Chinese stocks screamed higher last night on news that trade talks with the U.S. were constructive, as China pledged greater than previously-proposed measures related to IP theft and forced technology transfer.

Nonetheless, the S&P future contract is pointing to a +14-point opening, which pushes through what has been pretty stiff recent resistance at 2820. The sustainability of any move toward and beyond the last-September high will depend on the extent to which the tariff regime that is now inflicting real damage onto the global economy is dialed down.

Brexit looms large on markets as I type. The pound is rallying hard this morning on speculation that some Labour Party members could back Teresa May’s plan in a vote later this morning. Fallout there could notably mitigate any rally we see in U.S. equities today, while a surprise win for May would have stocks immediately screaming higher.

The macro data of late, while not all bad (or recessionary), clearly points to a general slowing of global economic activity.

As for what the market says about the state of the U.S. economy, I would characterize the latest signals as mixed: Tech and consumer discretionary stocks have outperformed the broader market in March (says good things). However, financials, materials and industrials have under-performed (not good things), while consumer staples and utilities stocks have been winners (also not good things). Again, mixed!

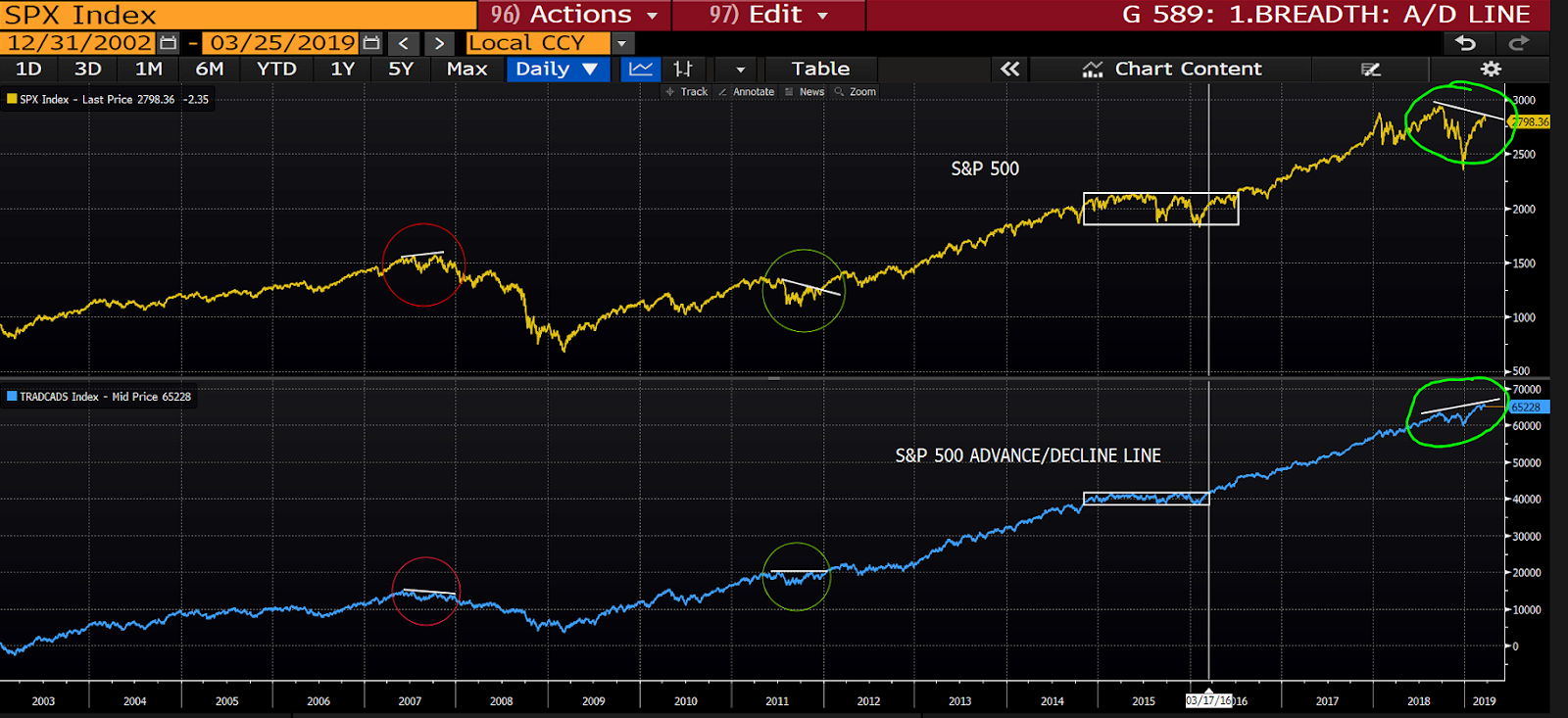

In terms of market breadth, the S&P advance/decline line continues to show a strong bullish divergence from price, that’s historically-speaking very positive.

Here’s the graph: click to enlarge…

Bottom line: General conditions remain just okay for now, which I’m certain will not be my characterization 6 months out. Conditions between now and then will grow markedly better or worse depending on how key policy decisions play out.