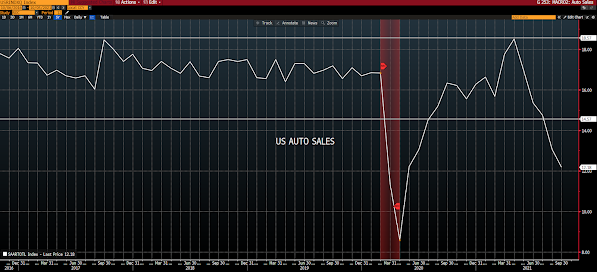

In our portfolio discussion yesterday Nick and I pondered the coming earnings season. The key question: How are companies going to handle their forward guidance when so many are hamstrung by lack of necessary materials, components and such?

The Auto industry for example:

“While Europe is in a power plant/natural gas/coal crisis with prices spiking, I read this on BN today, “European banks are beginning to drop clients that pose a climate risk rather than face the possibility of higher capital requirements, according to the watchdog overseeing the development…There’s already evidence that upstream oil and gas projects are falling out of favor as banks move beyond coal exclusions.” The transition to ‘clean’ is all well and good but if the ‘clean’ part is not fully ready to take the baton from the ‘dirty’ than getting rid of the ‘dirty’ will only result in sharply higher prices for energy everywhere which will in particular hurt parts of the world least able to afford it. I remain bullish on energy stocks, particularly the European majors.”

September’s swoon in stocks seems to have done a number on sentiment.

From several conversations with clients who’ve been around a few market blocks in their day I gather that there’s worry afoot. Our own “PWA Fear/Greed Barometer” has moved from signaling notably bullish sentiment to slightly bearish over the past few weeks.

While, as I expressed in last week’s main message, yes, there’s heightened cause for concern right here (trading patterns of late alone are suspect), seasonality and ultimately political constraints favor Q4, assuming some of the dust (debt ceilings, spending bills, Fed appointments, yada yada) settles early on.

Now, Q4 looking, at the margin, okay or not, there remains major risk underneath these markets. Hence we’re staying uber-diversified and are actively hedging…

Asian equities leaned green overnight with 8 of the 14 open markets (on-shore China remains on holiday) we track closing higher. Note, however, Japan was down over 3%, So Korea nearly 2%.

Europe’s leaning slightly red this morning, with 11 of the 19 bourses we follow trading lower, as I type.

U.S. stocks are attempting a comeback from yesterday’s drubbing: Dow up 303 points (0.89%), SP500 up 0.97%, SP500 Equal Weight up 0.82%, Nasdaq 100 up 1.14%, Nasdaq Comp up 1.11%, Russell 2000 up 0.74%.

The VIX sits at 21.46, down 6.53%.

Oil futures are up 1.82%, gold’s down 1.04%, silver’s down 0.86%, copper futures are down 1.42% and the ag complex is down 0.77%.

The 10-year treasury is down (yield up) and the dollar is up 0.25%.

Led by Nokia, energy stocks, ALB (lithium miner), KRBN (carbon credits) and uranium miners — but dragged notably by gold, base metals futures, sliver, ag futures and metals miners — our core portfolio is up 0.33% to start the session

While it’s easy to get all sideways over politicians’ preferences when they don’t comport with one’s view of how things “should” be, there’s a reason why I listed “political constraints” among the reasons to feel okay about Q4: You see, preferences are optional, constraints aren’t. A point Marko Papic makes in his excellent book Geopolitical Alpha:

“…constraints anchor the smart investor to a subjective probability grounded in material reality.”“The punchline: investors (and anyone interested in forecasting politics) should focus on material constraints, not policymaker preferences.”

Have a great day!

Marty