This week has been virtually all about inflation. As we suggested (i.e., the obvious), inflation was clearly peaking, leaving only the question of speed and magnitude of the coming deceleration. Keep in mind PWA is firmly in the structurally-higher inflation camp going forward.

With regard to this week’s data and how to properly view it, Peter Boockvar stated it well in his note regarding the Producer Price Index released yesterday: emphasis mine…

“Bottom line, 80% of the headline drop was attributable to the fall in gasoline prices which fell by almost 17%. Outside of this, for the 5th straight month in CPI we’ve seen a moderation in the rate of change in goods prices and that is reflected here too. This data point too, points to the peak in inflation that we’ve been talking about here for a few months. The question again then is to what extent does it moderate from here and how quickly. I still believe it will take time and that inflation will remain sticky and persistent, albeit at lower rates of increase. If true, it will limit the Fed’s ability to eventually start easing at some point in response to the growing recession clouds.”

Oh, and by the way, today’s inflation is a global thing: France and Spain, for example, just reported their highest year-on-year inflation is over 30 years!

A key component to our inflation thesis is deglobalization — yes, and make no mistake, globalization was utterly huge in keeping inflation low these past few decades. This morning’s announcement that five Chinese state-owned companies will delist from the New York Stock Exchange further punctuates the trend.

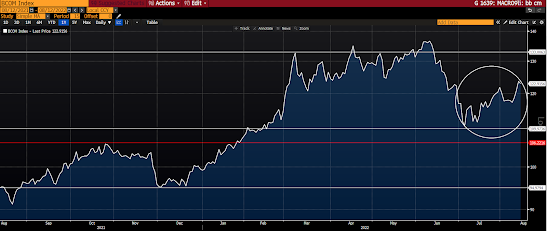

And, lastly, keeping this one short (our weekly economic update is on deck), to the extent commodities as a group explain inflation coming in a bit lower than expected of late… well, I circled July 6 to present in the graph below:

Bloomberg Commodity Index:

Asian equities leaned green overnight, with 7 of the 16 markets we track closing higher.

Europe’s net positive as well so far this morning, with 14 of the 19 bourses we follow trading up as I type.

US stocks are up to start the session: Dow up 168 points (0.50%), SP500 up 0.55%, SP500 Equal Weight up 0.54%, Nasdaq 100 up 0.64%, Nasdaq Comp up 0.52%, Russell 2000 up 0.54%.

The VIX sits at 19.96, down 1.19%.

Oil futures are down 2.22%, gold’s up 0.37%, silver’s up 0.93%, copper futures are down 1.43% and the ag complex (DBA) is down 0.24%.

The 10-year treasury is up (yield down) and the dollar is up 0.47%.

Among our 35 core positions (excluding options hedges, cash and short-term bond ETF), 26 — led by Disney, Albemarle, AMD, Brazil equities and silver — are in the green so far this morning. The losers are being led lower by Dutch Bros, base metals futures, MP Materials, oil services stocks and Nokia.

“The odds change as our position in the cycles changes. If we don’t change our investment stance as these things change, we’re being passive regarding cycles; in other words, we’re ignoring the chance to tilt the odds in our favor. But if we apply some insight regarding cycles, we can increase our bets and place them on more aggressive investments when the odds are in our favor, and we can take money off the table and increase our defensiveness when the odds are against us.”

–Marks, Howard. Mastering the Market Cycle: Getting the Odds on Your Side

Have a great day!

Marty