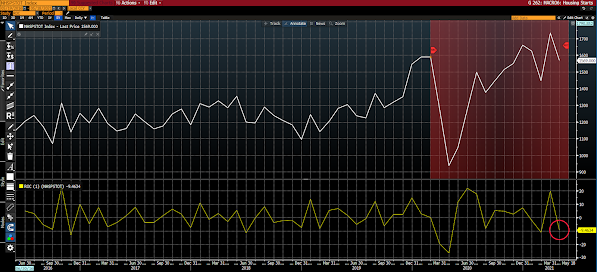

In yesterday’s morning note I featured my weekend comment regarding the positioning of speculators who trade lumber futures:

“Lumber net longs dropped notably, now nearly neutral. Speaks to the huge, unsustainable runup in price, and evidence of project delays and cancellations.”

Evidence of that implied pullback in production exhibited itself in this morning’s housing starts numbers for April:

After rallying bigly on news that it’s selling its media stake, AT&T reversed course in yesterday’s session — and is taking it the chin bigly this morning as well. What is likely a long-term win for shareholders (shedding a ton of debt and ending up with 71% ownership of a new streaming giant when the deal’s done) isn’t enough — for the moment — to offset the disappointment of a dividend cut that’ll take this huge yielder from roughly 6.5% to what’ll likely settle in at around 4% going forward (based on current price).

Yep, lots of folks like AT&T for the yield. We do as well. But, as a core position, it’s always been first and foremost a telecom/coming-5G play for us. It’s still that — more so now — of course, but nevertheless we’ll be reassessing whether or not it remains the best use of ~1.5% of our portfolio (there’s lots we like in the resource and emerging markets space these days)…

“The Americans have lost interest in being the global policeman, security guarantor, referee, financier, and market of first and last resort. The people who remember the world wars personally are almost gone, and the oldest of those born after the age of the Soviet nuclear threat have already voted in three presidential elections.

It is difficult to justify an Order when the people doing the justifying weren’t even alive when the circumstances that necessitated its creation occurred.” — Zeihan, Peter. Disunited Nations