Two weeks ago yesterday I posted “A Telling Two Weeks to Come!“. In it I stated that the following pending events would help us gauge stock price-action going forward.

Week 1: The we-have-a-trade-deal announcement that was supposed to be announced a week ago last Friday (5/10). I suggested that if the deal did not eliminate at least the lion’s share of the tit-for-tat tariffs that it would not be welcomed by the markets.

Week 2: The deadline for Trump to declare foreign auto imports to be national security threats (sorry, but every time I type that one I have to add something along the lines of; I KID YOU NOT!), and impose 25% tariffs on European auto imports (again, sorry, I KID YOU NOT!).

Well, as for week 1, not only did we not get a deal that eliminated tariffs, we didn’t get a deal at all! In fact, the day after I wrote my “Telling” post, the President announced that he was increasing existing tariff rates and was likely to throw in the rest of the kitchen sink to boot. Of course that led to the worst week of the year for stocks.

As for week 2, well, thank goodness for week 1! I personally believe that had the previous-week market rout not occurred, it would’ve occurred in worse fashion in week 2 on news that the U.S. was indeed going to impose tariffs ASAP on Mercedes’s and Beemers. As it turned out, the market got the Administration’s attention and instead of announcing tariffs, it settled for a delay, along with a threatening statement; as I anticipated in last Tuesday’s post:

“I’ll be surprised, given the market’s reaction to the latest on trade, if Trump makes good on his threat to announce tariffs on EU autos this week. If he does, the market will tank further. If he doesn’t, and if he goes so far as to suggest that he has no intention to, we’ll likely see a meaningful rally. Although I suspect we’ll need to experience more pain in equities before we hear any such lasting (sounding) declarations. Thus, unless we get a further (and increasingly dramatic) meltdown in equities this week (certainly a possibility), inspiring a conciliatory statement, I expect the Administration will issue a tariff threat toward the EU, but take no action at this juncture.”

Per my Tuesday comment, however, we’re nowhere near out of the woods yet. In my view, nothing short of an all-out abandoning of the tariff tool (i.e., a complete rollback of the last year’s+ worth of tariff damage and an announced complete change of tack) will see the market sustainably into all-time high territory. Sadly, the Administration is nowhere near warming to such an about face at this point: I.e., there’s likely more market pain to come.

Speaking of more market pain, that’s what much of our latest research points to.

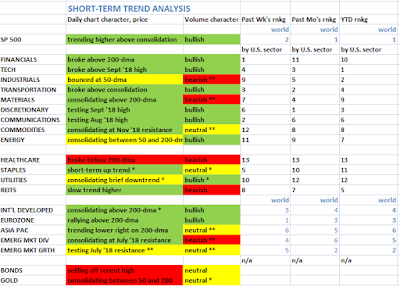

In my “Telling” post I featured some visuals: click inserts to enlarge…

I started with my April 15 short-term sector trend analysis:

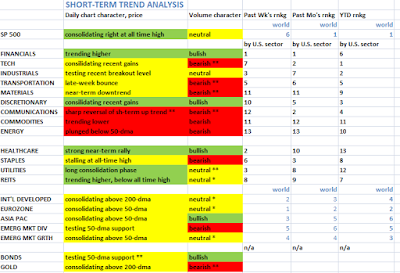

And compared it to the same analysis performed that morning:

I pointed to the deterioration you can see in the color changes.

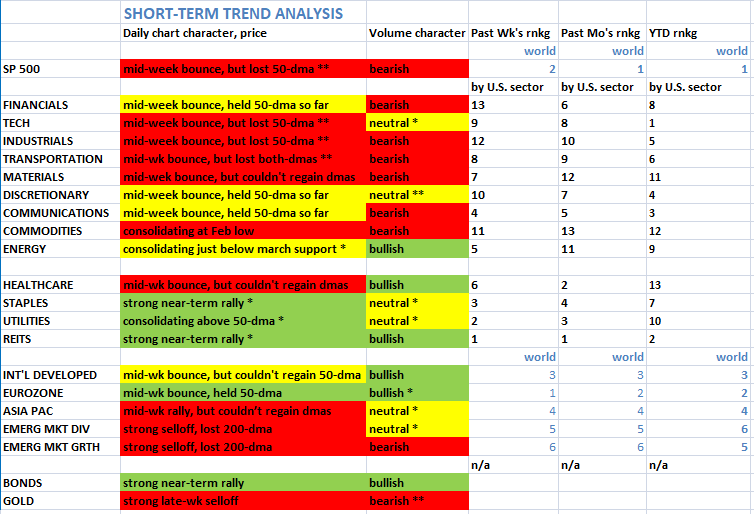

Now, here’s the same analysis as of yesterday:

Definitely not looking better at this point!

I also offered this graph and noted the “somewhat dicey short-term picture.”

Here it is as of this morning:

The market dipped right on cue!

I bring it all home with this brief must-watch video:

Here’s the link to the blog post I referenced in the video.