Now, before I share what I know will excite a number of our readers (you know who you are 😎), I have to warn you, while analogues can be useful in sizing up probabilities, just because patterns similar to today’s have formed during markets past, it in no way means today’s pattern will continue to play out in that same manner going forward.

So, as interesting/compelling as the following may seem, let’s keep the above front and center in our minds.

As you know, markets haven’t been challenged by the likes of this present-day inflation since the late-70s/early-80s… Therefore, it behooves the serious investor to consider the action back then when assessing probabilities in the here and now.

From an overall macro perspective, however, we consider the 1940s — which was the last time the US was saddled with over 100% government debt to GDP, with large amounts of debt in need of refinancing coming due, alongside the reality that government was set to run massive budget deficits as far as the eye can see — to be perhaps history’s best analogue for what’s happening today… Which, by the way, is in sharp contrast to the dynamics that Fed Chair Paul Volcker and company faced back in the early 80s… I.e., they didn’t have the debt sword of Damocles hanging over their heads, as does the Fed of 2022, and they were in fact just entering a resoundingly capital-friendly (disinflationary) era — as opposed to exiting one (it), which characterizes the present go-forward setup…

Therefore, our point remains that, tough talk aside, J. Powell and company — considering the current debt setup — simply cannot attack inflation the way the Fed of the early 80s was able to… Clearly, they’re already getting spooked by the prospects of seriously breaking something as they tighten the screws on the economy.

Nevertheless, Volcker’s name has been invoked ad nauseam of late (even by Powell himself) as the Fed has until very recently vowed to slay the inflation dragon at virtually any and all costs.

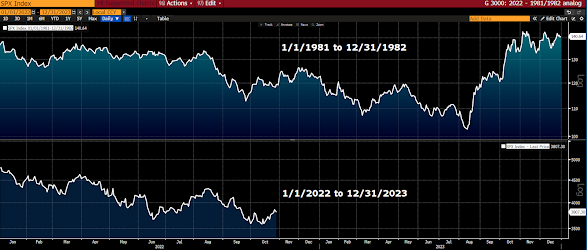

Interestingly, according to BCA Research analyst Dhaval Joshi, over the past 200 calendar quarters (50 years) there are only 2 where “all asset prices — stocks, bonds, gold, inflation-linked bonds, commodities — fell together”, which happened to be Q2 1981 and, yes, Q2 2022… In both instances “the Fed was fixated on killing inflation above all else.”

Now, if you’ve been paying attention to our commentary of late, particularly in the videos, you know that we’ve, albeit cautiously, been short-term constructive on stocks, while still anticipating yet another leg lower before the present bear market fully plays itself out.

So take a look…

Top panel — 1/1/1981 through 12/31/1982… Bottom panel — 1/1/2022 to current:

As I view these, thus far, similar patterns and consider the inflation dynamic, I’m reminded of good old Mark Twain with his “history doesn’t repeat itself, but it often rhymes,” which of course captures the logic behind technical analysis.

Asian equities leaned red overnight, with 10 of the 16 markets we track closing lower.

Same for Europe so far this morning, with 11 of the 19 bourses we follow trading lower as I type.

US stocks are green to start the session: Dow up 308 points (1.02%), SP500 up 0.58%, SP500 Equal Weight up 0.55%, Nasdaq 100 up 0.52%, Nasdaq Comp up 0.39%, Russell 2000 up 0.79%.

The VIX sits at 26.78, down 2.23%.

Oil futures are down 1.12%, gold’s down 1.11%, silver’s down 1.72%, copper futures are down 2.21% and the ag complex (DBA) is down 0.51%.

The 10-year treasury is down (yield up) and the dollar is up 0.08%

Among our 34 core positions (excluding options hedges, cash and short-term bond ETF), 20 — led by AMD, AT&T, tech stocks, energy stocks and communication stocks — are in the green so far this morning. The losers are being led lower by MP Materials, base metals futures, emerging market equities, silver and Brazil equities.

“If you’re experiencing contradiction, confusion, or even frustration in your thinking – that’s good news. Your intellect is having some brutal workouts.”

Andrei, Vizi. Economy of Truth

Have a great day!

Marty