Clients and regular readers know that our overall macro thesis includes a view that has odds favoring inflation running “hotter” well into the foreseeable — beyond the present “transitory” rise in prices that was inevitable given the dead-stop/fast-rebound (pent-up-demand) nature of COVID providing cover for the most aggressive fiscal and monetary action the world has ever seen (including, on the monetary side, an utter breaching of the Federal Reserve Act of 1913 [forbids the Fed from buying corporate securities, which they did anyway], which of course, on top of taking personal incomes [via “stimulus” checks], in the aggregate, above prepandemic levels) — takes the concept of moral hazard to a whole new level!

Therefore, being true to our research/data-driven conviction, our core portfolio features exposure to the likes of gold, silver, base metals and agriculture futures, metals and minerals miners’ stocks, and the equities of companies domiciled in commodity-centric emerging nations. All trades (save for gold) that worked quite nicely this year; up to early/mid June, that is.

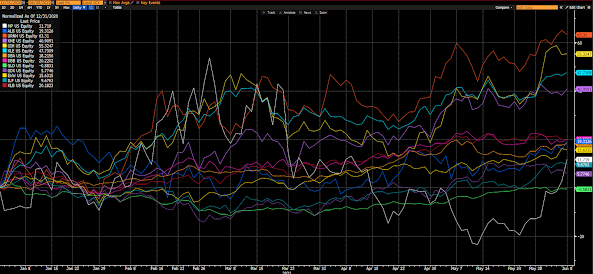

Here are those positions 1/1 through 6/8:

Gold performed the worst (-0.58%), 2nd-worst being gold miners (+5.77%), the rest ranged from +9.67% (Latin America) to +63.31% (uranium miners).

Fast forward to the present; my what a difference 6 weeks can make!

Here’s how they’ve done since:

The best performer (during the stretch) being Latin American equities (+7.39%), the worst being uranium miners (-21.60%), with oil services the next worst (-21.58%). The rest ranged from -0.45% (rare earth miner) to -14.47% (energy index ETF).

And, putting the two charts together, here’s the year-to-date look:

Best being our lithium miner (+26.93%), worst being gold miners (-7.55%). The rest ranging from -5.03% (gold) to +26.64% (uranium miners). Honorable mention goes to energy stocks (+25.57%), metals miners (+21.53%) and oil services stocks (+20.63%).

Now, what about that present “PWA mantra” I keep telling you clients about? You know;

“In the present environment our aim is to simply compound returns at a decent rate while diversifying/hedging in a manner designed to mitigate a major market selloff.”

I mean, holding stuff that can go up over 60% in 5 months, then down over 40% in less than 2! That doesn’t jibe with that mantra, now does it?

Well, not at first blush, but we’re talking asset allocation my friends, which, done right, mixes securities that don’t all move in the same direction at the same time.

Take a closer look at those graphs above. Even though each plays in the resource space — and should do well in an inflationary environment — notice how (while there are clear positive correlations among many) they don’t all move in the same direction at the same time. And, of course, we take into account each position’s inherent volatility when we size it. For example, the one with the craziest moves occupies a mere 0.6% of our total core portfolio.

All in, the above positions make up 38% of our overall target allocation. The remaining 62% is divided among cash and super short-term high-grade corporate bonds (18%), developed economy non-US equities (19%), emerging market equity index (8%) and (17%) other U.S equities (industrials, financials, healthcare, utilities, tech, staples, telecom).

Suffice to say, we are managing a very diversified mix of assets, plus we’re hedging against the big downside stuff with options (i.e., remaining true to our mantra).

Note: Even though, through diversification and options hedging, we’re working to notably mitigate the worst of the major market declines, our more risk (volatility)-averse clients have a higher fixed income/lower everything else mix in their portfolios…

So, all of the above just to set the stage for our view of what’s happened of late to the inflation trade.

For starters, as I stated in a number of weekly video messages leading into the recent selloff, the overall trade had run a little too far, a little too fast, for my taste. And, therefore, we anticipated some downside action in the coming weeks/months. Definitely called that one! Although, I must say, the extent of the correction was overall greater than I anticipated — barring an across the board stock market selloff (tech and consumer discretionary held up fine).

Thing is (strategically-speaking), as I also pointed out, the likelihood of a downturn notwithstanding, there was nothing at that point getting in the way of our overall inflation thesis. And, frankly, there still isn’t. But, that said, it’s still worth (necessary even for our purposes) understanding what’s behind the downdraft. I.e., is it purely profit-taking/consolidation of gains, or is there something more pernicious getting in the way of our overall relative performance of late?

Well, I’d say it’s definitely the latter, inspiring the former.

The latter, on the surface, being the Fed’s albeit slight pivot (in words, not actions) to maybe a little less accommodation (money printing and interest rate suppression) going forward. The value (the reflation) trade either took the Fed seriously and assumed they’d upset the applecart just as it’s gaining momentum, or warned, in no uncertain terms, that the Fed has virtually no wiggle room: I.e., tighten monetary policy and the markets will punish you unmercifully!

Plus, and clearly, the delta variant is playing serious havoc in the minds of traders — as, clearly, any degree of lockdown will have demand — and near-term inflation — waning. That said, imagine the reflation trade coming out of yet another round of lockdowns. Although, I don’t suppose those who’ve been vaccinated and aren’t shy about mask-wearing (not to mention those who haven’t been, and who are) are going to be the least bit welcoming to being shut in once again.

So, save for a few perhaps notable pockets here and there, the politics of locking down in a big way make it prohibitive.

Those two factors — along with other weedy things, like futures traders being notably short treasuries (betting on higher interest rates [read inflation]) and, thus, finding themselves caught off guard and forced to cover (buying treasuries, pushing interest rates lower, and casting huge doubt on the inflation trade), and not to mention the auto-rebalancing of blended funds out of outperforming value stocks and into underperforming bonds, and the prospects for a slowing Chinese economy — served to shake the resolve of skittish investors; inspiring them right back to the trade that’s worked wonderfully these past few years (read tech), despite the fact that no wonderful trade EVER lasts forever — and that value (out of favor asset classes, sectors, regions) ultimately has its day (for typically extended periods of time).

So then, we’re left with the following questions?

1. Will the Fed implement tightening measures to slow the risk of higher inflation going forward?

2. Will the delta variant derail the reopening of the global economy?

3. Will politicians come to terms on meaningful infrastructure investments (to the tune of $trillions) over the next several years?

4. Will world leaders keep their sights on curtailing carbon emissions and aggressively promoting renewable energy sources going forward.

5. Will governments — including China — (along with their central banks) step in with stimulus anytime their respective economies threaten to roll back into recession?

6. Will governments continue to cater to generally populist anti-global sentiment within their own jurisdictions?

Our answers:

1. NO

2. Can’t know for sure, but politics say no

3. Yes, but with plenty of market-upsetting grandstanding along the way

4. Yes

5. Yes

6. Yes

Now, the ultimate question for investors at this juncture:

Will the above lead to a general weakening of the dollar and strengthening of inflationary pressures well into the foreseeable future?

Our answer: Odds/probabilities, at this juncture, say yes…

Thanks for reading!