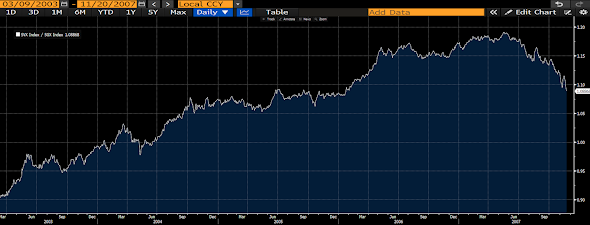

Before we explain what the first graph below represents, have a look at its price action during the 90s tech-fueled bull market:

Then the period that captured the bottom of the 90s tech bubble burst to the top of the subsequent real estate/mortgage bubble:

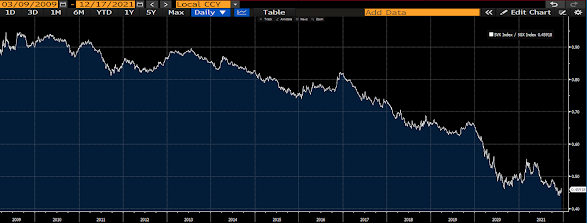

And now from the bottom of the real estate/mortgage bubble burst to current:

So, from a multi-year investment standpoint, does the above look presently appetizing, or timely, to you?

Assuming you’re a person who likes to buy “value”, or, let’s say, buy quality stuff when it’s relatively cheap, I imagine you’re nodding your head yes.

The above represents the results of US large cap value stocks (via the S&P 500 Value Index) compared to US large cap growth stocks (via the S&P 500 Growth Index). A rising line denotes value outperforming growth, a falling line says growth was the place to be.

Here’s another comparison to consider:

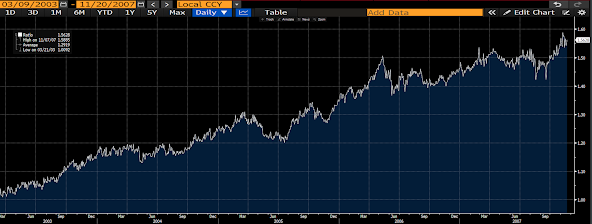

During the 90s bull market:

From the tech bubble burst to the real estate/mortgage bubble top:

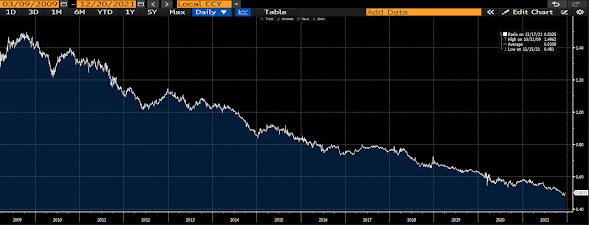

From the real estate/mortgage bubble burst to current:

Same question. Would you?

I presume yes.

That was the ratio of developed foreign market equities (represented by the MSCI Europe, Australasia and Far East Index) to large cap US equities (represented by the S&P 500 Index). A rising line denotes foreign outperforming US, a falling line says US was the place to be.

Now, before we expand our case for why we’re somewhat diverting our allocation away from where the momentum’s been these past many years — beyond the compelling historical evidence that extended periods of underperformance tend to be followed by extended periods of outperformance — we want to make very clear that whether we’re talking growth, value, US or Non-US, we presently view equity markets in a skating-on-historically-thin-ice sense.

Therefore, while we’re not predicting that some great collapse is in the offing, we’re continuing to take measures designed to limit the hit should one occur.

Note: While said measures won’t protect us from the shallower, say single-digit to low-double-digit corrective declines, we anticipate — as they did during last year’s washout — that our hedging activities will produce meaningful mitigation amid a deep selloff.

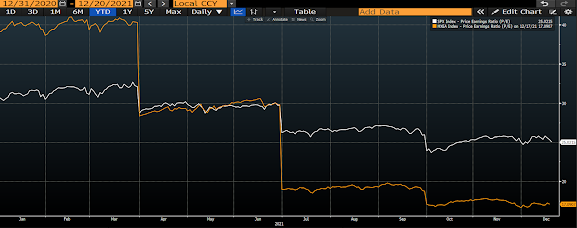

Digging a little deeper, let’s consider valuation.

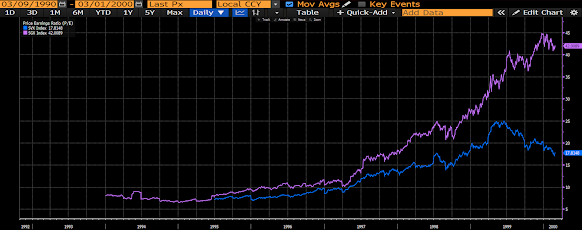

Here were the price to earnings (p/e) ratios during the 90s tech boom (the S&P value and growth indices were established in the mid-90s). Purple = growth, blue = value:

Indeed, at a p/e of 42, growth stocks in the aggregate were monumentally more expensive than value stocks (18 p/e) just as the tech bubble was about to unwind.

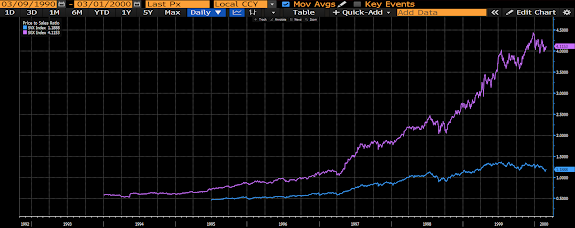

Here’s from the tech bust to the real estate/mortgage top:

While value remained “cheaper” than growth as the real estate bubble began to burst, the p/e spread got historically-narrow (17 vs 15).

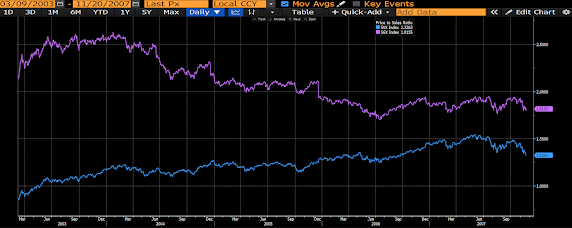

And here’s from the real estate bubble bottom to current:

That’s a p/e of 35 for growth, 19 for value. I.e., presently pushing toward that tech bubble topping setup…

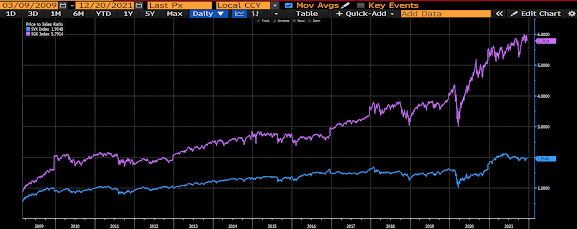

Being that revenue is arguably much harder to manipulate (pardon my cynicism) than is earnings, let’s consider price to sales (p/s) ratios:

The 90s boom:

The real estate boom:

The real estate bust to current:

While there are a number of other valuation metrics we can explore, suffice to say that value stocks presently offer up notable… well… “value” relative to growth stocks.

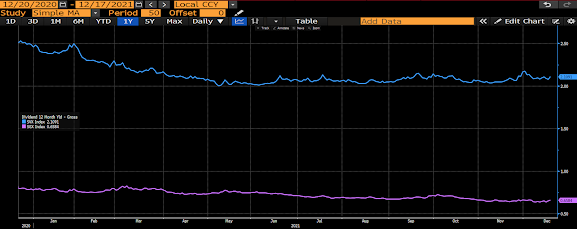

Let’s compare dividend income:

Value currently has quite the yield advantage over growth, to the tune of an annualized dividend rate of 2.11% versus 0.66% (or a spread of 1.45%).

Now we’ll take a snapshot of the current valuation and income setups for US versus Non-US developed market equities.

Current p/e (white = US, orange = foreign):

That’s 25 US, 17 Non-US…

Current p/s:

That’s a historically-high price to sales ratio of 3 (it peaked at 2.4 during the tech boom) for US equities, 1.5 for non-US…

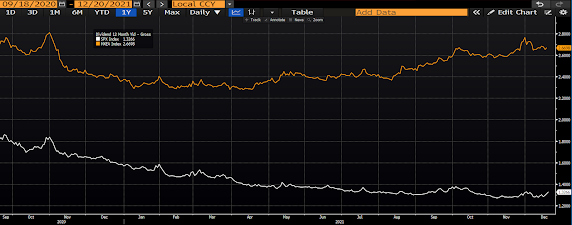

Dividend Yield:

That’s 1.33% US, 2.67% Non-US, for a yield spread of 1.34% in favor of Non-US…

Clearly, much like the attractive valuation and income setups with regard to US value over US growth, large cap foreign equities presently possess notable advantages over US large caps.

Of course, all of the above said, while markets are indeed subject to reversion, while valuations tend to matter in the long-run and while notably higher dividend income matters measurably as the years roll on, there’s certainly no guarantee that 2022 will usher in the next great stretch of value equities over growth, and foreign over US. Therefore, as always, proper balance, diversification — and hedging as/when prevailing risk demands — remains a must going forward.

Nevertheless, thinking in terms of multi-year probabilities, when we consider the above alongside the key considerations that have us presently leaning bullish on inflation and commodities, suffice to say that we’re feeling quite good about the risk/reward prospects for our clients’ long-term portfolios going forward.

Although we take absolutely nothing for granted when it comes to markets!

Stay tuned…