Just finished up my weekly deep dive into the market and economic fundamentals and technicals that matter — on both short and longer-term time frames — and I’ll tell ya, whether you’re a bull or a bear, the cherries are presently ripe for the picking, and it’s a bumper crop.

Make no mistake, if you happen to catch the guru of the hour on your chosen outlet for financial noise and she’s forecasting nothing but blue skies ahead, she’s cherry picking to the max. Conversely, if you switch stations and happen to catch their guru du jour and he’s telling you the longest expansion in history is done expanding and the next big bear market is about to begin, well, same thing; he’s mining only for data that fits his hypothesis.

Like I said, there’s plenty of cherries to go around, whether you’re a bull or a bear.

To help the bull case, here’s a small sampling taken from our weekly analysis:

S&P 500 200-Day Moving Average: click any insert below to enlarge…

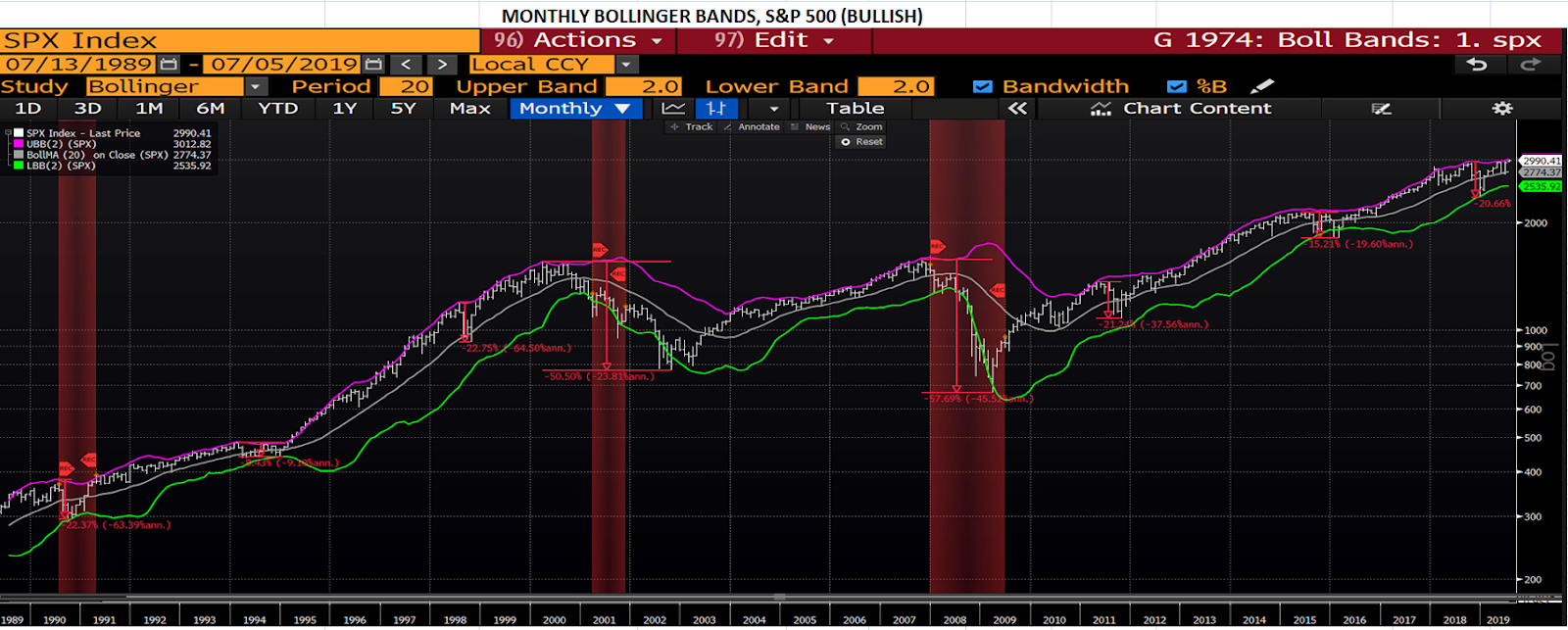

Monthly Bollinger Bands:

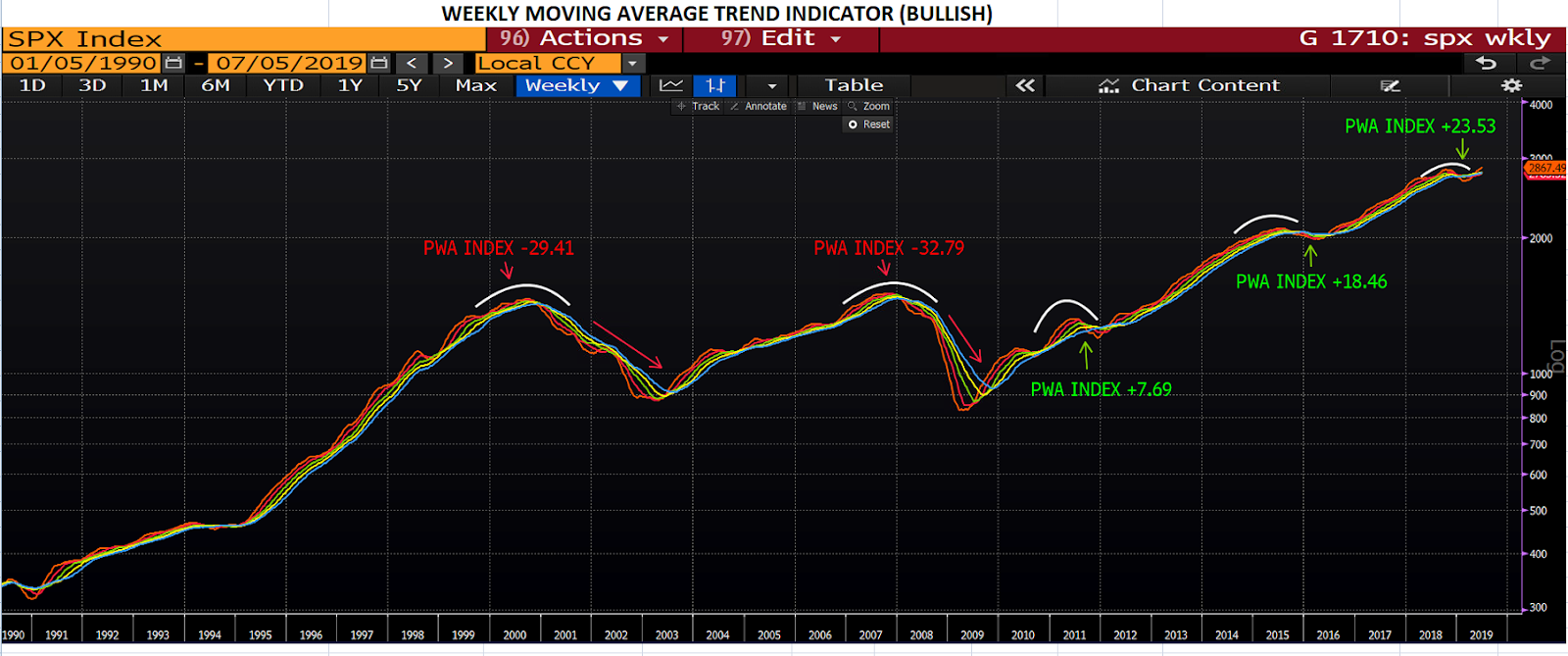

20 to 60-Week Move Averages With PWA Index Score:

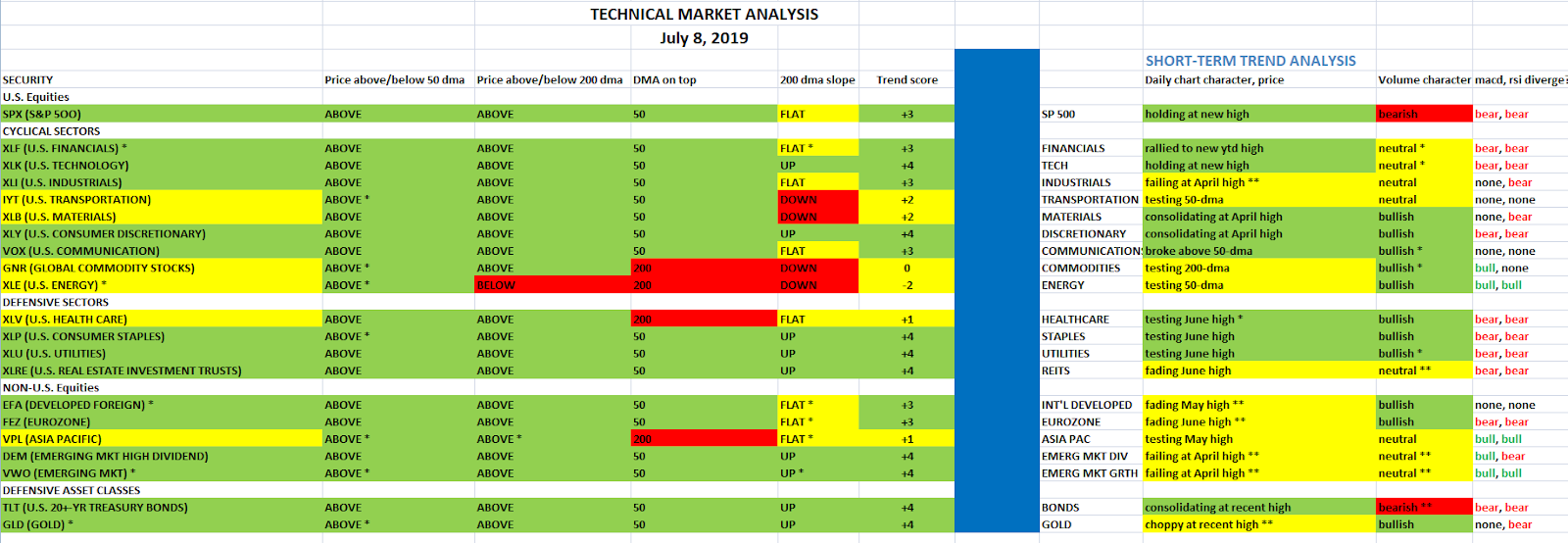

Our Weekly Long and Short-Term Trend Analysis By Sector and Region:

While there’s a bit of red on the last insert above, all in all, these four displays paint a pretty healthy picture of the financial markets.

Ah, but if you’re a bear, you could trot out the following (also from our weekly analysis):

S&P 500 Weekly MACD and RSI (flashing bearish divergences that often precede market tops):

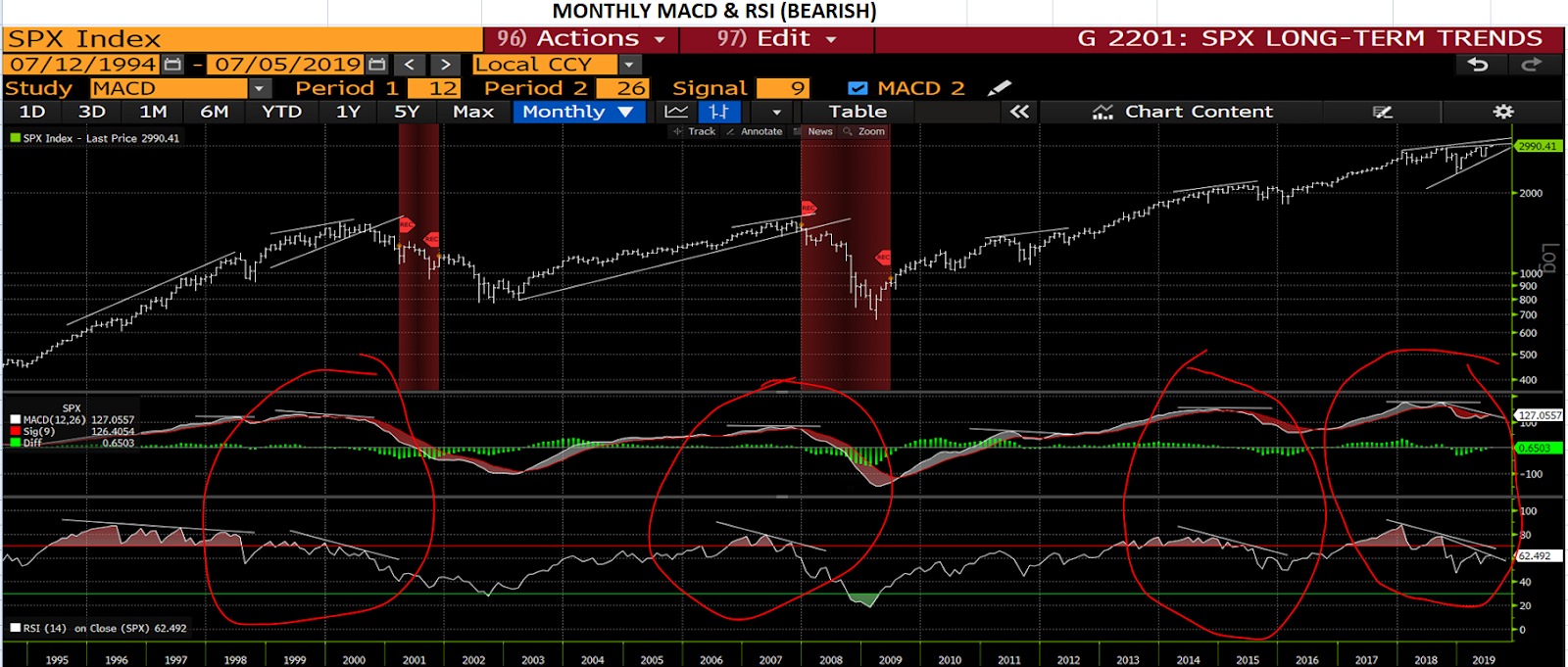

Monthly MACD and RSI (flashing bearish divergences; and there tend to be less false signals in the monthlies vs the weeklies):

Smallcaps and Transports Lagging The Broader Market (historically bearish signal):

![]()

The Stock/Bond Ratio Flashing Historic Warning Sign:

Any good bear could paint an ominous picture out of those last four inserts.

Bottom line, the market’s in a precarious spot. Typically, while our own macro index scores in the green (+23.53 this week) we consider market selloffs regardless of size to be healthy phenomena within the context of an ongoing expansion and bull market. Presently, however, I’m struggling more than usual with the direction of some of the data.

Here’s an example: While the ISM Manufacturing and Services Surveys (hugely important snapshots of general conditions) still score above 50 (denotes expansion), the latest trend concerns me:

Not that, as you can see, sentiment doesn’t dip and recover outside of recessions (red shaded areas), what troubles me this go-round is that the source of the sour mood is anything but cyclical phenomena, nope, it’s purely political (read trade war), and it’s pernicious enough to throw the global economy into recession long before its time.

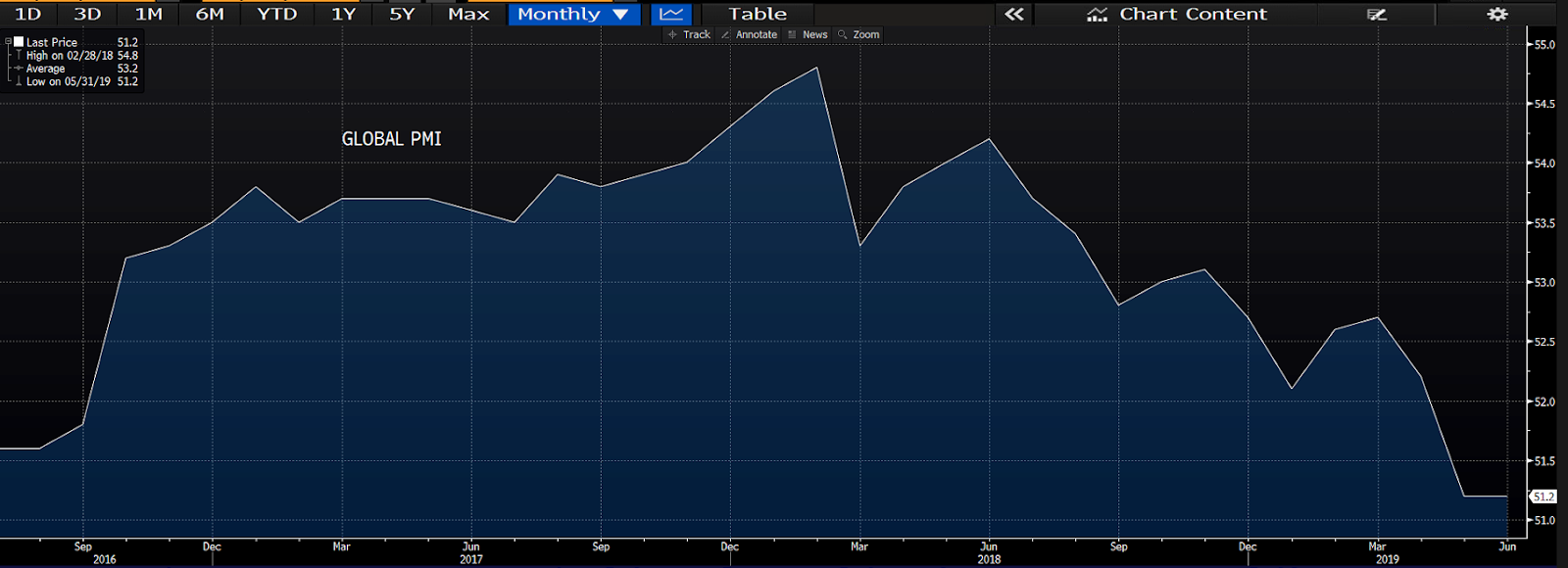

Case in point, the Global Purchasing Managers Index (PMI) is now sitting at a 10-year low:

Make no mistake folks, when producers are stressed they pull in. I.e., they stop expanding operations and it ultimately bleeds into the rest of the economy.

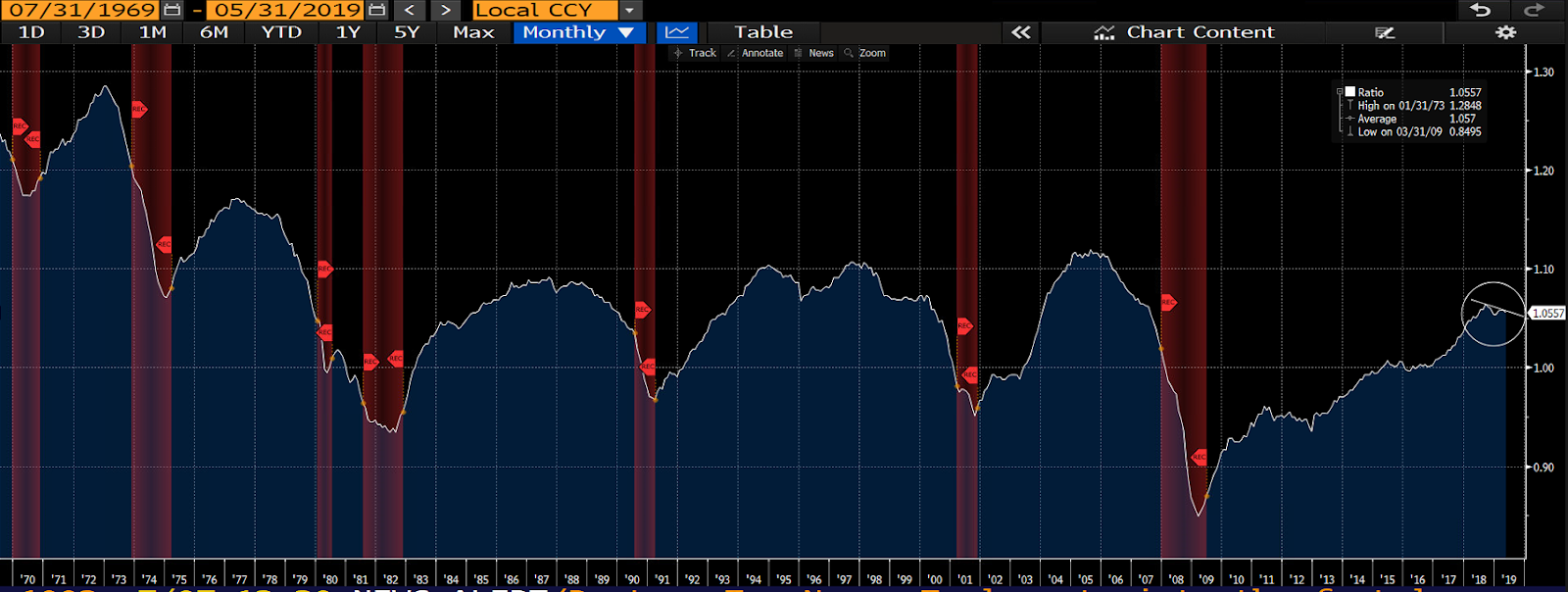

Here’s our LEI (Leading Economic Indicators)/CEI (Coincident Economic Indicators) Ratio chart: The line rises when leading indicators are scoring higher than coincident indicators [denoting good times ahead], and declines when the future gets iffy:

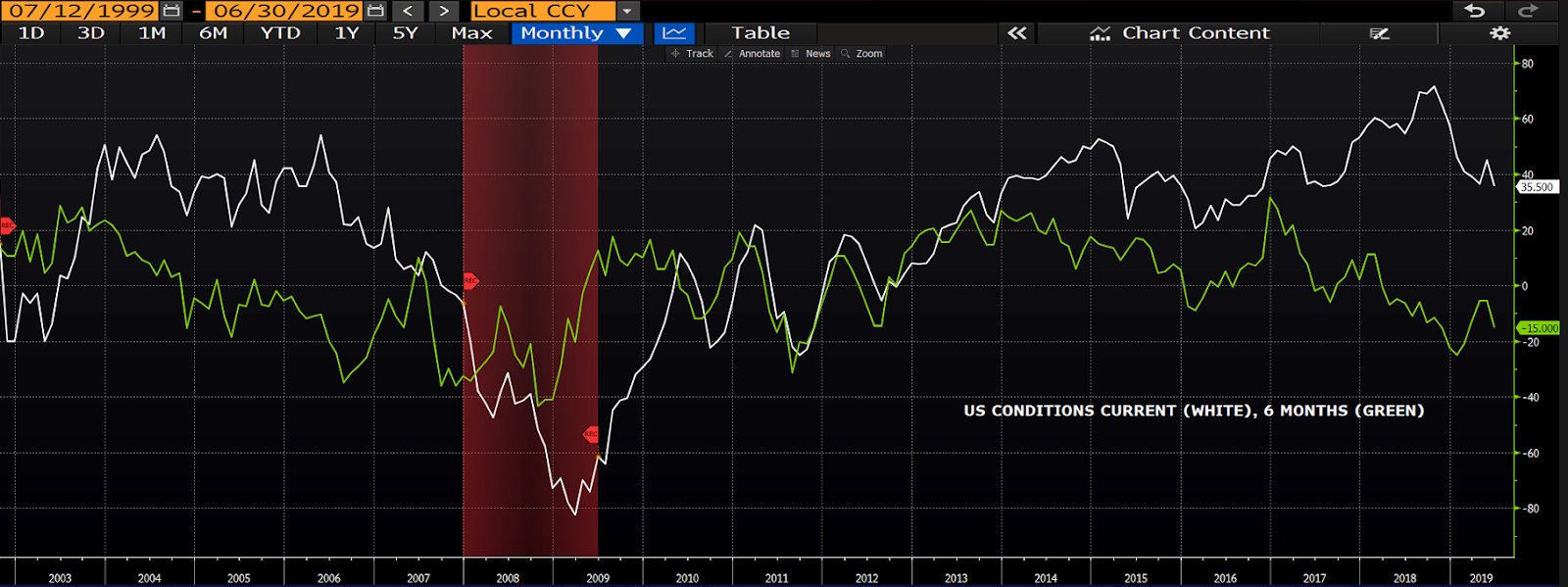

And, lastly, take a look at the Global Sentix Institutional Investor Sentiment Index (white = current conditions, green = 6-month outlook):

Here’s for the U.S.:

To sum it all up, the stock market is at all time highs and futures are pricing in a 100% chance of a Fed rate cut later this month. The latter suggests something isn’t right.

Now, we have to assume (and pray!) that the Fed cuts for entirely economic reasons, as opposed to bowing to political pressure from the White House. Otherwise, we’d be risking a Richard Nixon/Arthur Burns (Fed chair at the time) scenario; Burns did Nixon’s political bidding, which ultimately brought us the monster inflation of the late-70s and early-80s. That’s right, Carter (and OPEC) got a bum rap on that one…

Here’s that sad story:

Winning Elections: Nixon fired Fed Chairman William McChesney Martin and installed presidential counselor Arthur Burns as Martin’s successor in early 1971. Although the Fed is supposed to be solely dedicated to money creation policies that promote growth without excessive inflation, Burns was quickly taught the political facts of life. Nixon wanted cheap money: low-interest rates that would promote growth in the short-term and make the economy seem strong as voters were casting ballots.

Because I Say So! In public and private Nixon turned the pressure on Burns. William Greider, in his book “Secrets of the Temple: How the Federal Reserve Runs The Country” reports Nixon as saying: “We’ll take inflation if necessary, but we can’t take unemployment.” The nation eventually had an abundance of both. Burns, and the Fed’s Open Market Committee which decided on money creation policies, soon provided cheap money.

It worked in the short term. Nixon carried 49 out of 50 states in the election. Democrats easily held Congress. Inflation was in the low single digits, but there was a price to pay in higher inflation after all the election year champagne was guzzled.

In the winters of 1972 and 1973, Burns began to worry about inflation. In 1973, inflation more than doubled to 8.8%. Later in the decade, it would go to 12%. By 1980, inflation was at 14%. Was the United States about to become a Weimar Republic? Some actually thought that the great inflation was a good thing.

The Bottom Line: It would take another Fed chairman and a brutal policy of tight money, including the acceptance of a recession before inflation would return to low single digits. But, in the meantime, the U.S. would endure jobless numbers that exceeded 10%. Millions of Americans were angry by the late 1970s and early 1980s.

If Trump’s right on his assessment of the present economy (“best in history”), the Fed cutting rates into that environment would lead to something very very ugly (like 70’s inflation and/or the ’08 bubble-busting recession). The good news — as it relates only to what the Fed is contemplating — is that while the economy is still in decent shape there are indeed cracks forming, which allows us to assume for now that the Fed absolutely knows what it’s doing, and is doing it holistically, not politically.