried about economic prospects that they expect that the Fed will soon have to reduce interest rates: Locking up longer-term rates in a falling rate environment is a prudent, and profitable, thing to do.

More often than not, a recession ensues within 2-years of such an inversion.

Now, the problem with much of the recent rhetoric is the assumption that since the curve is flattening it’s destined to soon invert, and, thus, the next recession is in the offing. History, however, as illustrated in the charts, tells a very different story.

The flattening we’re currently seeing is classic, and completely normal, in the context of a Fed tightening cycle (the raising of the Fed funds rate, among other things). I.e., the yield curve virtually always flattens as the Fed initially steps up interest rate hikes. It’s not that the economy is suffering (the opposite in fact), it’s that the Fed Funds rate is very short-term, and, therefore, shorter rates must adjust rapidly in response (folks sell the short end of the curve forcing those rates higher), which occurs initially at a faster pace than the longer end, hence the flattening.

If indeed the Fed is correct and the economy is quite strong (the reason they’re hiking rates), the yield at the long-end of the curve will remain higher than the yield at the short end. In fact, more recently, the curve has begun to steepen back a bit

If indeed the Fed is correct and the economy is quite strong (the reason they’re hiking rates), the yield at the long-end of the curve will remain higher than the yield at the short end. In fact, more recently, the curve has begun to steepen back a bit

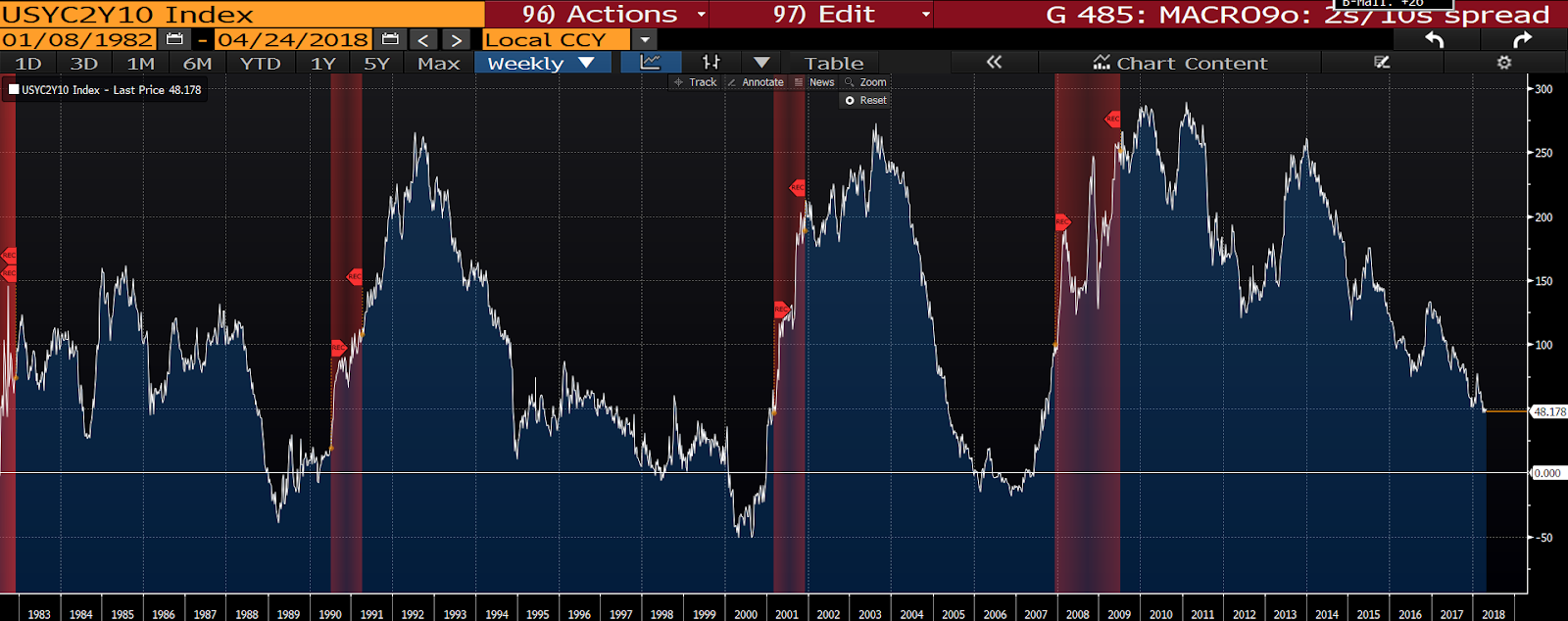

Here’s our chart of the 2s/10s curve. The dips below the white horizontal line are the inversions since the early 80s (red shaded areas are recessions). Note the flattening (or declining) periods during the 80s, 90s and 00s:

click to enlarge…

And here’s a chart where I actually separate the 2-yr (orange) and the 10-yr (blue) treasury yields in the lower panel. Take a look at the movement in rates as the yield curve changes over time. Note that during the inversions of the past 30+ years (red circles) rates were actually on the (or on the verge of) decline. And note how that’s very much not the case today:

As the presently higher trending 10-year yield suggests, folks are indeed not running to the safety of long-term bonds in fear of a looming recession; quite the opposite in fact.

Frankly, those who are trotting out the yield curve at this juncture (and there seems to be a lot of them lately) to paint a concerning picture of present conditions are doing their clients/readers a disservice: Deeper analysis clearly shows that today’s pattern doesn’t look at all like concerning patterns of the past.

Of course, and I assure you, we’ll eventually get to a recession-threatening setup. And when we do we’ll be screaming it from the rooftops here on the blog, and compensating for it in our clients’ portfolios. We’re just not there at the moment.

Have a nice week!

Marty