While you’d expect quiet on the day before Thanksgiving, well, definitely not — in terms of the number of data releases — on the economic front.

Here’ I’ll try to sum much of it up:

The US jobless picture continues to improve.

US durable goods orders on-the-surface look decent, however, we need to remain cognizant of the fact that while new orders are up 9.5% this year, the Producer Price Index is up 11.5%. Hmm…

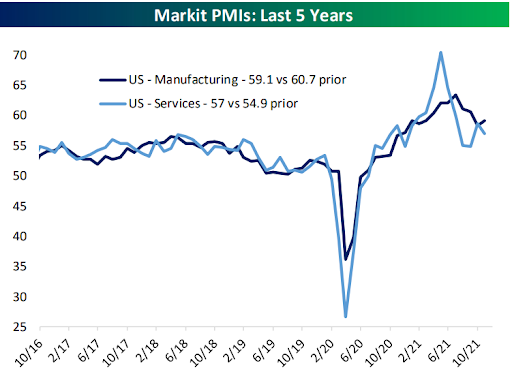

Yesterday’s preliminary Purchasing Manager sentiment readings shows manufacturers feeling relatively upbeat, service sector actors, less so:

Chart by Bespoke Investment Group

Mortgage purchase apps rose week-over-week, although still down 4.4% year-over-year. Refinances were essentially flat on the week, down 34% year-over-year.

New home sales were up 3k on the month, but 45k lower than expectations.

University of Michigan’s US consumer sentiment survey came in a bit better than expected on the headline number, but nevertheless down from the previous month. Inflation expectations continue to rise.

Despite flailing confidence readings, US consumers are determined to enjoy the upcoming holiday season. Purchases of goods and services rose a not-small 1.3% on the month. Inflation, per the Fed’s preferred inflation gauge, however, rose 0.6%, up 5% year-over-year!

US personal income rose .5% on the month. Adjust for taxes and inflation, however, and personal income actually declined 0.3% last month (3rd monthly decline in a row).

The US consumer savings rate dropped to 7.3% (more or less the pre-covid level).

Sentiment across Europe is mixed. Amazing that it’s not dire given the latest COVID numbers.

Japanese sentiment is on-balance improving: I.e., while firms are reporting rising price pressures, growing vaccination rates and lessening of restrictions have companies “strongly optimistic” on business activity over the coming year. As we’ve illustrated herein, we like Japanese equities going forward!

Asian equities were mixed overnight, with half of the markets we track closing lower.

Europe’s essentially splitting the difference as well this morning.

US major averages are off a bit across the board: Dow down 63 points (0.18%), SP500 down 0.11%, SP500 Equal Weight down 0.09%, Nasdaq 100 down 0.26%, Nasdaq Comp down 0.15%, Russell 2000 down 0.13%.

The VIX, at 19.81, continues to signal caution. Up 2.06%.

Oil futures are up 0.50%, gold’s down 0.32%, silver’s down 0.84%, copper futures are up 1.10% and the ag complex is down 0.10%.

The 10-year treasury is down (yield up) and the dollar is up a big 0.43%.

Led by MP (rare earth miner), KRBN (carbon credits), AMD (chip maker), energy stocks and base metals futures — but dragged by Indian equities, Mexican equities, Uranium miners, Asia-Pac and Eurozone equities — our core portfolio is down 0.24% to start the day.

The great Milton Friedman on inflation:

“Inflation is just like alcoholism. In both cases when you start drinking or when you start printing too much money, the good effects come first. The bad effects only come later.

That’s why in both cases there is a strong temptation to overdo it. To drink too much and to print too much money.

When it comes to the cure, it’s the other way around. When you stop drinking or when you stop printing money, the bad effects come first and the good effects only come later.”

On that note: HAPPY THANKSGIVING TO YOU AND YOURS!!

Marty