Yesterday, I touched on the resoundingly negative breadth that conflicted with positive moves in the major averages. While this morning’s breadth is a touch more tolerable, it’s still nothing to write home about.

As I type the S&P 500 is up 0.41% while just over 40% of its members are in the red. The Nasdaq Comp’s up 0.60%, while roughly half of its members are trading lower so far this morning…

Hmm… what’s that say about market internals?

Well, historically-speaking, it’s a red flag. But I must say, today’s market has become so, let’s say intervened in, injected, or however you’d describe a market that garners unrelenting attention from policymakers, that historical red flags have been utterly useless indicators since, say, last spring…

Nevertheless, breadth — timing signal or not — indeed remains an important tell in terms of overall market health, therefore we’ll continue to track and consider it in our own assessments of general conditions.

Digging deeper than simply the daily noise, here’s Bespoke Investment Group on the present state of affairs:

“While the cap-weighted S&P 500 is less than 2% from all-time highs, the average stock in the S&P 1500 index (made up of large-caps, mid-caps, and small-caps) is 15.8% from its 52-week high.”

Remarkable! Everybody’s U.S. benchmark is essentially at all time highs, while the average stock across the broader market is off its yearly high to nearly bear market proportions!

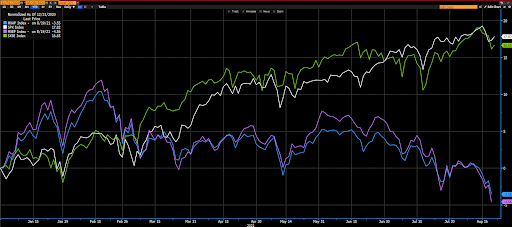

In terms of breadth globally, well, save for Europe hanging in there, let’s just say it’s been a rough relative road of late for global macro managers.

White line = SP500, green = Europe, blue = Developed Asia-Pad, purple = Emerging Markets — Year-To-Date:

The delta variant no doubt explains much about that chart. Now imagine the catch up to come when the numbers begin to peak — or, alas, the catch down, in the meantime, should it take larger hold in the western world.

When I mentioned yesterday that we’re targeting early Q4 to maybe take a modest slice from fixed income and strategically increase our best (and most unloved of late) long-term ideas — but added that if this keeps up we might go there sooner (appropriately hedging at the same time, by the way) — the above represents some of what I was talking about.

That said, if we’re anything, we’re patient… Happens (as a necessity) when one’s banged one’s head against markets for 36 years 😎…

Asia was mixed overnight, with half of the 16 markets we track closing lower.

Europe’s catching a bid this morning, with all but 6 of the 19 bourses we follow in the green as I type.

U.S. major averages are in rally mode (more so, and with a bit better breadth, than when I began this note): Dow up 173 points (0.49%), SP500 up 0.62%, SP500 Equal Weight up 0.37%, Nasdaq 100 up 0.95%, Nasdaq Comp up 0.94%, Russell 2000 up 0.57%.

The VIX sits at 19.32, down 10.80%

Oil futures are down 0.69%, gold’s down 0.08%, silver’s down 1.12%, copper futures are up 2.07% and the ag complex is down 0.34%.

The 10-year treasury is down (yield up) and the dollar is up 0.03%.

Led by solar stocks, ALB (lithium miner), AMD (chip maker), tech stocks and AT&T — but dragged by silver, Latin American equities, KRBN (carbon credits), uranium and gold miners — our core mix is off 0.03% to start the session.

Howard Marx’s Mastering the Market Cycle: Getting the Odds on Your Side is a must read for any serious investor, or advisor. The disregarding of cycles he refers to in the following quote can only happen when the price action deviates from underlying cyclical reality, which has the unsuspecting investor forever chasing what’s hot.

Understanding cycles and price trends, therefore, has the diligent investor/advisor allocating accordingly, then waiting patiently as things logically unfold. Again, as I’ve come to learn (in head-pounding fashion over the decades), patience is key!

“Invariably, investors who disregard where they stand in cycles are bound to suffer serious consequences.”