This morning’s action in treasuries, and the dollar, has me belaboring just a bit the labor topic (touched on it here, here and here Friday and Saturday).

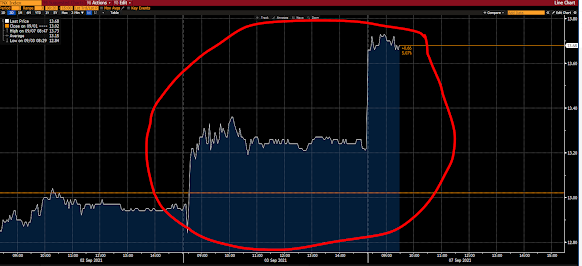

Suffice to say that if the majority of the headlines have it right, that it’s all (or mostly) about the Delta variant, and/or if the bears have it right, that it’s all about a weakening economy, well, you wouldn’t be seeing this in yields Friday and today:

Yes, by the way, I do see the Fed ultimately capping yields before this is all over, but not at these low levels. I.e., there’s clearly some upside risk in yields right here.

Nor would you see this in the dollar (as its been trading on yields of late) this morning:

If Friday’s jobs miss was indeed about what the headlines suggest, those charts would be turned on their heads.

Asian equities were mixed overnight, with 8 of the 16 markets we track closing lower.

Europe’s struggling nearly across the board this morning, with all but 2 of the bourses we follow in the red as I type.

U.S. stocks are mostly off as well to start the week: Dow down 204 points (0.58%), SP500 down 0.32%, SP500 Equal Weight down 0.55%, Nasdaq 100 down 0.10%, Nasdaq Comp up 0.04%, Russell 2000 up 0.21%.

The VIX sits at 17.90, up 9.08%.

Oil futures are down 0.98%, gold’s down 1.01%, silver’s down 0.83%, copper futures are down 0.76% and the ag complex is down 0.05%.

The 10-year treasury is down (yield up) and the dollar is up 0.37%.

Led by uranium miners, MP (rare earth miners), Latin American equities, Viacom and KRBN (carbon credits) — but dragged by industrial stocks, gold, healthcare stocks, silver and utilities stocks — our core portfolio is up 0.03% to start the session.

“it’s easier to fool people than to convince them that they have been fooled.”

Ain’t that the truth!

Have a great day!

Marty