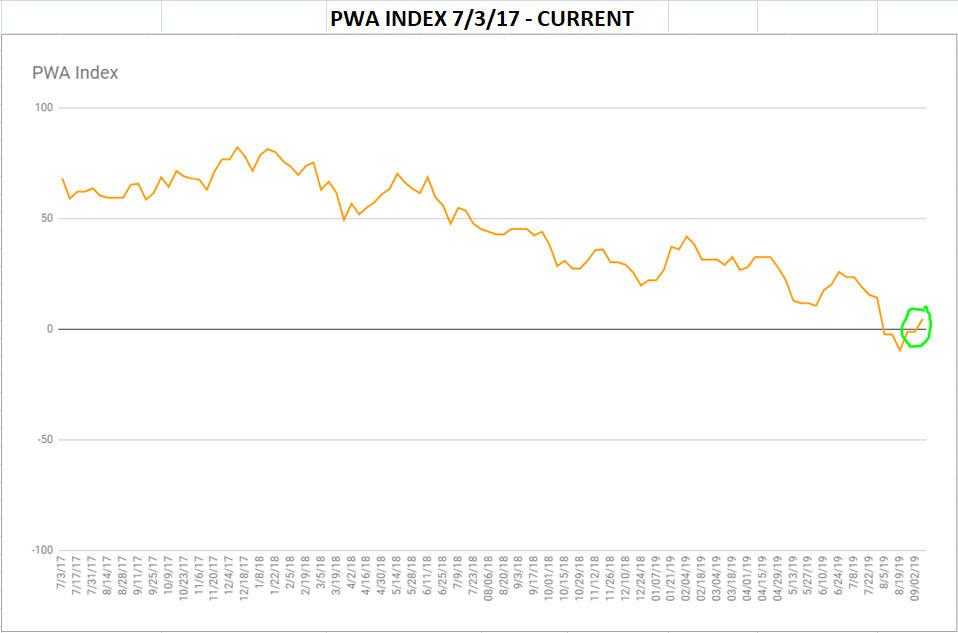

The good news this week is that our proprietary macro index broke a 5-week string of negative (heightened recession risk) readings, coming in at +4.65.

The not-so-good news is that 100% of the improvement occurred (thanks to the recent rally in stocks) within the financial markets subindex; itself improving by 22.1 points on the week — while the financial stress subindex didn’t budge from its concerning, yet not panicky, score of -10, and the economic subindex came in at an uninspiring +11.11; giving up 1.85 points on the week.

In a nutshell, the consumer (scoring a strong +56.25) continues to carry the load for the economy, while the business data remain a drag (-20).

Note: The range for the index, as well as each component subindex, is +100 to -100…

Fed Chair J. Powell this morning, while speaking in Zurich, did a masterful job of not roiling the market, as he has had a tendency to do. He essentially reported that the economy remains in okay shape, with the trade war being the existential risk. The market’s lack of reaction says to me that a .25% rate cut would be just fine, all things considered.

Back to our index: Here’s the graph since inception: click to enlarge…

While, again, it’s good news to see the score above zero, the overall trend since the January ’18 peak remains very concerning.

As I’ve pounded herein, and on the videos, the long-term technical setup looks too much like pre-recessionary/bear market periods, to, when coupled with a weakening macro trend, allow for anything but a relatively cautious approach to investing at this juncture.

Speaking of the videos, I’ll close this week’s message right here and post the past two days-worth below.

Between the two (if you haven’t watched them already), you’ll catch what I mean regarding the long-term technical setup, what our index suggests today relative to historical back-testing, as well as my take on today’s jobs number and the recent rally in stocks:

This morning’s video:

Yesterday’s:

Have a great weekend!

Marty