For this week’s main message I’ll share an excerpt from my latest internal log entry, where I briefly update our theses on individual positions. Specifically, non-US equities, gold and ag futures. But first, my thoughts on today’s market reaction to the release of the Fed’s latest meeting minutes.

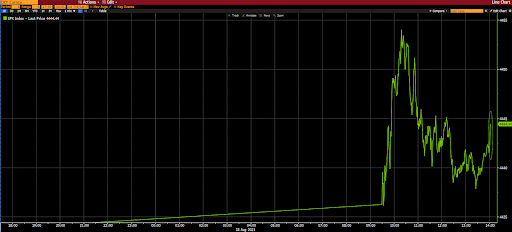

Before I heard or read a peep on the Fed’s notes, it was, at least initially, clear to me that they intend to remain very accommodative. I got that signal from the immediate move in the dollar (plunged):

VPL: The Developed Asia Pacific region, sporting notably more compelling valuations and dividend yields vs the U.S., has much ground to make up on a long-term relative return basis.

Our longer-term (lower) dollar thesis adds a notable advantage to non-US equities as well.

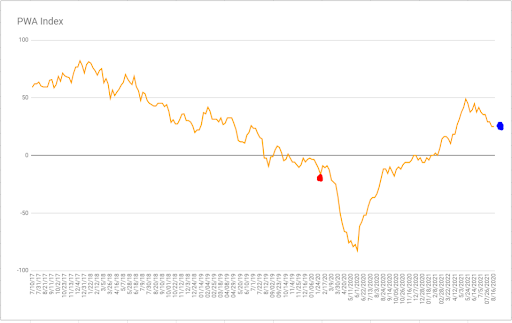

Note (top panel) the gross underperformance of Asia-Pac (yellow) vs U.S. equities (white) during the 90’s tech boom. And the rising dollar (bottom panel):

Then the outperformance of Asia-Pac from the bottom of the tech bubble bear market to where the subsequent bull market peaked. And the declining dollar:

Then the underperformance of Asia-Pac from the bottom of the mortgage/real estate bubble bear market to the peak in February of last year. And the rising dollar:

And from that peak to current (note the circles where Asia-Pac peaked and the dollar bottomed back in February of this year):

GLD: Gold, while it has been somewhat of a ball and chain on the portfolio since last July, is uniquely positioned to do long-term well given our thesis. I.e., to repeat:

“While it’s my view that the Fed literally cannot (without crashing the markets) tighten monetary policy to any consequential degree, I nevertheless believe there’s upside risk in interest rates. Although there’s a serious pain point where the Fed steps in. I think it could be as low as 2% on the 10-year treasury, although equity market action will ultimately make that determination. I.e., if the 10-year pushes to 2% without a major selloff in equities, rates can go higher.”

The fed stepping in (yield curve control) amid structurally rising inflation is the quintessential setup for gold. Plus, it tends to perform notably better than equities during protracted bear markets as well, essentially providing a potential hedge against consequentially declining stocks. And of course gold correlates demonstrably negatively with the dollar (its monthly correlation coefficient from March 2009 to present is -.63).

While, per the above, gold’s long-term prospects are compelling, it is clearly at risk between here and the Fed’s pain point on the yield curve. Which has us presently hedging the GLD position with put options.

DBA: Owning ag futures going forward is a virtual must, all things considered. In a nutshell; challenges related to inflation, supply constraints, geopolitics, global demographics, and weather patterns all play beautifully for a sector that (like the rest of the commodity space) has been unloved for the past decade+, and, therefore, is now hugely under-owned.

FEZ: Essentially the same case — valuations, dividend income, ground to make up, negative correlation to the dollar — made on behalf of our Asia-Pac exposure can be made for developed Europe as well. I’ll add, and it can be added to the Asia-Pac narrative as well, that when investors wake up to the reality that U.S. stocks have reached historically-bubbly extremes — either at the peak of today’s bull market, or during (or subsequent to) its demise — a protracted period of underperformance for U.S. equities in the aggregate will unfold.

VWO: Emerging economies house the largest, youngest concentration of Earth’s humans. With, as the word “emerging” denotes, greater growth potential vs — as the word “developed” denotes — developed economies. Of course with growth comes growing pains, which makes for greater volatility and prolonged periods of underperformance.

As has been the case with non-US developed markets, emerging market equities have seen an extended period of relative (to the US) underperformance. The same case with regard to valuations and dividends is to be made here as well, while the negative dollar correlation case is even stronger (significantly!).

The monthly correlation coefficient for the MSCI Emerging Market Index vs the dollar from March 2009 to present is -.64. While it’s -.32 for MSCI Asia-Pac, -.21 for MSCI Europe, and a less negative -.03 for US equities (SP500).