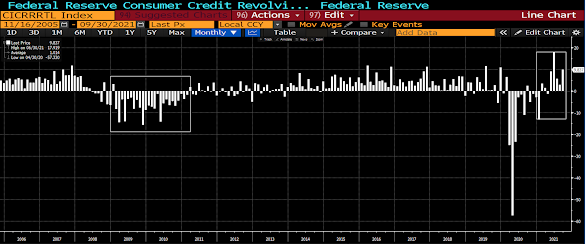

Here’s the monthly change in consumer revolving debt. Note the big jump in credit card usage over the past few months vs the 2 years+ of frugality following the 2008 recession:

Yep, it’s way different this time!

Clearly, the above (the latest reading anyway) and this morning’s positive retail sales numbers flies directly in the face of last Friday’s dismal consumer confidence report.

Either, as they say, actions speak louder than words, or folks are simply spending it (their savings and space on their credit cards) while they got it. As I mentioned in our latest macro update, U.S. consumers presently sit on some $2 trillion of savings… well, I guess (per the retail numbers) they’re not exactly “sitting” on it these days.

With regard to credit cards, after the big paydown during the pandemic there’s definitely more room to run going forward. And that, coupled with all of that savings, has some economists and market actors feeling pretty good about next year’s prospects. Makes sense, but keep in mind, while all of that government largesse still sloshes through the system, there’ll be no matching (not remotely) last year’s injections…

The dollar’s been on a tear of late, which, as I’ve promised, should it become the long-term trend, ultimately poses a threat to asset markets (in of course dollar terms). Ironically, save for yesterday and today, it occurred amid a nice rally across the commodity space (helping our core portfolio to a nice week last week while equity markets struggled).

Suffice to say that commodities are responding to inflation pressures, the dollar to rising rate pressures (as well as the dynamics around other nations’ currencies).

Ultimately, it’s safe to assume, something’s gotta give. Either the dollar retreats, providing a tailwind for commodities, or the dollar continues to soar, providing a potentially tough to buck headwind for commodities. You know our longer-term position on the topic. Although, yes, like last week, both do move in tandem at times, headwinds aside…

I’ll tackle the dollar in my next technical update. Here’s a sneak peek:

Asian equities leaned red overnight, with 9 of the 16 markets we track closing lower.

Same for Europe so far this morning, with 10 of the 19 bourses we follow trading lower, as I type.

We’ll call U.S. major averages mixed, although, save for the Russell 2000, the indices we report on herein are in the green (but only slightly). The mixedness shows up in the breadth. While the S&P’s green, 40% of its constituents are in the red. The Nasdaq Comp, also trading higher, is actually seeing its losers outnumber its winners by nearly 2 to 1 so far this morning:

Dow up 94 points (0.25%), SP500 up 0,20%, SP500 Equal Weight up 0.12%, Nasdaq 100 up 0.17%, Nasdaq Comp up 0.16%, Russell 2000 down 0.37%.

Oil futures are down 0.89%, gold’s down 0.11%, silver’s down 0.34%, copper futures are down 1.59% and the ag complex is down 0.15%.

The 10-year treasury is up (yield down) and the dollar is up a not-small 0.35%.

Led by AMD, water infrastructure stocks, KRBN (carbon credits), healthcare stocks, German equities and Nokia — but dragged by miners, Latin American equities, Viacom/CBS, base metals futures and Indian equities — our core portfolio is off 0.17% to start the day.

Read the following quote carefully and see if it strikes a chord (HT John Hussman):

“One of the striking features of the past five years has been the domination of the financial scene by purely psychological elements. In previous bull markets the rise in stock prices remained in fairly close relationship with the improvement in business during the greater part of the cycle; it was only in its invariably short-lived culminating phase that quotations were forced to disproportionate heights by the unbridled optimism of the speculative contingent. But in the 1921-1933 cycle this ‘culminating phase’ lasted for years instead of months, and it drew its support not from a group of speculators but from the entire financial community. The ‘new era’ doctrine – that ‘good’ stocks were sound investments regardless of how high the price paid for them – was at bottom only a means of rationalizing under the title of ‘investment’ the well-nigh universal capitulation to the gambling fever.

That enormous profits should have turned into still more colossal losses, that new theories should have been developed and later discredited, that unlimited optimism should have been succeeded by the deepest despair are all in strict accord with age-old tradition.”

– Benjamin Graham & David Dodd, Security Analysis, 1934