Like I said yesterday, the setup for inflation, and, nearly by default, commodities, is resoundingly bullish well into the foreseeable future. I also said that as investors embrace that sentiment, related markets will get ahead of themselves and correct, at times “violently.”

While this morning’s selloff across the resource complex is anything but violent, and while there are a number of headline drivers to credit, a breather right about now would make sense, and, frankly, would be welcome.

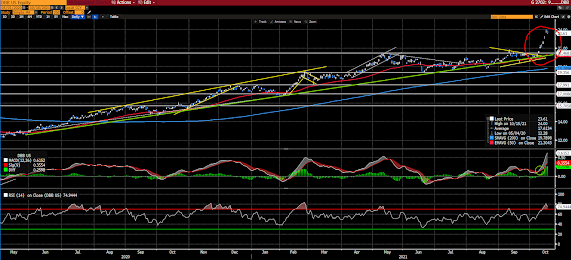

Recall in Sunday’s video the charting we did of our base metals ETF. I pointed out that nothing goes parabolic without ultimately giving some, sometimes a lot, back before resuming its uptrend (assuming it’s going to).

Here again is that chart we worked on together:

Now let’s zero in on the past 5 trading days:

While a 3.6% 5-day move is nothing to freak out over in a position that’s up 70+% since we added it last year, it nevertheless hints of the potential volatility I pointed to yesterday.

By the way, we cut the position by 30% on Monday (bought SOXX [semiconductors] and more AT&T with the proceeds) and bought a put option out till next April on the remaining position with a strike price of $20. The position trades at $22.11 this morning.

Bottom line, the long-term setup remains compelling for our commodities-related exposures, but, like everything else, they’ll need to be appropriately managed along the way. The prior week we cut a bit of our energy exposure and added to consumer staples stocks.

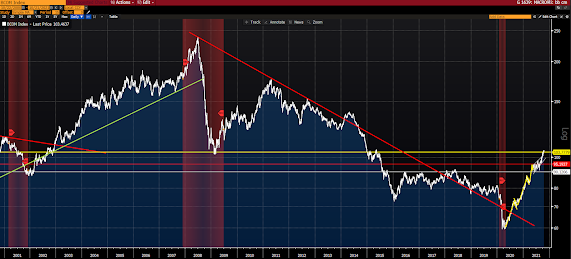

Lastly, to really drive the point home, take a look at the 5-year chart of the Bloomberg Commodity Index:

Yes, it’s looking lofty. However, not (necessarily) so much when we consider that it’s just a few months removed from breaking above a 12 year down trend. Commodity trends tend to run for several years:

Asian equities got creamed overnight (Japan by 1.9%), with 12 of the 16 markets we track closing lower.

Europe’s leaning red this morning as well, with 10 of the 19 bourses we follow trading lower, as I type.

U.S. major averages are mixed: Dow down 73 points (0.20%), SP500 up 0.06%, SP500 Equal Weight down 0.08%, Nasdaq 100 up 0.37%, Nasdaq Comp up 0.42%, Russell 2000 up 0.33%.

Note: We can mostly thank tech for this morning’s relative buoyancy in US equities, as industrials, financials, staples, healthcare, energy and materials are all taking hits to start the session.

The VIX sits at 15.48, down 0.06%.

Oil futures are down 1.63%, gold’s down 0.25%, silver’s down 0.73%, copper futures are down 2.22% and the ag complex is down 0.70%.

The 10-year treasury is down (yield up) and the dollar is up 0.04%.

Led by AMD (chip maker), KRBN (carbon credits), solar stocks, wind stocks and semiconductor stocks — but dragged notably by base metals, uranium miners, Latin American equities, MP (rare earth miner) and energy stocks — our core mix is off 0.56% to start the day.

I have to agree with the late great Benoit Mandelbrot on the following, at least when we’re talking short-term volatility:

“In substantial part, prices are determined by endogenous effects peculiar to the inner workings of the markets themselves, rather than solely by the exogenous action of outside events.”

“Finance is a black box covered by a veil. Not only are the inner workings hidden, but the inputs are also obscured, by bad economic data, conflicting news reports, or outright deception.”

Have a great day!

Marty