In yesterday’s note I placed less than 50/50 odds on the Fed raising its benchmark rate by .75% come tomorrow’s wrap of their 2-day policy meeting. Well, the market says different.

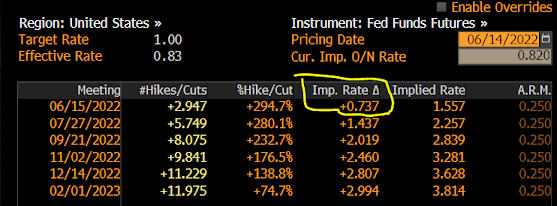

The yellow outline below says that’s precisely what Fed funds futures are pricing in.

Which, make no mistake, inspired the plunge yesterday that took stocks to levels that, as we’ve been explaining lately, inspired the sort of hedging action that added to the downward momentum.

Apparently, according to a complete 180 by the Wall Street Journal this week (one day they placed scant odds of a .75 hike, the next they’re predicting .75 hikes in June and July), .75 is nearly a given. Clearly they have insight into what Fed voting members are considering among themselves.

A .75 move tomorrow will be clear evidence that the Fed has moved on. I.e., abandoning (for the moment, anyway) its support of the equity market in favor of seriously battling inflation.

If, on the other hand, assuming the WSJ, and futures traders, indeed had an inside line on Fed-think (yesterday), and they now — in the wake of yesterday’s drubbing — surprise with a .50 move, well, then that says they still have feelings 💖for the market.

Aside from equities, if recent trends in the credit markets persist, well, let’s just say that Powell and Company can’t be sleeping well these days. Our own “Financial Stress Index” — which tracks yield curves, various spreads, lending sentiment, etc. — says that the risk that they’ll break something is rising too rapidly for comfort.

The Producer Price Index for May was released this morning, inspiring a bounce in equities. It came in lower across each component on a year-on-year basis, but, alas, likely not to a consequential degree at this juncture…

Stay tuned…

Asian equities were mixed overnight, with half of the 16 markets we track closing higher.

Europe’s leaning red so far this morning, with 11 of the 19 bourses we follow trading lower as I type.

US stocks are catching a bit of a bid to start the session: Dow up 133 points (0.44%), SP500 up 0.63%, SP500 Equal Weight up 0.79%, Nasdaq 100 up 0.84%, Nasdaq Comp up 0.77%, Russell 2000 up 0.46%.

The VIX sits at 32.59, down 4.20%.

Oil futures are up 1.97%, gold’s down 0.27%, silver’s down 0.05%, copper futures are down 0.33% and the ag complex (DBA) is down 0.23%.

The 10-year treasury is up (yield down) and the dollar is down 0.05%.

Among our 38 core positions (excluding cash and short-term bond ETF), 26 — led by Nokia, energy stocks, Dutch Bros, Albemarle and MP Materials — are in the green so far this morning. The losers are being led lower by uranium miners, Disney, gold, defense stocks and ag futures.

Unfortunately, while the following applies to policy, in the real world it too often applies to investing as well:

“…underlying trends become dominated by short-run shocks and policy responses. A related failing is that factors that dominate short-term forecasting are then given too large a role when it comes to constructing a long-term view.”

Have a great day,

Marty