In yesterday’s video commentary I offered a brief technical snapshot of the S&P 500 where the 60-minute chart pointed to the potential for short-term pop higher, plus a number of market indicators/setups that supported the notion that perhaps a “bear market rally” was in the near-term offing.

“Last Friday marked the most significant OPEX day since March 20, 2020, and, in one key respect, per the chart below (legend omitted as it reflects pay-walled proprietary data), since December 2018 as well. Both of which preceded huge rallies in equities:

The above notwithstanding and, while there remains this coming Tuesday as a potential for a post-opex dealer short-covering-inspired rally, it’s looking less likely by the minute. And, clearly, general conditions are vastly different, and less bullish today vs those past two occurrences (Fed was easing, or about to ease, virtually zero inflation to consider, etc.).

According to the snip below, hedge funds came to the market last week, shorting equities in apparently massive fashion:

“Additional near-term developments – ones that may inspire dovish (or perhaps less hawkish) Fed-speak and could, therefore, be net-near-term bullish – are this week’s drop in oil prices, weakening manufacturing data, a nascent rising trend in weekly jobless claims, falling housing permits and starts, rising credit market stress – all reflected in market-based inflation expectations coming off the boil.

2, 5 and 10-year inflation swap rates:

10-year high yield spread:

5-year IG CDS (cost of insurance against default for 5-yr investment grade bonds)

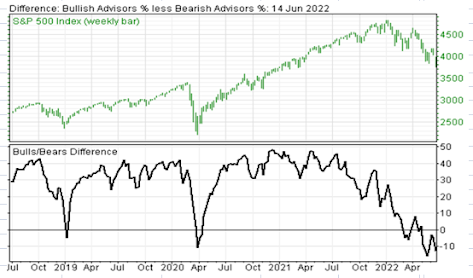

Then there are sentiment dynamics. Per the below, the bull/bear spread among investment advisors is at an extreme (negative) low – a level that typically closely precedes strong equity market rallies:

The individual investor read presently tells the same story:

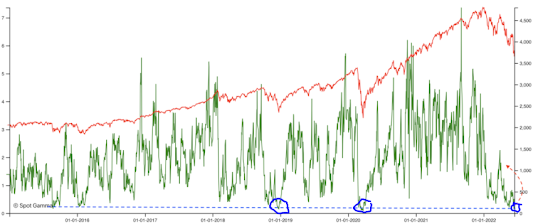

Also, the number of SPX members trading below their 200-DMAs is well below the level that typically precedes notable rallies:

Same with regard to the 50-DMA:

Lastly, the Nasdaq Comp has, for the second time in that past 4 weeks, just moved back into rare oversold territory on the weekly chart:

A phenomenon that over the past 30 years has closely preceded notable rallies. Last month’s rally happened to be the weakest produced by this signal (+11.64%):

Well, whether it’s options dealers covering shorts after all, or hedge funds forced to cover some of those supposedly massive (in total) short positions they put on last week, US stocks are seeing quite the rally to start the session.

Now, forgive me for pouring cold water on today’s presumably hot setup for equities, but… well… here’s the close that log entry:

“Now, all of the above said/illustrated, I’m still only talking about potential catalysts for a decent bear market rally. The longer-term price charts, macro and earnings prospects, central banks’ posture, credit market conditions and so on, present general conditions that ultimately overwhelm all of the above, and, therefore, have probabilities pointing to yet lower lows before all’s said and done.

Here’s a good summary coming from my email response this morning to a client question sparked by my Monday blog post stating that our 3500 SPX target could get seriously brought into question:

With regard to our SP500 target…

Technically-speaking (chart patterns), it’s the area (relative to price action and key moving averages) where corrections and bear markets (outside of recession) the past 30 years have bottomed… Key words there being “outside of recession.”

Now, one might argue that the precedent the Fed and Washington set when the market collapsed in 2020 (trillions of $ spent to rescue the economy — and the markets) presents a case that if we do dip into recession they’ll flood the system once again, and once again rescue markets…. Well, perhaps, but presumably there’ll be no pandemic lockdown to use as an excuse, and the monster difference today is inflation… It’s a huge factor that didn’t exist then, and, arguably, has been notably exacerbated by all of that stimulus…

In a nutshell, if corporate earnings contract notably (as they do during recession) against the current backdrop, and there’ll be no liquidity brought to bear the likes of what we saw in 2020 (at least not initially [it would indeed come eventually]), highly likely we’re looking at much lower lows… The past two recessions saw 50% and 57% drawdowns respectively for the S&P 500…

All that said, if we were at 3500 today, we would scale in a bit of the cash we’re sitting on, but we’d definitely be keeping some powder dry, all things considered…”

Asian equities rallied overnight, with 11 of the 16 markets we track closing higher.

Europe’s catching a bid as well this morning as well, with all but 1 of the 19 bourses we follow trading higher as I type.

US stocks are up across the board to start the session: Dow up 514 points (1.72%), SP500 up 2.37%, SP500 Equal Weight up 1.29%, Nasdaq 100 up 2.97%, Nasdaq Comp up 3.05%, Russell 2000 up 2.49%.

The VIX sits at 30.08, down 3.37%.

Oil futures are up 1.81%, gold’s up 0.12%, silver’s up 0.93%, copper futures are up 1.34% and the ag complex (DBA) is down 0.37%.

The 10-year treasury is down (yield up) and the dollar is down 0.23%.

Among our 38 core positions (excluding options hedges, cash and short-term bond ETF), 33 — led by AMD, our energy stock ETF, our semiconductor ETF, Nokia and MP Materials — are in the green so far this morning. The losers treasury bonds, our ag futures ETF, our utilities stocks ETF, our South Korean equity ETF and our Eurozone ETF (the latter reflecting today’s dividend distribution [taking down the share price by 2.1%, which’ll be recaptured when the dividend reinvests]).

While in many respects we live in unusual times, when it comes to market booms and busts, not so much:

“In the financial world, risk, reward, and catastrophe come in irregular cycles witnessed by every generation. Greed, hubris, and systemic fluctuations have given us the tulip mania, the South Sea bubble, the land booms in the 1920s and 1980s, the U.S. stock market and great crash in 1929, and the October 1987 crash, to name just a few of the hundreds of ready examples.”

Marty