As I mentioned yesterday, our PWA Index presently scores a recessionary -33.33; with 20% of its inputs scoring positive, 53% negative and 27% neutral.

One of its current negative influencers is the Sectors-to-SP500 ratio — each week we take a 30-day lookback at how each major sector is fairing against the broader market.

Here’s last week’s look (a below-100 score denotes the sector underperforming the S&P 500):

Financials (88.86):

Consumer Discretionary (99.19):

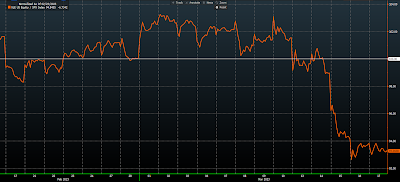

Energy (93.27):

So, when Tech is the only sector, among what we’ll call the economically-sensitive sectors, that’s presently outperforming the broader market, suffice to say that the economy ain’t presently looking so good.

Especially when you consider the fact that economically-defensive consumer staples and utilities have outperformed of late:

Utilities (102.57):

Healthcare, on the other hand, would be your defensive sector whose recent relative performance doesn’t comport with our overall recession score (give it time):

Now, looking again at those graphs, we need to address the rapid relative-performance descent of Industrials, Materials and Energy, in particular, that occurred over just the course of last week.

Thing is, if indeed that’s the right depiction of big-money positioning — while it may continue in the short run — it, in our view, is entirely the wrong thinking.

Asian stocks leaned green overnight, with 9 of the 16 markets we track closing higher.

Europe’s mostly red so far this morning, with 15 of the 19 bourses we follow trading down as I type.

US equity averages are rebounding from yesterday’s drubbing to start the session: Dow up 284 points (0.89%), SP500 up 1.21%, SP500 Equal Weight up 0.89%, Nasdaq 100 up 1.92%, Nasdaq Comp up 1.85%, Russell 2000 up 0.99%.

The VIX sits at 20.63 down 7.32%.

Oil futures are up 0.56%, gold’s up 0.51%, silver’s up 0.27%, copper futures are up 1.28% and the ag complex (DBA) is down 0.10%.

The 10-year treasury is up (yield down) and the dollar is down 0.07%.

Among our 36 core positions (excluding options hedges, cash and money market funds), 31 — led by AMD, Albemarle, MP Materials, Dutch Bros and base metals miners — are in the green so far this morning… The losers are TLT (long-term treasuries), EWZ (Brazil equities), LEMB (local currency emerging market bonds), Johnson and Johnson and VGIT (intermediate term treasuries).

“Still a man hears what he wants to hear and disregards the rest.” –Simon and Garfunkel

Might as well 😎 ⇩

Have a great day!

Marty