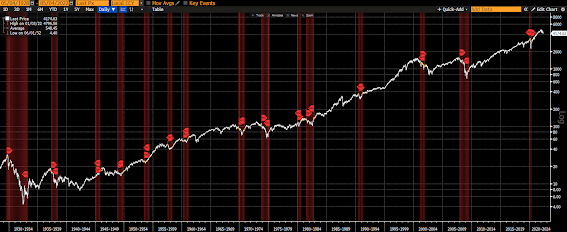

So, you bet, a 12.4% year-to-date decline in the S&P 500 and a 19.5% year-to-date hit to the Nasdaq is nothing so sneeze at. I mean, I’m sure folks are feeling it, particularly those who thought they were playing it “safe” with the old tried and true 60 (stocks)/40 (bonds) mix. That last one (using Blackrock’s 60/40 ETF as our proxy) is down 10.5% on the year so far.

And to add insult to what I’ll call minor (in terms of the depth of this year’s decline relative to historically-meaningful downturns) injury right here, with regard to the S&P 500 (white below), a year’s worth of price gains are gone. For the Nasdaq (blue) we’re talking 17 months. As for that 60/40 portfolio, our proxy is a traded ETF, and, therefore, in the process of rebalancing to that 60/40 target has seen large year-end capital gain distributions, which effectively lower the share price when they occur (i.e., a look back at share price movement would not fairly assess the results of that fund).

Now, please forgive my tough-loviness this morning, but, I must say, anyone who’s willing to expose his/her monies to the stock market is going to experience moments like these; history absolutely guarantees it!

So enough with this morning’s dose of reality… Well, actually, on second thought, I think — given what’s going on today — I better stay with that (reality) theme.

“Well, circa November of last year, the Fed’s stance took an abrupt turn from what many, yours truly included, consider the primary reason for what has been history’s greatest bull market in stocks — that would be their on-balance uber-easy policy stance over the period.

I.e., inflation — the likes of which hasn’t been seen in 40 years — had them changing their tune from one that promised to protect asset prices at virtually all costs to one that promised to slay the inflation dragon, markets be damned (well, we’ll see)...”

If indeed this particular Fed’s predisposition has them praying for an out (of their threatened aggressive go-forward stance), yesterday’s labor market data gave them zero room to wiggle.

Here’s from Bespoke Investment Group’s coverage: emphasis mine…

• Today’s Job Openings and Labor Turnover Survey (JOLTS) data for March provided ample evidence of a very hot labor market that continues to look as healthy as can be.

• While the layoff and discharge rate is slightly above lows a few months ago, it remains well below historical norms and those separations were less than 1% of the total nonfarm labor force in March.

• Similarly, hiring is very robust, with gross additions to firms (distinct from the net numbers measured in payrolls data at the end of each month) continuing to accelerate as employers eagerly add unemployed workers or poach talent from other companies.

• Hires this high almost mathematically require higher quit rates and they continue to run at a very impressive pace; workers are finding it easy to locate a better deal from an alternative employer and are therefore jumping ship at historic rates.

• With job openings running at more than 7% of the labor force, that strong environment for worker bargaining power looks set to continue.

• Bottom line: JOLTS for March confirmed a very tight and healthy labor market.

Asian equities saw mostly red overnight, with 10 of 12 open (4 were shuttered) markets we track closing lower.

Europe’s a mess so far this morning, with 17 of the 19 bourses we follow trading lower as I type.

US major averages (save for the Dow) are off to start the day: Dow up 36 points (0.11%), SP500 down 0.33%, SP500 Equal Weight down 0.09%, Nasdaq 100 down 1.22%, Nasdaq Comp down 1.26%, Russell 2000 down 0.84%.

The VIX sits at 29.08, down 0.58%.

Oil futures are up 3.81%, gold’s up 0.03%, silver’s down 0.85%, copper futures are up 0.71% and the ag complex (DBA) is up 0.59%.

The 10-year treasury is down (yield up) and the dollar is down 0.14%.

Among our 39 core positions (excluding cash and short-term bond ETF), 18 — led by Albemarle, AT&T, AMD, energy and utility stocks — are in the green so far this morning. The losers are being led lower by uranium miners, our semiconductor ETF, emerging market equities, Nokia and MP Materials.

“Preferences are optional and subject to constraints, whereas constraints are neither optional nor subject to preferences.”

Have a great day!

Marty