Mixing it up a bit, we’ll do this week’s macro update in writing…

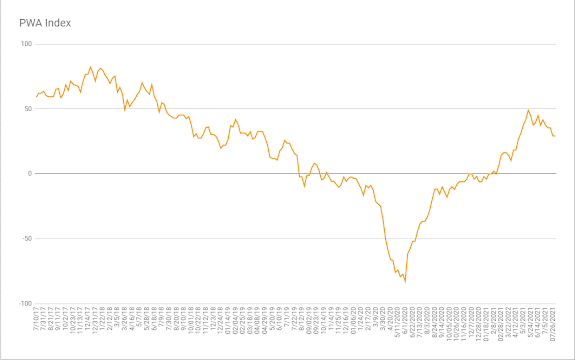

For starters, our own general conditions index scored no change on the week, with an overall macro score of 29.17:

Although it’s not that we didn’t have any needle-moving inputs, it’s that the four that saw individual score changes cancelled each other out.

The two positives were:

The consumer savings ratio:

and the price of copper.

The two negatives were:

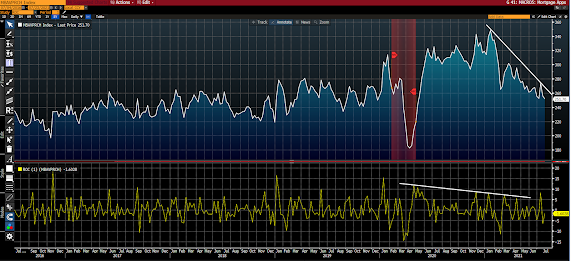

Mortgage purchase apps

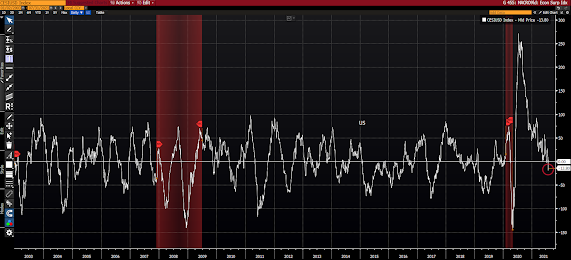

and the U.S. Economic Surprise Index.

So why would a declining consumer savings ratio score positive in our index? Great question! You see, at 9.4% of personal income it’s still historically high, and seeing it come down from those extremely high (covid) levels speaks to the consumer’s willingness to spend more of his/her income (which is presently holding up) on him/herself. And we live in a consumption-driven economy.

A rebounding copper — the most ubiquitous industrial metal — price speaks to the prospects for everything construction and renewable energy going forward. And, not to mention, a general tightness in capacity relative to demand.

On the negative side, the consistent decline in mortgage purchase apps of late flies in the face of the present residential market narrative. Although it indeed comports with the buyer sentiment indicators we’ve shared herein, as well as the parabolic rise in home prices we’ve witnessed of late –– pricing out the all-important first time buyer cohort. Pending home sales, by the way, were down 1.9% month-on-month for June. Although that comes off of an 8.3% jump in May.

While we’re not seeing any recession risk to speak of right here, per the U.S. Economic Surprise Index falling below zero, the economy is not nearly meeting economists’ latest expectations.

One more positive of note:

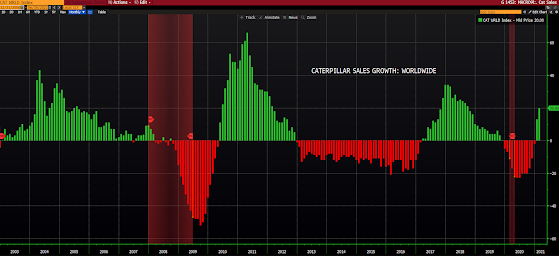

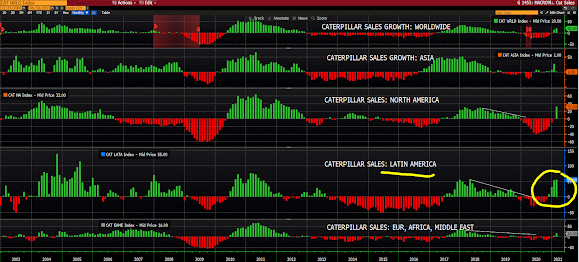

A non-needle-mover (already receives our highest score) worth mentioning is the quarterly update of Caterpillar global sales.

A second consecutive quarter of double-digit sales growth speaks to our general thesis around infrastructure spending going forward. Although it also speaks to favorable base effects — i.e., recall where we were in Q2 of last year!

Breaking it down, note the 4 consecutive quarters of sale’s growth (capturing the year-over-year growth off of pre-covid levels as well) in Latin America; an area we are long-term quite bullish on:

In a nutshell, the economy’s in okay shape right here. But let’s not forget what got us here — an (historically-speaking) unfathomable amount of top-down intervention. Which makes for all manner of distortions (read risk) that we’ll be carefully navigating in the months and years to come.

I’ll close here with my latest musings in our internal log:

7/30/2021 General Macro Thoughts

The merger of fiscal and monetary policy far into the foreseeable future is a given. Which makes for an investment landscape resembling the 1940s and, in some respects, the 1960s.

The past several decades that were resoundingly pro corporate, pro markets, pro debt, pro lower interest rates have resulted in a gaping inequality that is no longer sustainable, or politically-feasible. The relative losers (consumers at large) now have to be accommodated. But now we have an economy so levered to asset prices that are bubbly to the point that, if pierced, will take the economy down with them. Which, while indeed shrinking the inequality gap, would nevertheless markedly injure the voting populace in the process.

Hence, facing the choice of either allowing asset prices to contract to fundamentally-viable levels (i.e. crash!) versus running large fiscal deficits, and redistributing wealth, in order to nominally grow personal incomes and GDP, fostering steady rising inflation in the process — the latter is essentially the only choice.

Thus, every downturn will be met with aggressive fiscal and monetary stimulus… In other words, given the choice of either surrendering the equity market, the credit market or the dollar going forward, it is abundantly clear that the dollar’s the loser…

If it all plays out like the 40s, inflation will essentially cure the historically-high debt to GDP conundrum — by 1951 we were back well below 100% debt to GDP and the aggressive yield curve constraints were no longer necessary — but not without plenty of market volatility along the way…

Investment prescription: Exploit the setup with a healthy allocation to metals, miners, energy, renewable energy (minerals, etc), gold, silver, commodity currencies, etc… and don’t go unhedged under any circumstances…