We subtitled our May 13th of this year message “Our Present Inflation Narrative — and the Potential For Something ‘Long-Term’ Special In Commodities.”

Now, all that said, before we settle into that structurally rising inflation scenario (if indeed that’s where we’re headed), I look for a notable calming of the thrust we’re presently experiencing — as the worst of the production bottlenecks subside — inspiring a chorus of I-TOLD-YOU-SOs from the “it’s transitory” camp.

Thereafter, I suspect we’ll see inflation settle into a steadily rising structural trend, and in the process fuel what will likely turn out to be the next longer-term commodity supercycle.

As you can see (green trend lines on the 50-year chart below), commodity bull markets tend to last a very long time. This one — while, per my mentions in recent video commentaries, I anticipate a potentially notable (and healthy) correction in the not too distant future — is just getting underway:

And while we’ve yet to see that letup in the inflation prints (we expect it as we move into 2022), we are indeed seeing the corrective action we expected in commodities.

Here’s a year-to-date look at the (above-referenced) Bloomberg Commodity Index; shaded area captures the date of the above-referenced blog post to current:

Updating the long-term chart, you can see, recent corrective action aside, that the new nascent up trend remains intact:

Unlike US stocks in the aggregate, commodities as a group have a long way to go before threatening their all-time highs.

Here again are the main bullet points from our longer-term inflation thesis:

- Increasing populism (a serious headwind for global trade — in both goods and labor).

- A continual stimulating of the economy via fiscal policy (facilitated by easy monetary policy) — demanded by a politically-powerful populist movement.

- China maturing into a service-oriented, consumer-driven economy (while moving away from providing cheap labor and goods to the outside world).

- The Fed’s fear of bursting present asset and debt bubbles were it to implement traditional inflation-fighting measures — thus willing to fall notably behind the inflation curve well into the foreseeable future. In fact, I personally place better than 50/50 odds that if indeed a long-term trend of rising inflation emerges, that the Fed will revert to yield curve control (buying up the price (down the yield) of longer-term treasuries) to control lending rates that, were they allowed to rise, would themselves produce a headwind to rising inflation.

- The trillions of dollar-denominated debt sitting on foreign corporate balance sheets inspiring an active campaign by the Fed to keep the dollar at bay, in an effort to avert what could otherwise turn into very messy global currency crises.

- The reticence of producers in the metals space to aggressively expand capacity despite rising prices: Speaks to the devastation they experienced post the ‘08 to ‘11 China building boom.

- Aggressive and exceedingly commodity-intensive global green energy ambitions.

- The political/environmental headwinds for fossil fuel producers to expand capacity.

- Inflation being the US’s historically-preferred mechanism for reducing heavy federal debt burdens.

Now, while, again, we do anticipate a letup in inflationary pressures as bottlenecks ease, if — structural pressures notwithstanding — you’re sympathetic to the notion that COVID-explained supply constraints entirely explain the decades-high inflation we’re currently experiencing, allow me to disabuse you of that popular notion.

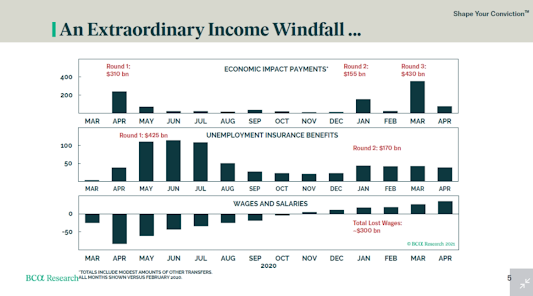

The bars in the top two panels track the amount of direct-to-consumer government payments made for the 12 months to April of this year. The bottom panel represents wages and salaries across the US workforce: