Lots to parse in our weekly macro exercise today, so I’ll keep this morning’s note short and sweet.

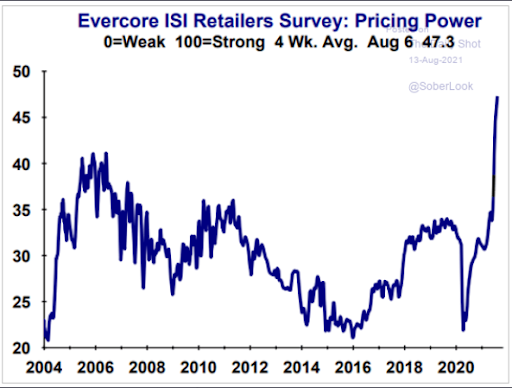

So, according to an Evercore ISI survey, retailers are presently able to pass higher costs onto the consumer:

“Maybe next time we’ll delve into additional measures Mom and Pop might deploy (say they determine that they can’t cut 3 Ashleys and serve their customers), such as changing the thermostat’s setting (making conditions less comfortable for those higher-earning employees—not to mention the customers who we’ll assume will be willing to bear a less hospitable environment), raising prices, opting for lower-quality beef, serving fewer, and skinnier, french fries, changing the oil in the fryer less often, charging employees full price to eat their own cooking during their lunch break, making them purchase their own uniforms, etc, etc, etc.”

And please understand, should you choose to click through and read that old article, that I was 100% advocating on behalf of the employee.

Asia struggled overnight, with 10 of the 16 markets we track closing lower.

Europe’s nicely green this morning, with 14 of the 19 bourses we follow trading higher as I type.

US stocks are mixed to start the session: Dow up 26 points (0.07%), SP500 up 0.05%, SP500 Equal Weight down 0.05%, Nasdaq 100 up 0.19%, Nasdaq Comp up 0.02%, Russell 2000 down 0.61%.

The VIX (SP500 expected volatility via options pricing) sits at 15.49, down 0.64%.

Oil futures are up 0.07%, gold’s up 0.97%, silver’s up 2.20%, copper futures are up 1.38% and the ag complex is up 0.21%.

The 10-year treasury is up (yield down) and the dollar is down a big 0.45%.

Led by AMD (new semiconductor position for us), silver, gold miners, base metals futures and NOK (new 5g play for us) — but dragged by MP (rare earth miner), uranium miners, solar stocks, energy and financial stocks — our core mix is up 0.20% to start the day.

In Marko Papic’s insightful book Geopolitical Alpha, he teaches that while the world tends to focus on the personalities/preferences of those in power, it’s actually their constraints one should focus on when assessing policy probabilities going forward. I couldn’t agree more!

“…investors (and anyone interested in forecasting politics) should focus on material constraints, not policymaker preferences.”

“Preferences are optional and subject to constraints, whereas constraints are neither optional nor subject to preferences.”

Marty