While my experience doesn’t entirely agree with Bloomberg’s analysts’ statement that a rising dollar is necessarily a net positive for stocks (the 20-yr monthly correlation is actually negative) — although there have absolutely have been periods when it appears as such — the point that equities receive foreign capital flows is, sadly, a seldom-spoken irrefutably inevitable benefit of trade.

(Bloomberg Intelligence) — If President Donald Trump gets his wish for dollar weakness, U.S. stocks could face relatively unexpected — and not altogether positive — outcomes. Recent trends buck the assumption that U.S. stocks should benefit from dollar weakness. Equities and the greenback are relishing capital flows into the U.S., energy stocks included. (07/24/18)

emphasis mine….

I.e., as I preach here ad nauseam, money we spend on foreign stuff that isn’t used to buy U.S. stuff all! comes back in the form of investment that supports your stock portfolio and helps keep U.S. borrowing costs (read treasury yields) down. China, for example, is the world’s largest buyer of U.S. treasuries. Imagine what happens if they stop! In other words, what happens if Americans stop accessing (or can’t access) the world market to buy the goods they want and need at the most competitive prices?

I know, many of you are thinking that we need to “level the playing field”. That’s fine, but just know that — all else equal — all that means is that there’ll be less money flowing into U.S. treasury securities (at a time when its sorely needed), as well as your stocks, and more toward the purchase U.S. goods. Whether or not that means more jobs and higher stock prices against the headwind of less capital flow and higher interest rates is a huge question at this stage of the cycle, believe me!

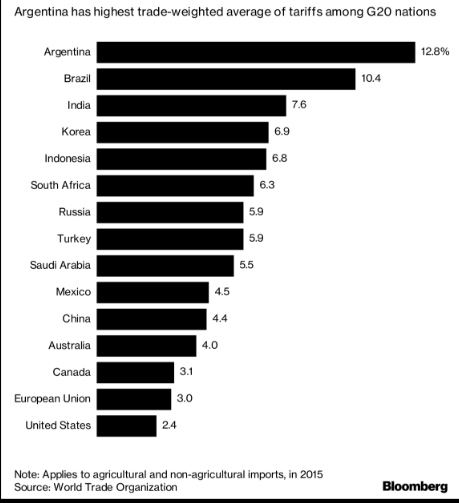

If, all of my pleas notwithstanding, you choose to stick with the “level playing field” argument, take a look at the average tariffs among G20 nations. Then ask yourself if “we’re” even challenging the right “opponents”: